Korea Macro Daily(Beta Mode)

KOSPI Edges Up, Won Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 5,781.20 | +0.31% |

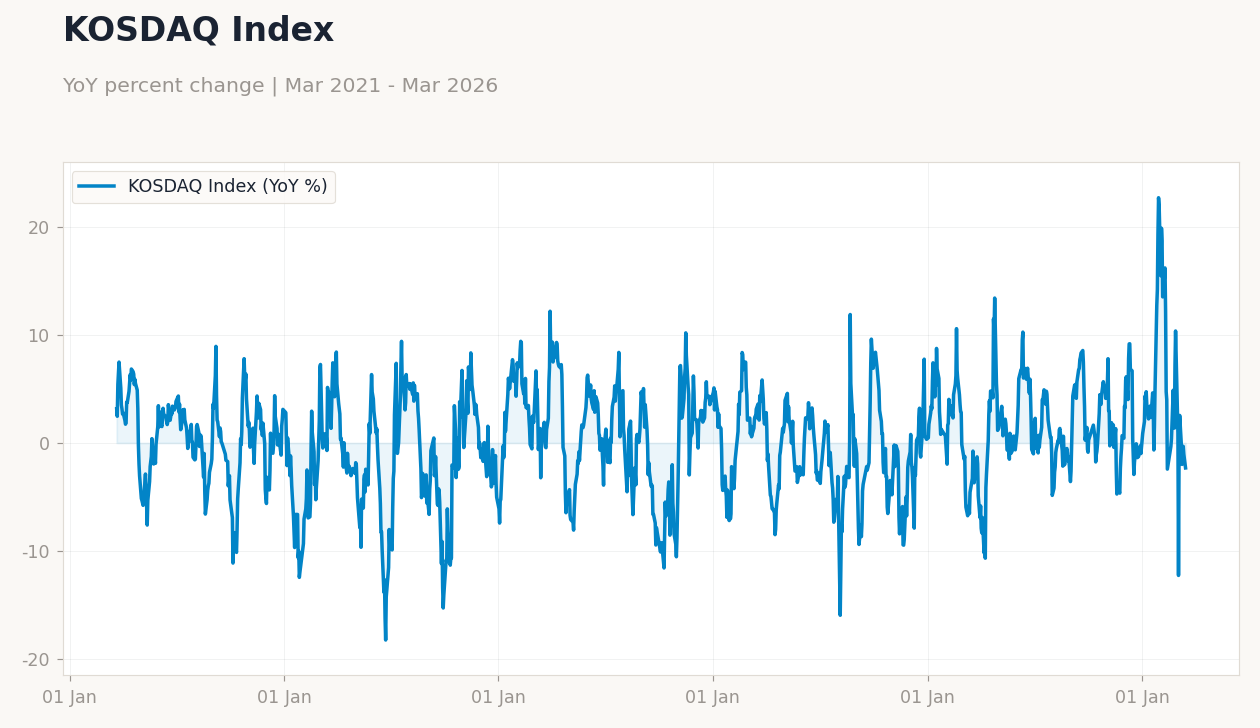

| KOSDAQ | 1,161.52 | +1.58% |

| USD/KRW | 1,504.83 | -0.03% |

| Samsung | 199,400.00 | -0.55% |

| SK Hynix | 1,007,000.00 | -0.59% |

| Brent Crude | 106.41 | -2.06% |

| Gold | 4,574.90 | -0.56% |

| Bitcoin | 70,276.18 | -0.35% |

| Korea Short-term Rate | 2.54% | +0.40% |

| Korea Long-term Rate | 3.61% | +3.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short vs Long Rates | Type: macro_line | Short-term Rate (%): 2.541 (2026-02-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.745,3.538,3.321,2.53,2.541 | Long-term Rate (%): 3.612 (2026-02-01) | Range: 1.905–4.272 | Trend(6pt): 2.041,3.64,3.86,3.07,3.366,3.612

Korea Short vs Long Rates | Type: macro_line | Short-term Rate (%): 2.541 (2026-02-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.745,3.538,3.321,2.53,2.541 | Long-term Rate (%): 3.612 (2026-02-01) | Range: 1.905–4.272 | Trend(6pt): 2.041,3.64,3.86,3.07,3.366,3.612

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-03-24) | |||

| Consumer Confidence Index | 112.10 | - | 17:00 |

| Thursday (2026-03-26) | |||

| Business Confidence Index | 72 | - | 17:00 |

- South Korean equities showed modest gains amid ongoing volatility concerns, with KOSPI up 0.31% and KOSDAQ rising 1.58%.

- USD/KRW dipped slightly by 0.03%, reflecting stable currency dynamics despite Middle East tensions.

- Bank of Korea pushes for bank-led won stablecoins as digital won pilots highlight subsidy and crypto liquidity contrasts.

Yesterday's Recap

South Korean markets closed with mild gains on March 20, as the KOSPI index rose 0.31% to 5,781.20, driven by selective buying in non-tech sectors amid easing global commodity pressures. KOSDAQ outperformed with a 1.58% increase to 1,161.52, boosted by small-cap resilience and positive sentiment in biotech and materials. USD/KRW edged down 0.03% to 1,504.83, supported by stable foreign inflows despite won wobbles from Middle East shockwaves.

Key stocks like Samsung fell 0.55% to 199,400.00 won, pressured by global demand concerns, while SK Hynix dropped 0.59% to 1,007,000.00 won amid memory chip price fluctuations. Korea's short-term rate rose 0.40% to 2.54%, aligning with steady monetary policy, and the long-term rate climbed 3.64% to 3.61%, reflecting inflation expectations. No major data releases occurred, allowing markets to focus on news of rising bank loan delinquency rates to 0.56% in January due to slowed bad-debt cleanup.

Overall, the session highlighted persistent 'Korea discount' from KOSPI volatility, with Brent crude falling 2.06% to 106.41 influencing export-oriented sectors.

The Day Ahead

Investors eye upcoming sentiment indicators that could signal consumer and business resilience amid global uncertainties. On March 24, the Consumer Confidence Index is due at 17:00 ET, with the previous reading at 112.1, potentially reflecting household spending trends. Thursday's Business Confidence Index release on March 26 at 17:00 ET follows a prior 72, offering insights into corporate outlook amid export challenges.

No events are scheduled for March 21 or 22, leaving room for markets to digest recent news on digital won pilots and petrochemical sector overhauls. These releases may influence expectations for Bank of Korea policy, especially with ongoing won stablecoin discussions. Broader Asia data, including Japanese inflation, could provide comparative context for Korean sentiment.

Other Economic Notes

South Korea's property market faces pressures as soaring prices and tight borrowing rules prompt earlier home gifting from parents to children, exacerbating generational wealth gaps. (cont...)