Japan Macro Daily(Beta Mode)

Tankan Lifts Sentiment as Yen Tests Lows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 70,062.32 | +0.86% |

| USD/JPY | 162.52 | -0.07% |

| EUR/JPY | 184.92 | -0.37% |

| GBP/JPY | 215.78 | +0.14% |

| Gold | 4,044.60 | +0.54% |

| Brent Crude | 71.14 | -2.44% |

| Bitcoin | 60,748.32 | +3.74% |

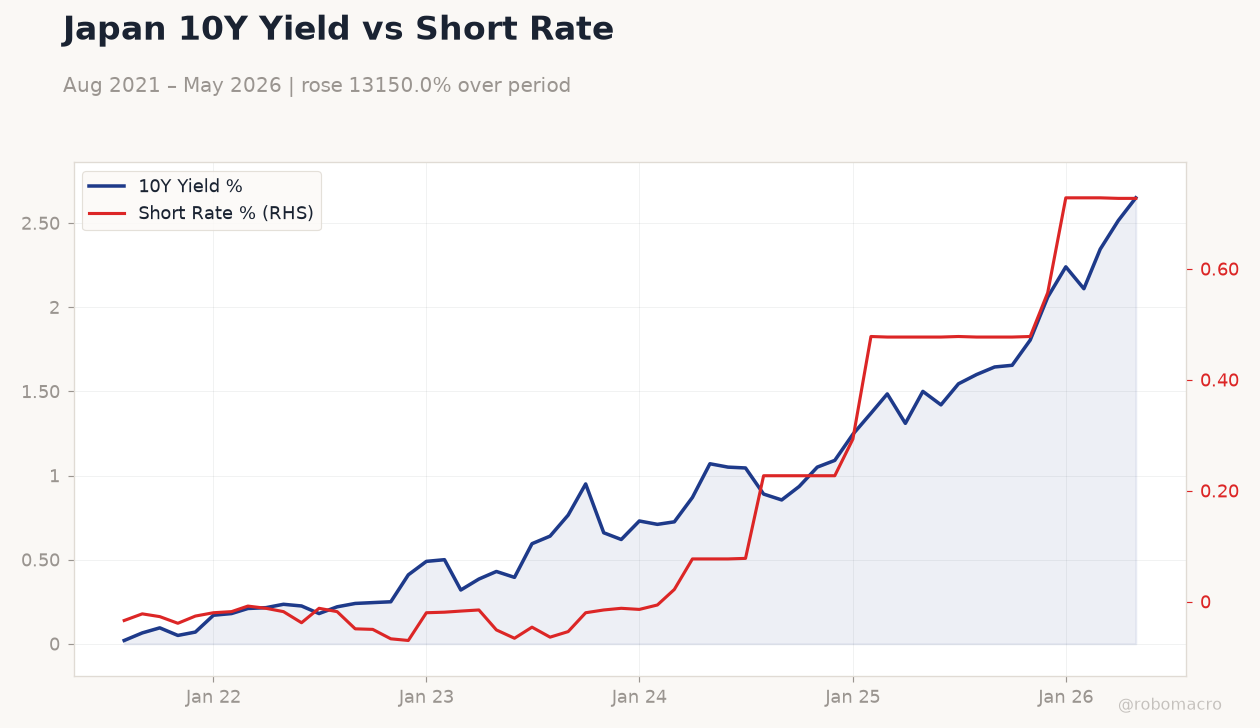

| Japan 2Y Govt Yield | 0.73% | +0.00% |

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 33.60 | 34 | 33.80 |

Japan 10Y Yield vs Short Rate | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65 | Short Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(5pt): -0.034,-0.05,-0.012,0.478,0.727

Japan 10Y Yield vs Short Rate | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65 | Short Rate %: 0.727 (2026-05-01) | Range: -0.07–0.728 | Trend(5pt): -0.034,-0.05,-0.012,0.478,0.727

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Monday (2026-07-06) | |||

| Household Spending Month-over-Month | 1.60 | - | 19:30 |

| Household Spending Year-over-Year | -0.50 | - | 19:30 |

| Tuesday (2026-07-07) | |||

| Current Account Balance | 3,907,000m | - | 19:50 |

- Consumer confidence edged up to 33.8 in June, beating the 33.6 prior but missing the 34 consensus.

- Nikkei 225 rose 0.86% to 70,062.32 while the 10-year JGB yield jumped 5.37% to 2.65%.

- USD/JPY held at 162.52 amid ongoing speculation over intervention thresholds.

Yesterday's Recap

Japan’s Consumer Confidence Index printed 33.8 for June, a modest improvement from 33.6 that still fell short of expectations. Equity markets responded positively with the Nikkei 225 advancing 0.86% to close at 70,062.32. The 10-year government bond yield surged 5.37% to 2.65%, reflecting firmer rate expectations, while the 2-year yield stayed at 0.73%.

USD/JPY eased 0.07% to 162.52 as thin holiday volume limited moves. EUR/JPY fell 0.37% to 184.92 and Brent crude dropped 2.44% to 71.14. Broader risk appetite lifted Bitcoin 3.74% despite the yen’s persistent weakness near 40-year lows.

The Day Ahead

Attention turns to the July 6 releases of household spending data for May, covering both month-over-month and year-over-year changes. Markets will also watch the July 7 current account balance print for May. No high-impact Japanese data are scheduled for today.

The Tankan survey’s positive signal on business conditions may support modest yen buying if follow-through data confirm resilience. Analysts expect the figures to reinforce views that domestic demand remains stable even as external risks mount.

Other Economic Notes

Japan’s business sentiment improved sharply in the April-June quarter according to the latest Tankan survey, with large manufacturers showing renewed optimism. Persistent yen weakness continues to pressure import costs and household purchasing power despite the stronger corporate mood. Exporters benefit from the weaker currency while policymakers weigh the trade-off between growth support and imported inflation.

Broader themes center on whether sustained yen depreciation will force a faster policy adjustment than currently priced.

Global Macro News

The yen steadied near 40-year lows against mixed US data releases that offered little clarity on Federal Reserve timing. Eurozone inflation cooling allowed the euro to hold losses versus the yen, with EUR/JPY at 184.92. Global oil prices fell sharply as Brent crude declined 2.44%, easing some imported energy cost pressures for Japan.

<i>↓ p.2</i>