Korea Macro Daily(Beta Mode)

BoK Holds at 2.5% as Business Confidence Jumps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,228.70 | +2.25% |

| KOSDAQ | 1,133.13 | -3.36% |

| USD/KRW | 1,495.88 | -0.64% |

| Samsung | 299,500.00 | -2.44% |

| SK Hynix | 2,289,000.00 | +2.05% |

| Brent Crude | 92.48 | -1.92% |

| Gold | 4,527.30 | +1.79% |

| Bitcoin | 73,600.01 | -1.00% |

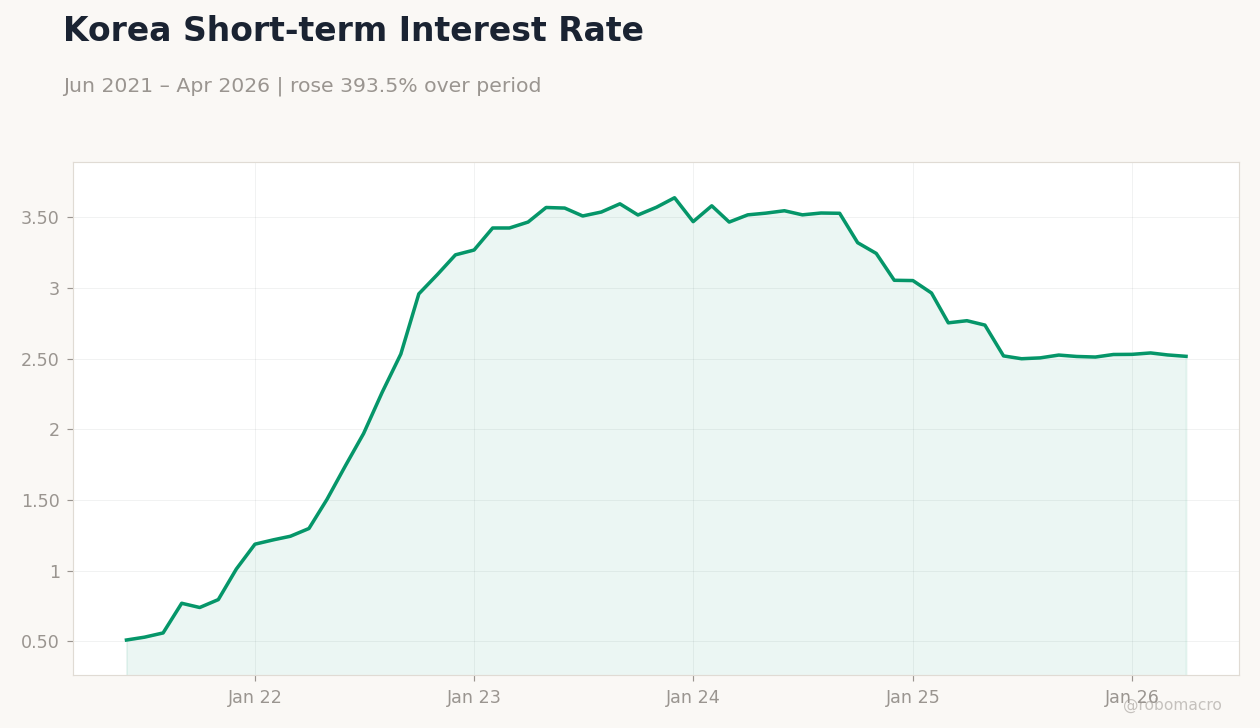

| Korea Short-term Rate | 2.52% | -0.40% |

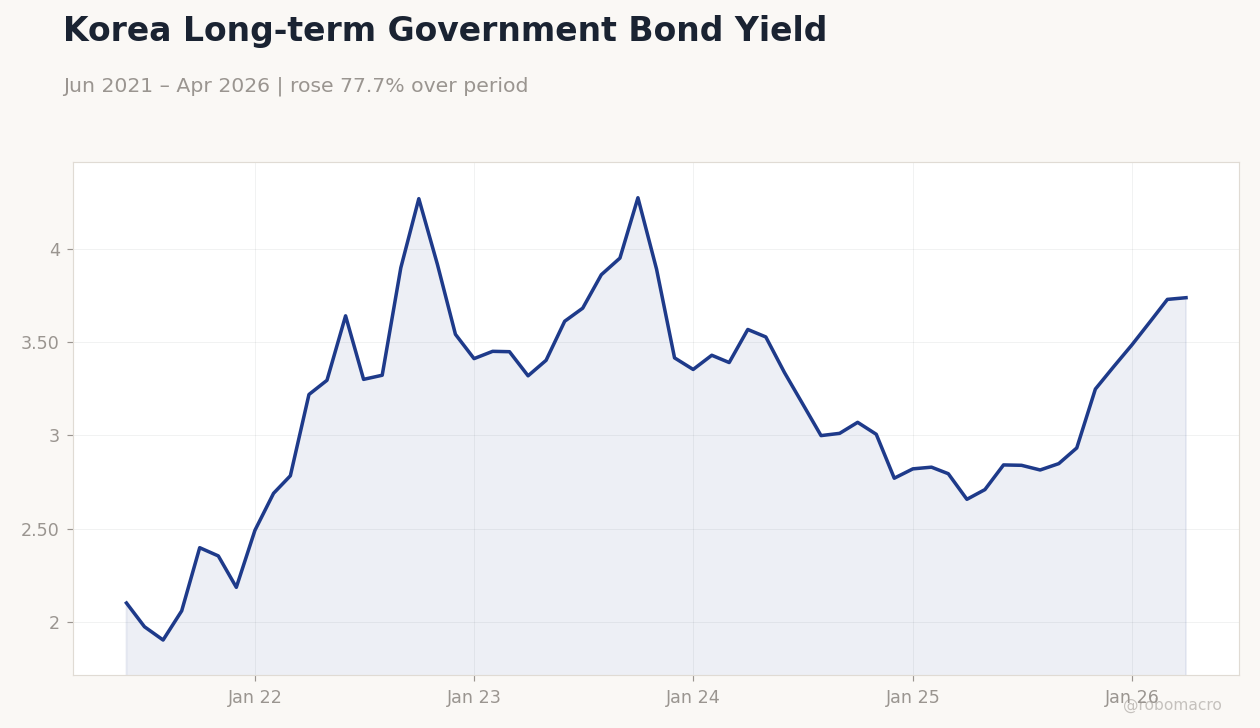

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 74 | - | 80 |

| Central Bank Interest Rate Decision | 2.50 | 2.50 | 2.50 |

Korea Long-term Government Bond Yield | Type: macro_line | 10Y Yield %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737

Korea Long-term Government Bond Yield | Type: macro_line | 10Y Yield %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 2.103,3.322,4.272,2.771,3.612,3.737

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank of Korea keeps base rate at 2.5% while flagging persistent inflation risks.

- Business Confidence Index rises sharply to 80 from 74, signaling improving sentiment.

- KOSPI climbs 2.25% to 8,228.70 on semiconductor demand, though KOSDAQ drops 3.36%.

Yesterday's Recap

The Bank of Korea held its policy rate at 2.5% as expected, citing elevated inflation pressures and Middle East uncertainty. The committee noted that growth had improved modestly yet remained cautious on price stability. Business Confidence Index printed at 80, well above the prior 74, reflecting stronger corporate optimism.

KOSPI advanced 2.25% to 8,228.70, supported by foreign buying in memory chips, while KOSDAQ fell 3.36% to 1,133.13. USD/KRW eased 0.64% to 1,495.88 despite ongoing geopolitical tensions. Korea’s short-term rate stood at 2.52% and the long-term rate rose to 3.74%.

SK Hynix gained 2.05% on AI-related demand, offsetting Samsung’s 2.44% decline.

The Day Ahead

No scheduled data releases or Bank of Korea speakers appear on the calendar for 28 May. Markets will monitor any follow-up commentary from MPC members on inflation risks. Equity flows into semiconductors may continue to influence KOSPI direction.

Attention will also turn to global oil prices given Brent’s 1.92% drop to 92.48. The absence of domestic events leaves external developments as the main driver for won and yields.

Other Economic Notes

Export growth remains anchored in semiconductors, with SK Hynix entering the trillion-dollar valuation club on HBM strength. Samsung workers secured record bonuses after the union dropped strike plans, supporting household income and consumption. The won’s persistence above 1,500 highlights structural pressures from energy imports and global rate differentials.

Industrial Bank of Korea’s new Vietnam subsidiary approval signals continued regional expansion by Korean lenders.

Global Macro News

Renewed US-Iran tensions lifted safe-haven demand for gold, which rose 1.79% to 4,527.30. AI-driven memory demand lifted East Asian chip stocks, benefiting Korean exporters. Brent crude fell 1.92% amid signs of easing supply concerns in the Middle East.

Bitcoin declined 1.00% to 73,600.01, tracking broader risk sentiment. <i>↓ p.2</i>