Korea Macro Daily(Beta Mode)

Korean Stocks Top 6 Trillion Won Milestone

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 6,475.63 | -0.00% |

| KOSDAQ | 1,203.84 | +2.51% |

| USD/KRW | 1,473.95 | -0.41% |

| Samsung | 219,500.00 | -2.23% |

| SK Hynix | 1,222,000.00 | -0.24% |

| Brent Crude | 101.84 | -3.31% |

| Gold | 4,694.10 | -0.60% |

| Bitcoin | 76,895.99 | -2.24% |

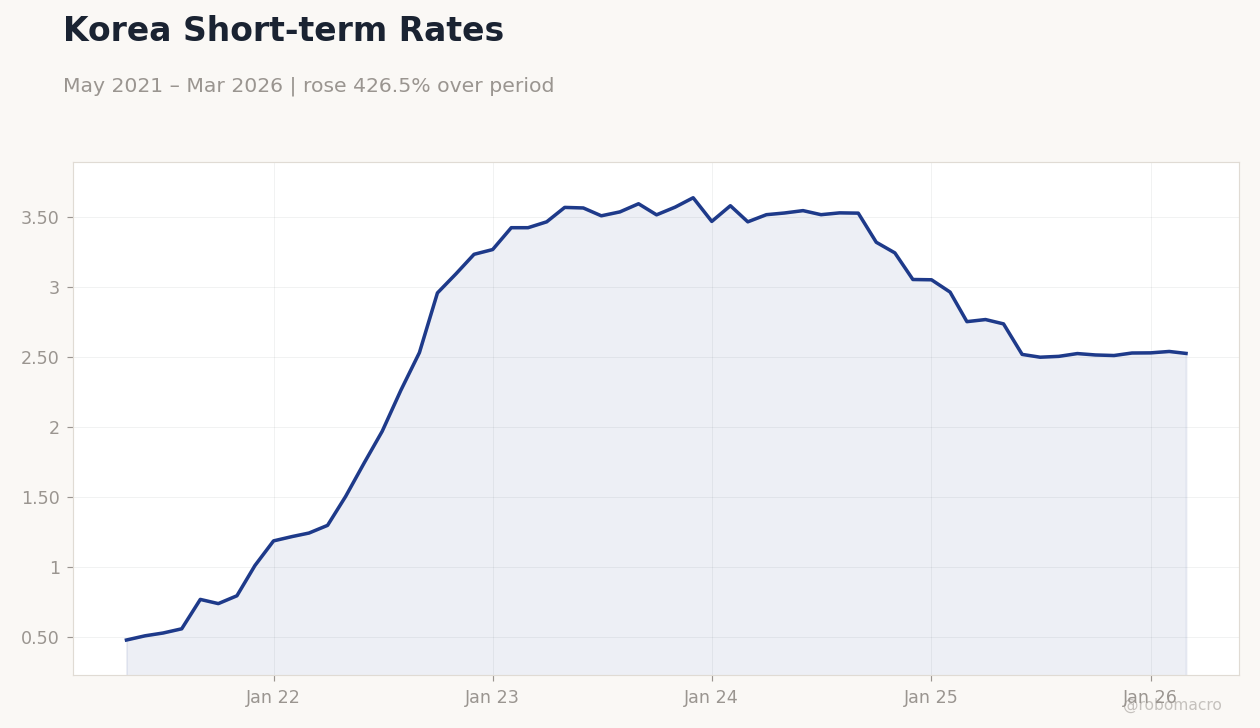

| Korea Short-term Rate | 2.53% | -0.55% |

| Korea Long-term Rate | 3.73% | +3.21% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 71 | - | - |

Korea Short-term Rates | Type: macro_line | Short Rate (%): 2.527 (2026-03-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.971,3.596,3.245,2.531,2.527

Korea Short-term Rates | Type: macro_line | Short Rate (%): 2.527 (2026-03-01) | Range: 0.48–3.639 | Trend(6pt): 0.48,1.971,3.596,3.245,2.531,2.527

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-30) | |||

| Exports Year-over-Year | 48.30 | 45 | 16:00 |

- Korean stock market cap tops 6,000 trillion won for first time, fueled by tech sector strength.

- Won strengthens on export optimism, while OECD cuts potential growth rate to 1.7%.

- BoK nominee prioritizes price stability; calls emerge for green monetary policies.

Yesterday's Recap

The Business Confidence Index was released with no actual value reported, maintaining medium impact amid ongoing economic assessments. KOSPI closed flat at 6,475.63 with a 0.00% change, reflecting mixed sentiment after a three-day record run and a slight dip. KOSDAQ surged 2.51% to 1,203.84, boosted by small-cap gains in semiconductors.

USD/KRW declined 0.41% to 1,473.95, supported by export resilience despite foreign dividend outflows hovering above 1,480. Samsung Electronics fell 2.23% to 219,500.00, while SK Hynix dipped 0.24% to 1,222,000.00 despite raised target prices to 2.34 million won, highlighting 91% upside potential. Korea's long-term rate rose 3.21% to 3.73%, contrasting with a 0.55% drop in short-term rate to 2.53%.

The Day Ahead

Upcoming events focus on Thursday's Exports Year-over-Year data, expected at 45% consensus versus 48.3% previous, impacting trade balance views. No major releases today or tomorrow, allowing markets to digest recent milestones like the 6,000 trillion won market cap. Attention turns to potential semiconductor export trends, with SK Hynix's HBM demand in spotlight.

Broader events include monitoring bad loan rises at top banks, now over 5 trillion won amid Middle East risks. Fiscal debates from IMF warnings may influence sentiment ahead of weekend.

Other Economic Notes

South Korea's potential growth rate has slumped to 1.7% per OECD, signaling structural challenges despite global investment banks lifting overall growth outlooks. Bad loans at the top four banks surpassed 5 trillion won, exacerbated by Middle East geopolitical risks affecting financial stability. Investments like Novo Holdings' 100 billion won in biohealth underscore sector diversification amid export-driven recovery.

Korean market cap hit 6,000 trillion won, but margin debt risks loom. Strong Q1 GDP growth, the fastest in over five years, was driven by chip exports.

Global Macro News

Global investment banks have raised South Korea's growth forecasts, countering the OECD's lowered potential rate amid strong semiconductor exports decoupling from China slowdowns. U.S. (cont...)