Korea Macro Daily(Beta Mode)

KOSPI Surges on Chip Strength

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 7,844.01 | +2.63% |

| KOSDAQ | 1,176.93 | -0.20% |

| USD/KRW | 1,492.07 | +0.15% |

| Samsung | 290,500.00 | +2.29% |

| SK Hynix | 1,949,000.00 | -1.37% |

| Brent Crude | 106.55 | +0.87% |

| Gold | 4,655.40 | -0.90% |

| Bitcoin | 81,393.84 | +2.67% |

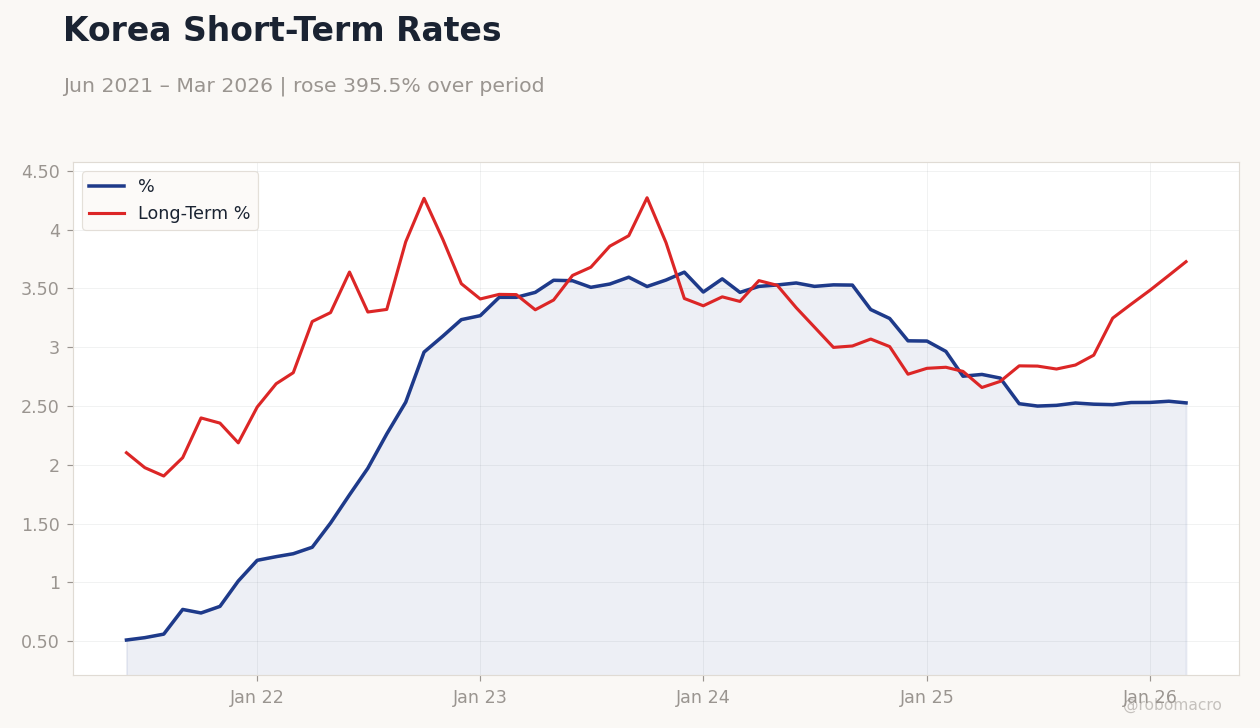

| Korea Short-term Rate | 2.53% | -0.55% |

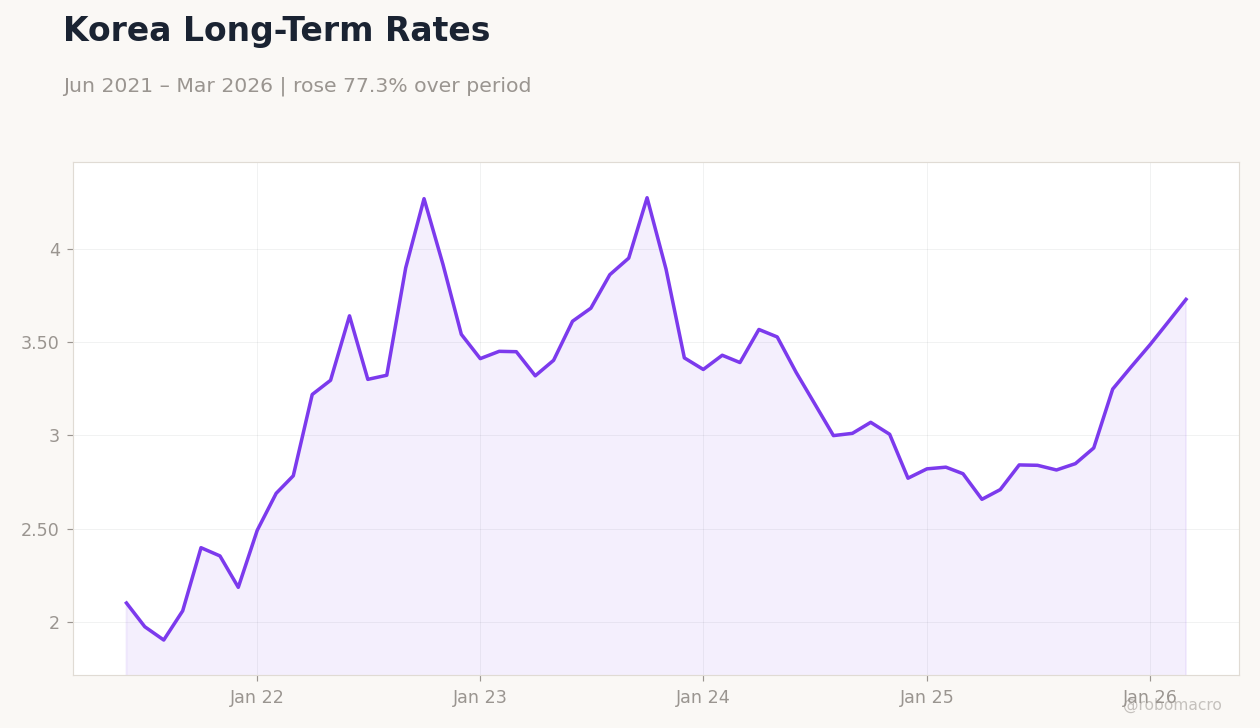

| Korea Long-term Rate | 3.73% | +3.21% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-Term Rates | Type: macro_line | %: 2.527 (2026-03-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.527 | Long-Term %: 3.728 (2026-03-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.728

Korea Short-Term Rates | Type: macro_line | %: 2.527 (2026-03-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.527 | Long-Term %: 3.728 (2026-03-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.728

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-21) | |||

| Consumer Confidence Index | 99.20 | - | 17:00 |

- KOSPI climbed 2.63% to 7,844.01, led by semiconductor gains with Samsung up 2.29%.

- USD/KRW rose 0.15% to 1,492.07 amid mixed currency sentiment.

- KOSDAQ dipped 0.20% to 1,176.93, contrasting broader equity rally.

Yesterday's Recap

South Korean markets displayed strong equity performance, with the KOSPI advancing 2.63% to 7,844.01, driven by semiconductor sector momentum. Samsung Electronics gained 2.29% to 290,500.00 won, while SK Hynix declined 1.37% to 1,949,000.00 won, reflecting varied dynamics in chip demand. The KOSDAQ index fell 0.20% to 1,176.93, weighed down by smaller tech stocks.

In currency trading, USD/KRW increased 0.15% to 1,492.07, as markets balanced robust exports against inflation concerns. Korea's short-term rate dropped 0.55% to 2.53%, consistent with easing bets, while the long-term rate climbed 3.21% to 3.73%, indicating yield curve shifts. No significant data releases took place, but positive sentiment arose from reports of strong chip demand and export orders in shipbuilding.

Export sectors like semiconductors bolstered the session amid global volatility.

The Day Ahead

No economic events are scheduled for today. The next notable release is the Consumer Confidence Index on May 21 at 17:00 ET, a medium-impact indicator that may shed light on consumer spending amid ongoing inflation. Markets could react to any previews of this data, potentially affecting retail and consumption-related stocks.

Attention will also center on semiconductor developments, including possible Samsung Electronics union actions regarding pay talks. Trading may remain subdued without major catalysts, though global news could influence the won or equities. Unscheduled Bank of Korea statements might impact short-term rates.

Other Economic Notes

South Korea's economy is riding an AI investment wave, enhancing chip exports and fueling stock gains in Seoul. However, a proposed AI tax dividend has raised market worries, leading to a 5.1% KOSPI drop upon announcement, highlighting tensions between wealth distribution and stability. Exports continue to drive growth, with semiconductors at the forefront due to global demand, but Samsung's union threats to exit pay negotiations pose risks to operations.

These factors underscore the balance between tech-led expansion and domestic challenges like labor disputes and fiscal proposals.