Korea Macro Daily(Beta Mode)

Samsung Strike Risks Weigh on KOSPI

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 7,271.66 | -3.25% |

| KOSDAQ | 1,084.36 | -2.41% |

| USD/KRW | 1,496.48 | +0.28% |

| Samsung | 276,000.00 | +0.18% |

| SK Hynix | 1,745,000.00 | +0.00% |

| Brent Crude | 105.45 | -5.24% |

| Gold | 4,546.20 | +0.89% |

| Bitcoin | 77,422.67 | +0.88% |

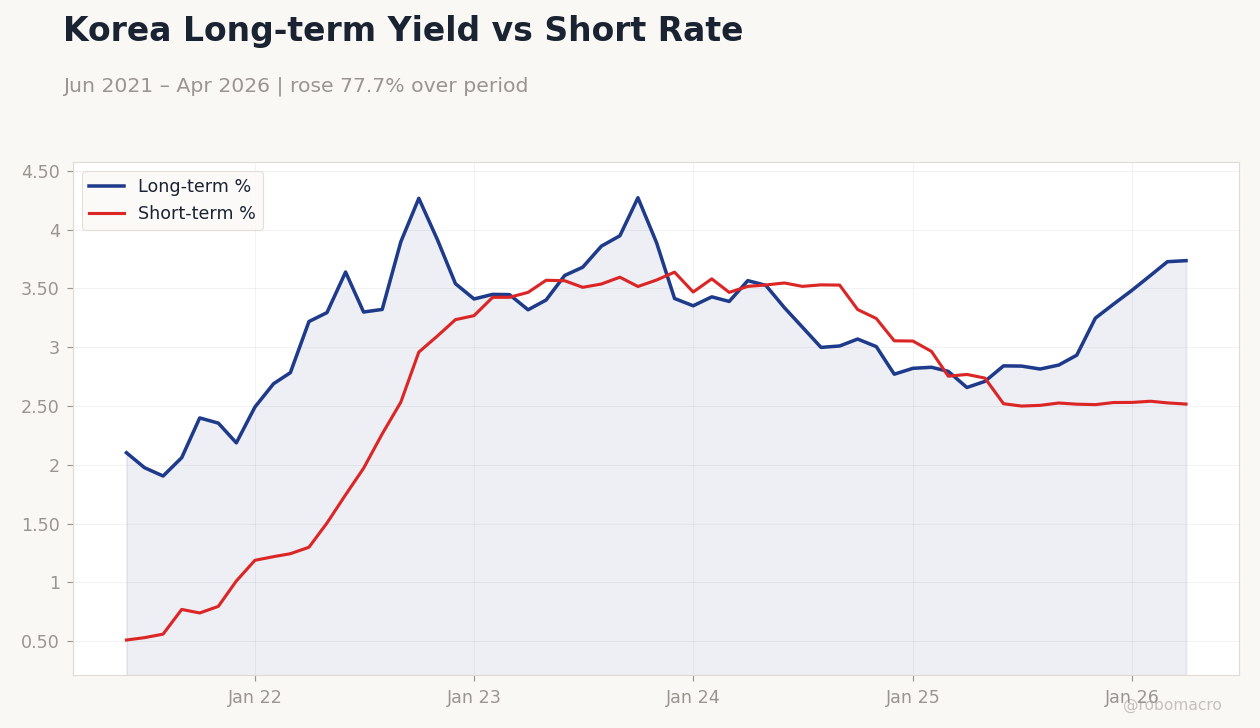

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Long-term Yield vs Short Rate | Type: macro_line | Long-term %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737 | Short-term %: 2.517 (2026-04-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.517

Korea Long-term Yield vs Short Rate | Type: macro_line | Long-term %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737 | Short-term %: 2.517 (2026-04-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-21) | |||

| Consumer Confidence Index | 99.20 | - | 13:00 |

- KOSPI drops 3.25% to 7,271.66 as Samsung strike risks mount and regional equities slide

- USD/KRW climbs to 1,496.48 amid foreign outflows and oil-driven volatility

- BOK flags 0.5pp GDP hit from Samsung strike while base rate holds at 2.52%

Yesterday's Recap

Korean equities posted steep losses with KOSPI falling 3.25% to 7,271.66 and KOSDAQ declining 2.41% to 1,084.36. Foreign selling intensified pressure on the won, lifting USD/KRW 0.28% to 1,496.48. The Bank of Korea warned that the ongoing Samsung Electronics strike could subtract 0.5 percentage points from annual growth.

Long-term treasury yields rose 0.24% to 3.74% as global bond rates climbed. Brent crude fell 5.24% to 105.45 while gold advanced 0.89%. Parallel weakness in Japanese markets, with the Nikkei dropping below 60,000, amplified the regional equity selloff.

No economic data releases occurred yesterday.

The Day Ahead

Markets will focus on the May Consumer Confidence Index due at 13:00 tomorrow, following April’s 99.2 reading. A softer print would reinforce growth concerns tied to the Samsung strike and support expectations for policy easing. FX authorities have signaled readiness to act as the won trades above 1,500 per dollar.

Investors will also monitor any updates from recent Japan-South Korea energy cooperation talks. Semiconductor names remain in focus given Samsung and SK Hynix positioning. No MPC members are scheduled to speak.

Other Economic Notes

Household debt nearing 2,000 trillion won continues to draw regulatory attention for pre-emptive measures. Biotech equities extended declines on rate sensitivity and disappointing earnings. Semiconductor export shipments rose 18% year-on-year in early-May data, cushioning the trade balance.

North Korea’s exchange rate jumped 80% to its weakest level since 2008, adding regional uncertainty. Authorities reiterated readiness to intervene in FX markets to curb excessive won volatility.

Global Macro News

Japanese and Korean stocks declined together, with the Nikkei falling below 60,000 on shared growth worries. Soaring global government bond yields lifted Korean treasury rates in tandem. Japan and South Korea deepened energy ties at the Andong summit, supporting longer-term supply security.

<i>↓ p.2</i>