Korea Macro Daily(Beta Mode)

KOSPI Slips, Rates Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 5,438.87 | -0.40% |

| KOSDAQ | 1,141.51 | +0.43% |

| USD/KRW | 1,508.06 | -0.02% |

| Samsung | 180,100.00 | +0.00% |

| SK Hynix | 933,000.00 | +0.00% |

| Brent Crude | 105.32 | -2.49% |

| Gold | 4,524.30 | +3.40% |

| Bitcoin | 66,543.45 | +0.34% |

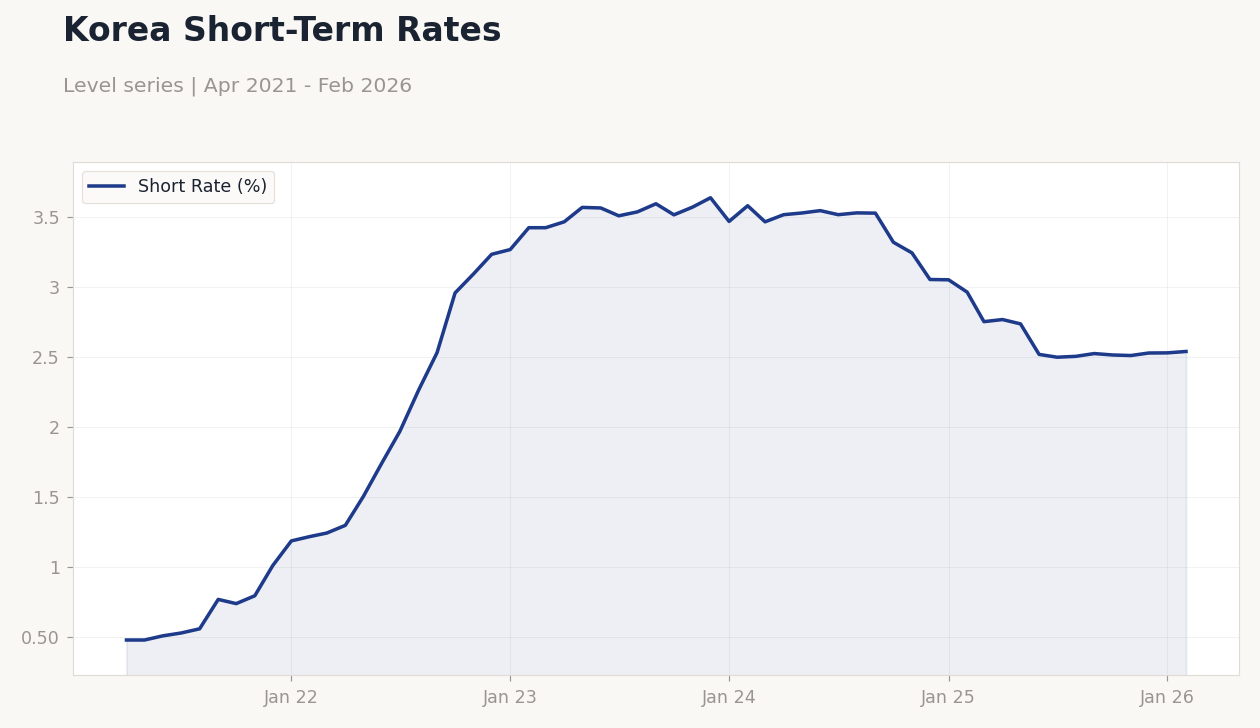

| Korea Short-term Rate | 2.54% | +0.40% |

| Korea Long-term Rate | 3.61% | +3.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-Term Rates | Type: macro_line | Short Rate (%): 2.541 (2026-02-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.745,3.538,3.321,2.53,2.541

Korea Short-Term Rates | Type: macro_line | Short Rate (%): 2.541 (2026-02-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.745,3.538,3.321,2.53,2.541

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-01) | |||

| Exports Year-over-Year | 29 | - | 20:00 |

| S&P Global Manufacturing PMI Index | 51.10 | - | 20:30 |

| Inflation Rate Year-over-Year | 2 | - | 19:00 |

- KOSPI dipped 0.40% amid mixed equity moves, while long-term rates surged 3.64%.

- Upcoming data includes exports, PMI, and inflation, key for BoK outlook.

- New BoK governor nomination signals policy continuity amid global tensions.

Yesterday's Recap

Korean markets showed mixed performance on March 28, with the KOSPI closing at 5,438.87 after a 0.40% decline, pressured by global risk-off sentiment. In contrast, the KOSDAQ rose 0.43% to 1,141.51, buoyed by small-cap gains. USD/KRW edged down 0.02% to 1,508.06, reflecting slight won stability despite dollar strength elsewhere.

Samsung Electronics held flat at 180,100.00, while SK Hynix remained unchanged at 933,000.00, indicating semiconductor sector resilience. Korea's short-term rate increased 0.40% to 2.54%, and the long-term rate jumped 3.64% to 3.61%, signaling hawkish repricing. No major data releases occurred, but the lack of events kept focus on external factors like falling Brent crude at 105.32 after a 2.49% drop.

Overall, markets digested broader commodity shifts, with gold rising 3.40% to 4,524.30 as a safe haven.

The Day Ahead

On March 29, markets anticipate low-event trading, but eyes turn to near-term releases including exports year-over-year on March 31 at 20:00 ET, with previous at 29%, impacting trade-sensitive sectors. The S&P Global Manufacturing PMI follows at 20:30 ET on March 31, prior reading 51.1, crucial for gauging export-driven growth. Inflation rate year-over-year arrives on April 1 at 19:00 ET, previous at 2%, influencing BoK rate expectations.

These medium-impact indicators could sway KOSPI and won if they signal weakening momentum. No events are slated for March 30, providing a brief pause before data flow. Traders watch for any spillover from global news on semiconductor supply chains.

Other Economic Notes

Broader Korean themes highlight export reliance, with semiconductors from Samsung and SK Hynix driving growth amid AI demand, though global chip disruptions from Middle East tensions pose risks. Fiscal stimulus signals from political leaders aim to counter consumer weakness, supporting retail and domestic demand. North Korea-related geopolitical news, including escapes and treaties with Belarus, adds uncertainty to regional stability, potentially affecting investor sentiment in export markets.