Korea Macro Daily(Beta Mode)

Chip Stocks Rally as Confidence Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 7,208.95 | -0.86% |

| KOSDAQ | 1,056.07 | -2.61% |

| USD/KRW | 1,506.40 | -0.10% |

| Samsung | 299,500.00 | +8.51% |

| SK Hynix | 1,940,000.00 | +11.17% |

| Brent Crude | 104.90 | -0.11% |

| Gold | 4,543.50 | +0.27% |

| Bitcoin | 77,702.25 | +0.32% |

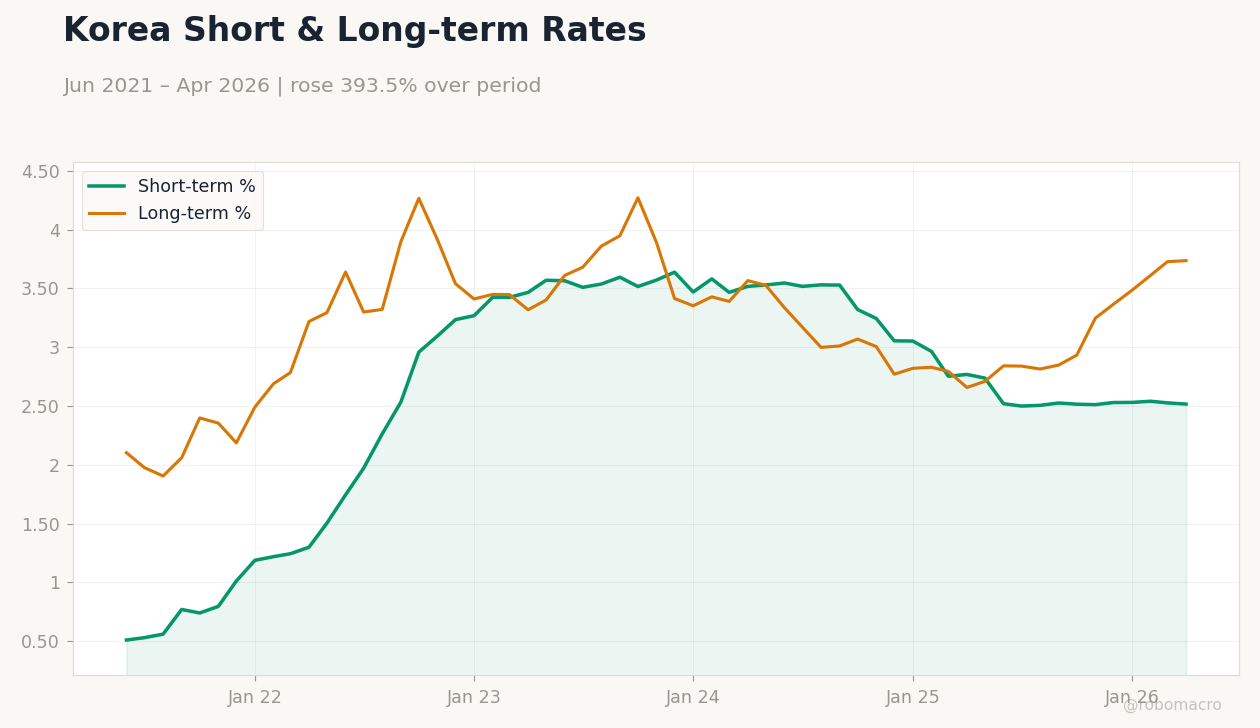

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 99.20 | - | 106.10 |

Korea Industrial Production YoY | Type: macro_line | YoY %: 1.898 (2026-03-01) | Range: -12.45–10.23 | Trend(6pt): 9.814,-1.743,4.803,4.732,3.88,1.898

Korea Industrial Production YoY | Type: macro_line | YoY %: 1.898 (2026-03-01) | Range: -12.45–10.23 | Trend(6pt): 9.814,-1.743,4.803,4.732,3.88,1.898

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Consumer confidence surged to 106.1 from 99.2, signaling stronger household sentiment.

- KOSPI slipped 0.86% to 7,208.95 while Samsung and SK Hynix surged on AI demand.

- USD/KRW steadied at 1,506.40 as foreign selling eased and BoK held base rate at 2.52%.

Yesterday's Recap

South Korea’s Consumer Confidence Index jumped to 106.1, well above the prior 99.2 reading and reflecting improved household optimism. Equity markets closed mixed: the KOSPI declined 0.86% to 7,208.95 while the KOSDAQ fell 2.61% to 1,056.07 amid broader regional weakness. Semiconductor names outperformed sharply, with Samsung Electronics rising 8.51% to 299,500 won and SK Hynix climbing 11.17% to 1,940,000 won on sustained AI memory demand.

The Korean won finished at 1,506.40 against the dollar, down just 0.10% after earlier tests above 1,510. Korea’s short-term rate held at 2.52% while the long-term rate edged up 0.24% to 3.74%, tracking global bond yield increases. Producer price data showed renewed upward pressure, keeping BoK officials alert to second-round inflation risks.

The Day Ahead

Today’s domestic calendar is empty, leaving markets to focus on external drivers and corporate updates. May manufacturing PMI is expected later in the week and will test whether the recent export strength persists. FX authorities have signaled readiness to intervene should the won weaken further past 1,510.

Global bond markets remain the dominant influence on Korean yields. Investors will also monitor any follow-through commentary from Samsung after the recent labor agreement that lifted shares.

Other Economic Notes

AI-related semiconductor exports continue to support headline growth even as the broader economy faces headwinds from the Samsung strike, which the BoK estimates could subtract 0.5 percentage points from GDP. Rising global government bond yields have pushed Korean treasury rates higher, tightening financial conditions despite the unchanged policy rate. The combination of strong chip demand and a persistently weak won has created a divergence between equity performance and currency valuation that policymakers are watching closely.

Global Macro News

Japanese and Korean equities declined together, with the Nikkei falling below 60,000 amid shared semiconductor and export concerns. Soaring global bond yields lifted Korean treasury rates and weighed on rate-sensitive sectors. North Korea’s exchange rate weakened sharply, hitting its lowest level since 2008 and highlighting regional currency stress.

<i>↓ p.2</i>