Japan Macro Daily(Beta Mode)

Yen Intervention Bets Intensify as Yields Spike

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Nikkei 225 | 70,474.96 | +0.59% |

| USD/JPY | 161.07 | -0.91% |

| EUR/JPY | 184.92 | -0.37% |

| GBP/JPY | 214.95 | -0.41% |

| Gold | 4,135.50 | +1.65% |

| Brent Crude | 71.54 | -0.04% |

| Bitcoin | 61,487.83 | +2.47% |

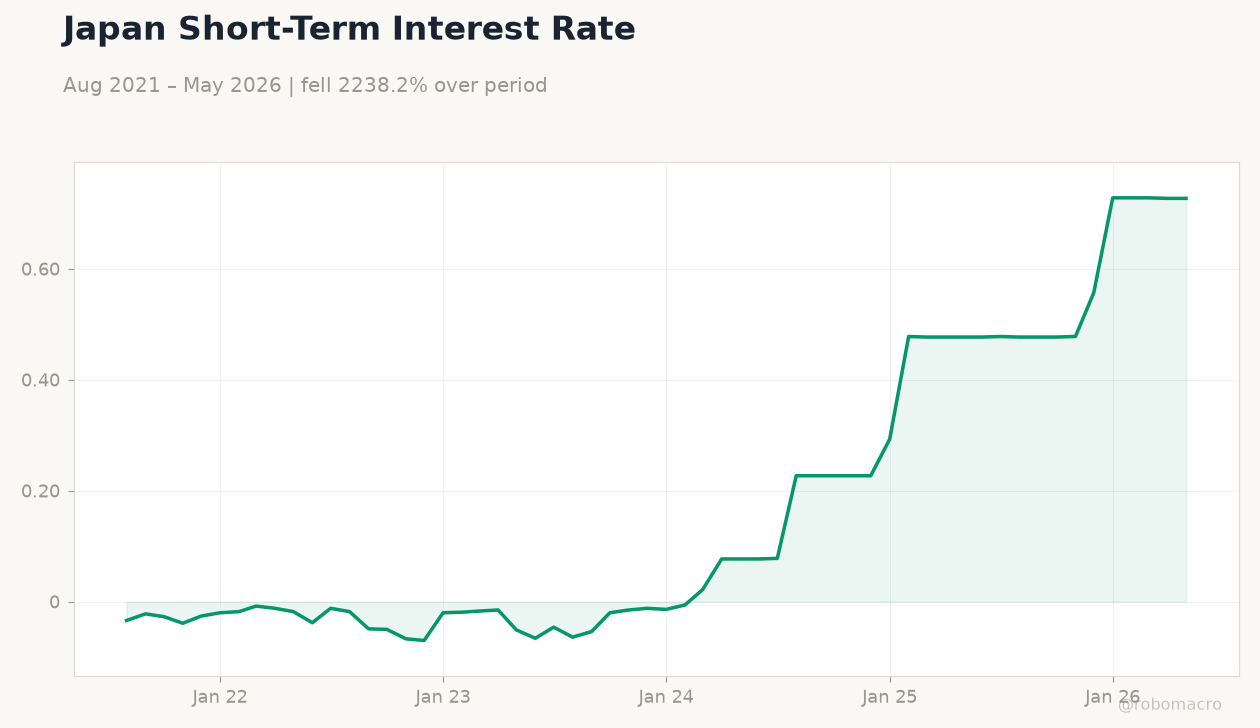

| Japan 2Y Govt Yield | 0.73% | +0.00% |

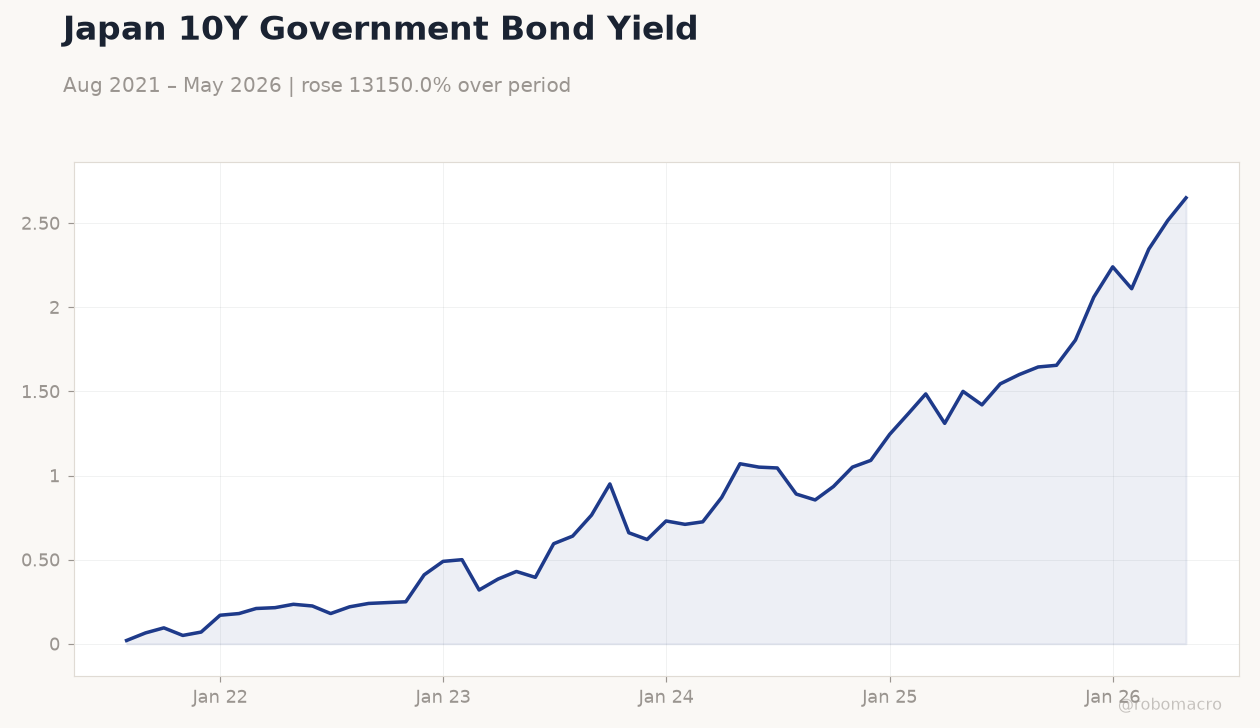

| Japan 10Y Govt Yield | 2.65% | +5.37% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

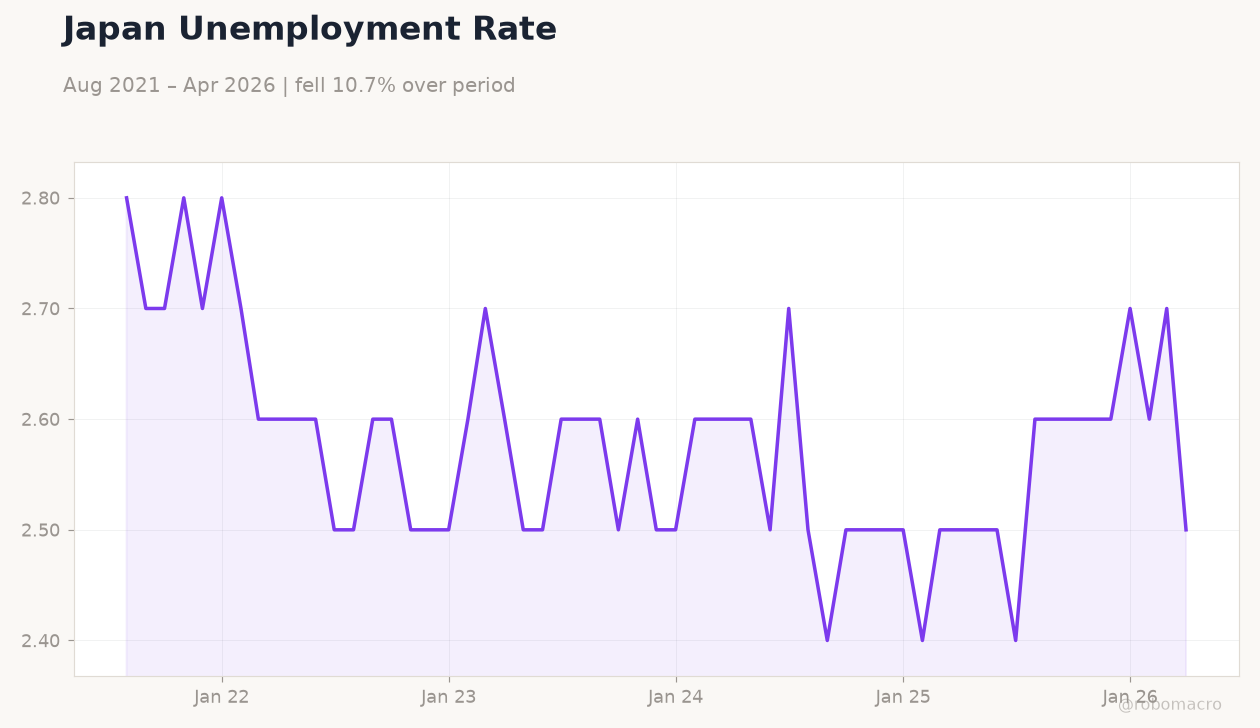

| Headline Unemployment Rate | 2.50 | 2.50 | 2.50 |

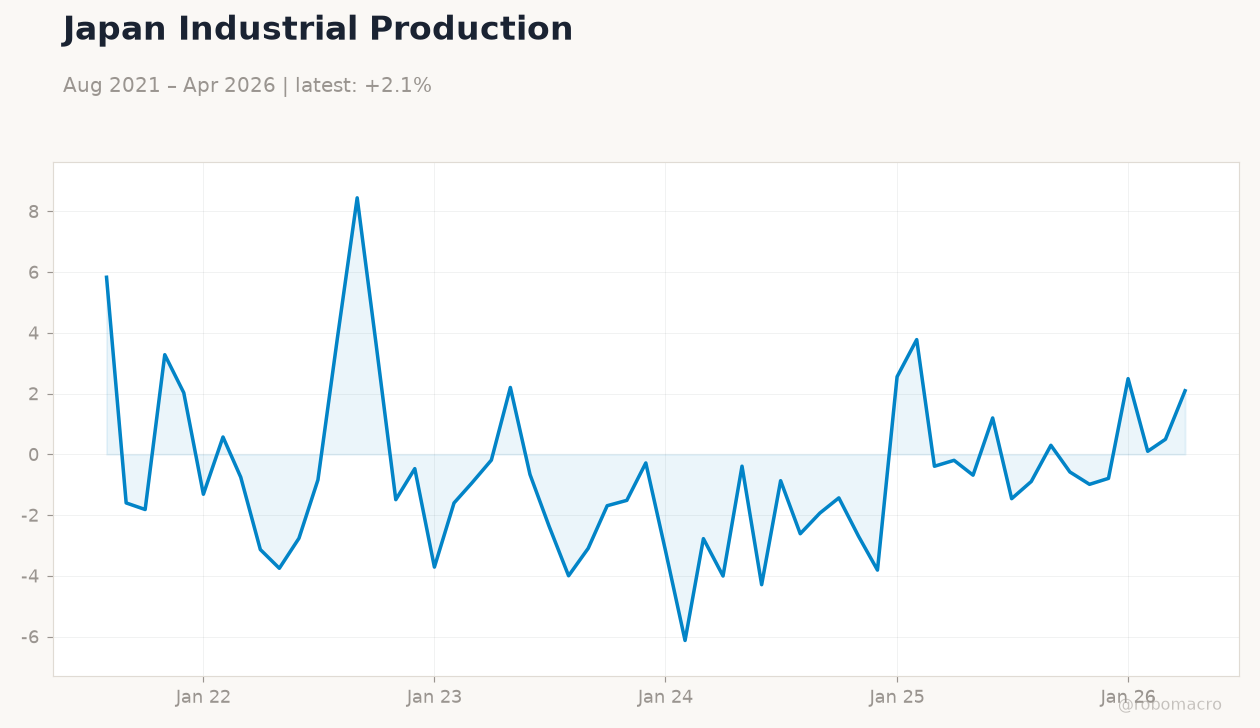

| Industrial Production Month-over-Month Preliminary | 0.50 | 1.10 | 0.50 |

| Consumer Confidence Index | 33.60 | 34 | 33.80 |

Japan 10Y Government Bond Yield | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65

Japan 10Y Government Bond Yield | Type: macro_line | 10Y Yield %: 2.65 (2026-05-01) | Range: 0.02–2.65 | Trend(6pt): 0.02,0.245,0.62,1.37,2.515,2.65

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Unemployment holds at 2.5% while industrial production misses forecasts at 0.5% MoM.

- Consumer confidence edges to 33.8, below 34 consensus, as yen intervention speculation intensifies.

- Nikkei rises 0.59% to 70,474.96 and USD/JPY drops 0.91% to 161.07 amid suspected MOF action.

Yesterday's Recap

Japan’s headline unemployment rate stayed at 2.5% on June 29, matching consensus. Industrial production rose only 0.5% MoM, missing the 1.1% forecast. Consumer confidence printed 33.8 on June 30 versus 34 expected.

The Nikkei 225 advanced 0.59% to close at 70,474.96 while USD/JPY fell 0.91% to 161.07 on suspected intervention. The 10-year JGB yield jumped 5.37% to 2.65% as markets priced higher BoJ normalisation odds. EUR/JPY declined 0.37% to 184.92 and GBP/JPY fell 0.41% to 214.95.

Gold climbed 1.65% to 4,135.50 while Brent crude edged 0.04% lower.

The Day Ahead

No major Japanese data releases are scheduled for July 2 or July 3. Markets will monitor ongoing yen moves after yesterday’s suspected MOF intervention. Traders await any follow-up comments from officials on the currency’s next red line near 162.50.

Equity flows may respond to global risk sentiment and US employment data due later this week. JGB trading desks will watch whether the sharp 10-year yield rise sustains or reverses.

Other Economic Notes

Tankan survey results showed business sentiment improving sharply in the April-June quarter. Currency-driven bankruptcies rose markedly as the weak yen squeezed importers and small firms. Inflation signals have strengthened according to Commerzbank analysis, supporting the case for earlier BoJ tightening.

A government panel member publicly advocated moderate rate hikes to address yen depreciation pressures. Yen-Rupee trade frameworks with India signal gradual de-dollarisation efforts that could influence regional capital flows.

Global Macro News

The euro tumbled against the yen on suspected Japanese intervention, highlighting coordinated defence tactics. US ISM manufacturing data missed expectations, adding to global growth concerns that indirectly support JGB demand. Middle East supply risks lifted Brent prices modestly and reinforced safe-haven bids for gold.

<i>↓ p.2</i>