Korea Macro Daily(Beta Mode)

Hawkish BoK Steadies Won After FX Warning

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 7,847.71 | +0.41% |

| KOSDAQ | 1,161.13 | +4.99% |

| USD/KRW | 1,517.53 | +0.87% |

| Samsung | 292,500.00 | -2.34% |

| SK Hynix | 1,941,000.00 | +0.05% |

| Brent Crude | 100.21 | -3.22% |

| Gold | 4,523.20 | +0.05% |

| Bitcoin | 77,283.91 | +0.39% |

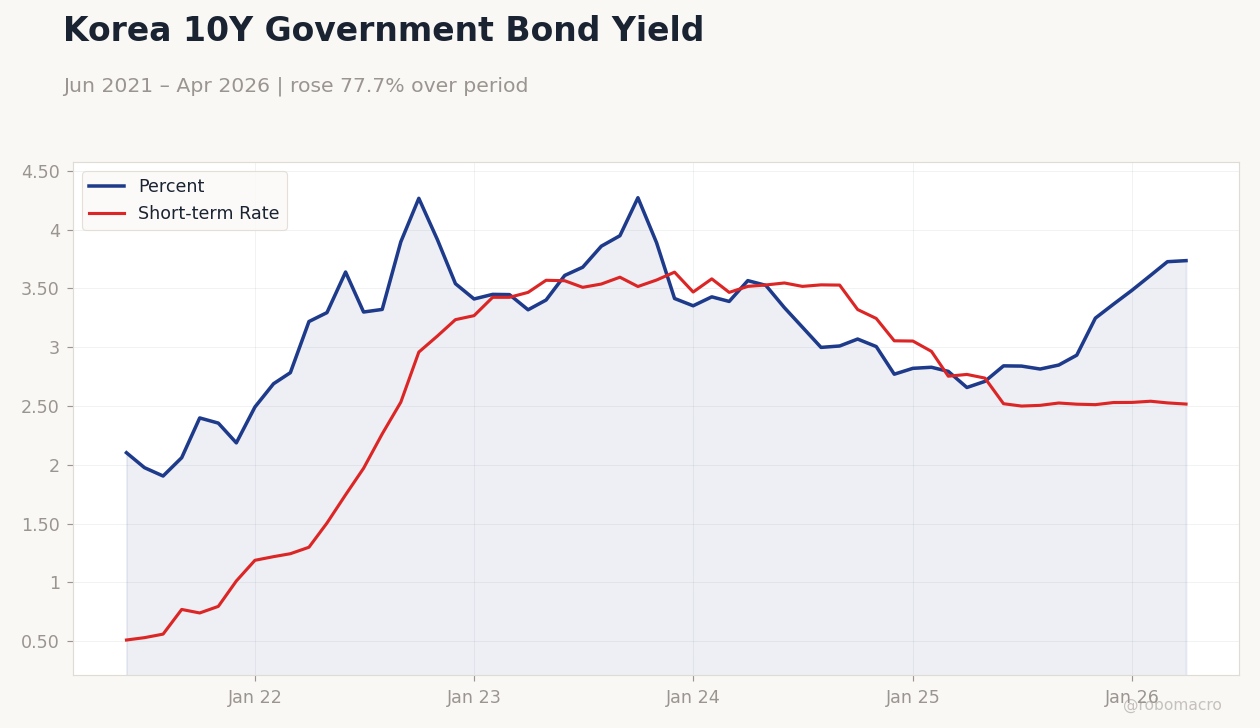

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea 10Y Government Bond Yield | Type: macro_line | Percent: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737 | Short-term Rate: 2.517 (2026-04-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.517

Korea 10Y Government Bond Yield | Type: macro_line | Percent: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737 | Short-term Rate: 2.517 (2026-04-01) | Range: 0.51–3.639 | Trend(6pt): 0.51,2.263,3.517,3.055,2.541,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-05-26) | |||

| Business Confidence Index | 74 | - | 17:00 |

| Thursday (2026-05-28) | |||

| Central Bank Interest Rate Decision | 2.50 | 2.50 | 21:00 |

| Monday (2026-06-01) | |||

| Exports Year-over-Year | 48 | 48 | 20:00 |

| S&P Global Manufacturing PMI Index | 53.60 | - | 20:30 |

| Inflation Rate Year-over-Year | 2.60 | - | 19:00 |

- Hawkish BoK tilt and verbal FX intervention lift KRW support despite foreign outflows from Samsung and SK Hynix.

- KOSDAQ jumps 4.99% while KOSPI edges up 0.41% as semiconductor names show mixed performance amid AI demand.

- USD/KRW climbs 0.87% to 1,517.53, prompting authorities to flag excessive moves and signal potential market action.

Yesterday's Recap

Korean equities closed mixed with KOSPI at 7,847.71, up 0.41%, and KOSDAQ surging 4.99% to 1,161.13 on selective semiconductor buying. USD/KRW rose 0.87% to 1,517.53 as foreign investors sold 46 trillion won in local shares, targeting Samsung and SK Hynix. Samsung fell 2.34% to 292,500 won while SK Hynix gained 0.05%.

Korea short-term rates eased 0.40% to 2.52% and long-term rates rose 0.24% to 3.74%. Authorities issued a verbal warning that won moves had become excessive and would trigger intervention if needed. No major data releases occurred yesterday, leaving markets focused on BoK signals and export momentum.

The Day Ahead

Markets will monitor the Business Confidence Index release at 17:00 today for any shift in corporate sentiment. The BoK is expected to hold the base rate at 2.5% on Thursday, with the committee voting to maintain current policy. Next week brings exports year-over-year data and S&P Global Manufacturing PMI, both due Monday, followed by inflation figures on Tuesday.

Traders will track any follow-through from the recent FX warning and semiconductor earnings updates. Global risk sentiment and Brent crude moves at 100.21 will also influence KRW flows.

Other Economic Notes

Foreign investors have offloaded 6.6 billion dollars from Samsung and SK Hynix amid profit-taking after strong AI-driven gains. Samsung C&T secured a 2.1 trillion won contract for Apgujeong District 4 redevelopment, supporting construction sector activity. BTS fandom spending is projected to add 0.35 percentage points to GDP by 2040 through sustained consumption and tourism.

Semiconductor capacity expansions at Samsung and SK Hynix continue to underpin export resilience despite global AI-related uncertainties.

Global Macro News

Brent crude declined 3.22% to 100.21, easing imported inflation pressures for Korea’s energy-intensive economy. Gold held steady near 4,523.20, reflecting persistent safe-haven demand amid global uncertainty. Bitcoin rose 0.39% to 77,283.91, offering limited spillover to risk assets.

<i>↓ p.2</i>