Korea Macro Daily(Beta Mode)

Kospi Dips, Won Pressured

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 5,438.87 | -0.40% |

| KOSDAQ | 1,141.51 | +0.43% |

| USD/KRW | 1,516.40 | +0.53% |

| Samsung | 180,100.00 | +0.00% |

| SK Hynix | 933,000.00 | +0.00% |

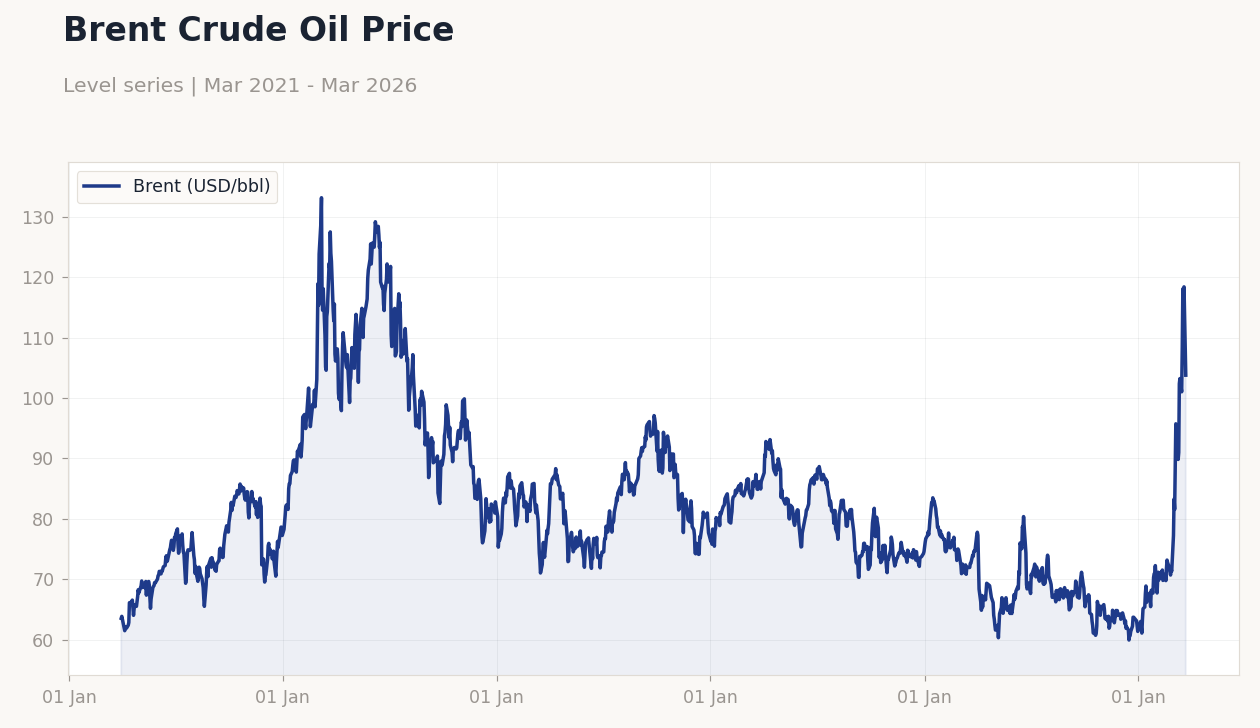

| Brent Crude | 108.70 | -3.44% |

| Gold | 4,540.00 | +1.07% |

| Bitcoin | 66,572.02 | +0.94% |

| Korea Short-term Rate | 2.54% | +0.40% |

| Korea Long-term Rate | 3.61% | +3.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent (USD/bbl): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8

Brent Crude Oil Price | Type: macro_line | Brent (USD/bbl): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-03-31) | |||

| Exports Year-over-Year | 29 | - | 16:00 |

| S&P Global Manufacturing PMI Index | 51.10 | - | 16:30 |

| Wednesday (2026-04-01) | |||

| Inflation Rate Year-over-Year | 2 | - | 15:00 |

- KOSPI fell 0.40% amid Asia-wide declines from Middle East tensions, while KOSDAQ rose 0.43% on tech gains.

- USD/KRW climbed 0.53% to 1,516.40, driven by safe-haven dollar flows and oil volatility.

- South Korea nominates BIS official Shin Hyun Song as new BOK governor, pointing to steady policy approach.

Yesterday's Recap

Korean markets ended mixed on March 29, with the KOSPI declining 0.40% to 5,438.87, leading Asia-Pacific losses as the Middle East war entered its fifth week, per reports. This pressured equities amid geopolitical risks, though the KOSDAQ advanced 0.43% to 1,141.51, supported by resilient small-cap tech stocks. USD/KRW increased 0.53% to 1,516.40, reflecting dollar strength from conflict-driven safe-haven demand.

Samsung Electronics remained flat at 180,100.00, and SK Hynix was unchanged at 933,000.00, indicating stable but cautious semiconductor sentiment. Brent crude dropped 3.44% to 108.70, offering some relief to importers like Korea, while gold rose 1.07% to 4,540.00 and Bitcoin gained 0.94% to 66,572.02. Korea's short-term rate edged up to 2.54%, with a 0.40% change, and the long-term rate increased to 3.61%, up 3.64%, amid inflation concerns.

No economic data was released, but markets responded to global headlines on Iran tensions potentially disrupting chip supplies. Trading volumes were subdued, with foreign outflows adding to equity weakness.

The Day Ahead

March 30 features no Korean data releases, shifting focus to near-term events. Exports year-over-year for March, scheduled at 16:00 ET on March 31, follows a previous 29% rise, which could underscore strength in semiconductors and shipbuilding if trends persist. S&P Global Manufacturing PMI at 16:30 ET on March 31, last at 51.1, may indicate ongoing expansion above 50, supporting views on industrial recovery.

Inflation rate year-over-year for March, due at 15:00 ET on April 1, builds on the prior 2% figure and could influence BOK decisions if it surprises upward. Investors will watch these for insights into trade dynamics, manufacturing health, and price pressures, alongside Middle East developments affecting oil and supply chains.

Other Economic Notes

South Korea's export-dependent economy is vulnerable to Middle East conflicts, which could interrupt semiconductor supply chains essential for firms like Samsung and SK Hynix, as highlighted in reports on Gulf disruptions. (cont...)