Korea Macro Daily(Beta Mode)

Record Surplus Fuels Stock Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 5,494.78 | +0.82% |

| KOSDAQ | 1,036.73 | -1.02% |

| USD/KRW | 1,478.50 | -1.95% |

| Samsung | 210,500.00 | +7.12% |

| SK Hynix | 1,014,000.00 | +10.70% |

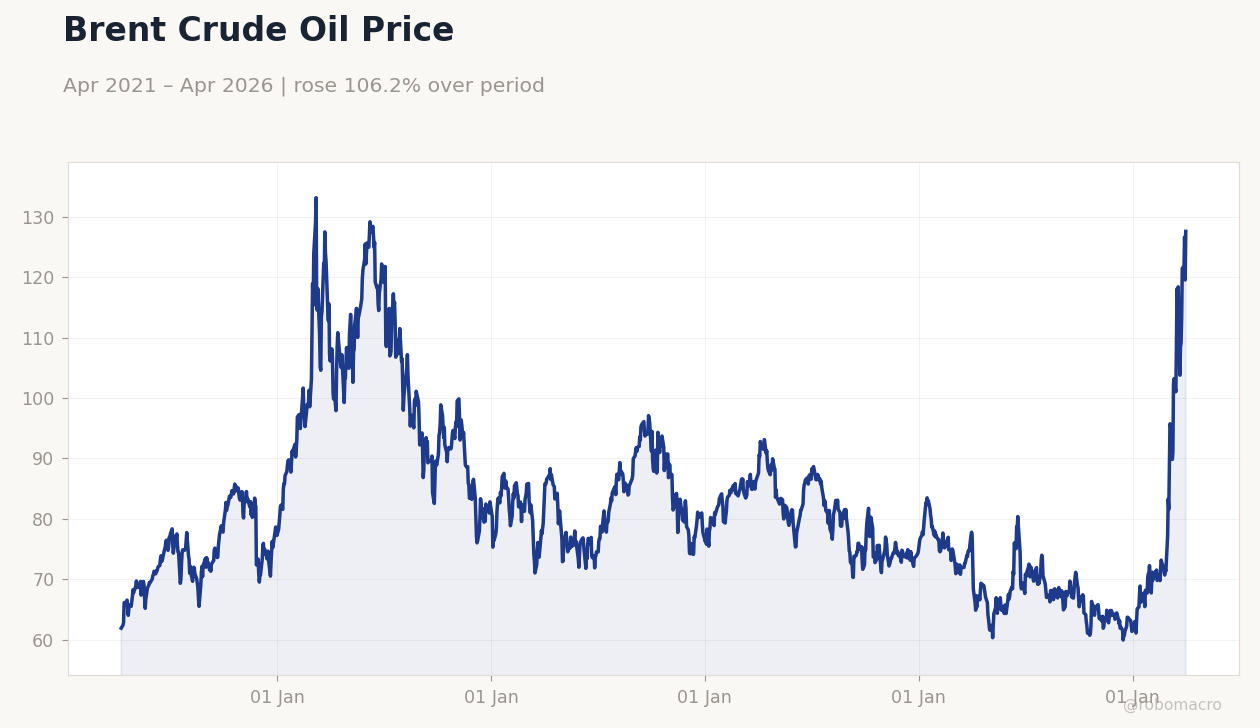

| Brent Crude | 96.27 | -11.90% |

| Gold | 4,745.30 | +1.89% |

| Bitcoin | 71,349.70 | -0.82% |

| Korea Short-term Rate | 2.54% | +0.40% |

| Korea Long-term Rate | 3.61% | +3.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent Price ($/bbl): 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 61.89,113.4,87.86,77.27,127.6

Brent Crude Oil Price | Type: macro_line | Brent Price ($/bbl): 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 61.89,113.4,87.86,77.27,127.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-09) | |||

| Central Bank Interest Rate Decision | 2.50 | 2.50 | 17:00 |

- Korea posted its largest-ever February current account surplus, boosting won and equities amid relief from Iran ceasefire.

- BOK nominee downplays stagflation risks, while polls expect rates held at 2.5% despite oil shocks and inflation concerns.

- KOSPI rose 0.82% led by Samsung (+7.12%) and SK Hynix (+10.70%), with USD/KRW dropping 1.95% on improved sentiment.

Yesterday's Recap

Korean markets rallied on geopolitical relief and strong economic data, with KOSPI closing at 5,494.78 after a 0.82% gain, driven by semiconductor heavyweights. Samsung Electronics surged 7.12% to 210,500.00, fueled by positive memory chip demand outlook, while SK Hynix jumped 10.70% to 1,014,000.00 on AI-related supply constraints. KOSDAQ dipped 1.02% to 1,036.73, weighed by small-cap volatility.

USD/KRW fell 1.95% to 1,478.50, reflecting won strength from ceasefire news and export optimism. The Bank of Korea reported February's current account surplus hit a record high, supporting currency gains. Korea short-term rate edged up 0.40% to 2.54%, and long-term rate rose 3.64% to 3.61%, signaling persistent inflation pricing.

No major data releases occurred yesterday, but prior export strength continued to underpin market resilience.

The Day Ahead

Tomorrow features the Bank of Korea's interest rate decision at 17:00 ET on 2026-04-09, with consensus expecting a hold at 2.5% amid war-driven uncertainty and oil price risks. Markets will scrutinize forward guidance for hints on inflation and growth outlooks. No events are scheduled for today, allowing focus on global cues like US inflation data.

The decision could influence USD/KRW and KOSPI, especially if dovish tones emerge on stagflation concerns. Expect volatility in semiconductor stocks like Samsung and SK Hynix based on any policy signals.

Other Economic Notes

Korea's export-driven economy benefited from February's record current account surplus, led by semiconductors and autos, highlighting resilience despite global slowdowns. Broader themes include easing Chinese visa rules potentially boosting tourism inflows, though Southeast Asian rivals and geopolitical tensions pose risks. The Ministry of Economy and Finance held an FX market meeting, vowing bold measures if won volatility becomes excessive.

KB Financial joined the Bank of Korea's Project Hangang for deposit token payments, signaling innovation in financial systems. Recent data underscores export rebound, with semiconductors driving gains to US and China markets.