Korea Macro Daily(Beta Mode)

Korea CPI Tops Forecasts at 3.1%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | nan | +nan% |

| KOSDAQ | 1,050.03 | -2.30% |

| USD/KRW | 1,515.30 | +0.56% |

| Samsung | 360,500.00 | +3.30% |

| SK Hynix | 2,360,000.00 | -0.13% |

| Brent Crude | 96.17 | +1.25% |

| Gold | 4,517.50 | +0.95% |

| Bitcoin | 66,485.77 | -6.78% |

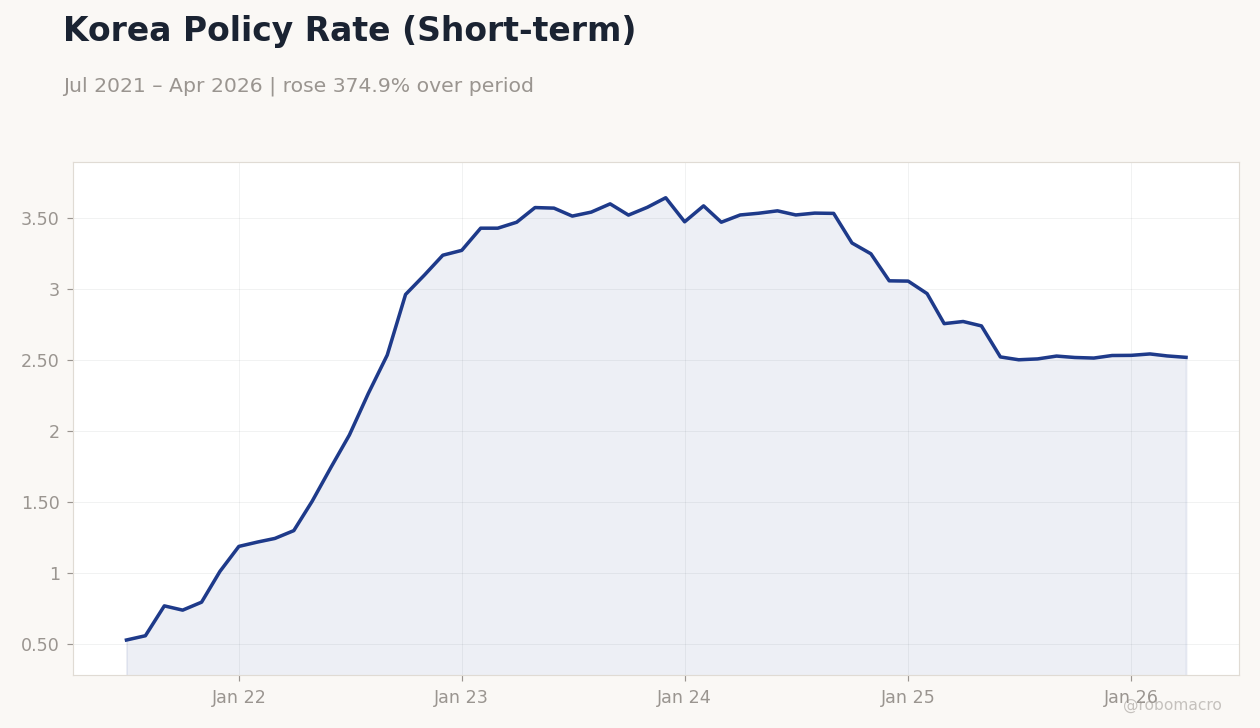

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.60 | 3 | 3.10 |

Korea Policy Rate (Short-term) | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Korea Policy Rate (Short-term) | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- May CPI rose to 3.1% y/y, above consensus, prompting Citi to lift its 2026 inflation forecast.

- KOSDAQ fell 2.30% while Samsung gained 3.30%; USD/KRW climbed 0.56% to 1,515.30.

- BoK base rate holds at 2.52% with export momentum supporting a patient policy stance.

Yesterday's Recap

South Korea’s May inflation rate printed at 3.1% y/y, exceeding the 3.0% consensus and prior 2.6% reading, driven by fresh food and energy components. The hotter print triggered immediate revisions from Citi, which raised its full-year inflation outlook. Equity markets showed mixed moves as KOSDAQ declined 2.30% to 1,050.03 while Samsung Electronics advanced 3.30%.

The won weakened, with USD/KRW rising 0.56% to 1,515.30. Short-term rates eased 0.40% to 2.52% while long-term yields rose 0.24% to 3.74%. Export data released alongside confirmed continued semiconductor-led gains, reinforcing external demand resilience despite the domestic price surprise.

The Day Ahead

The calendar is empty today and tomorrow, leaving markets to digest yesterday’s inflation surprise without fresh data releases. Focus will remain on export orders and semiconductor shipment trends already in train. Margin debt at a record 38 trillion won adds a layer of leverage risk if volatility rises.

Any comments from BoK officials on the 3.1% print could shift rate expectations quickly. Investors will also monitor global chip demand signals from Taiwan’s Computex for clues on SK Hynix and Samsung momentum.

Other Economic Notes

South Korea’s export engine continues firing, with May shipments expanding at the fastest pace in over four decades on AI-driven chip demand. Manufacturing PMI climbed to 54.8, signaling sustained factory expansion and supporting the won’s fundamental backdrop. Record margin loans near 38 trillion won highlight elevated retail leverage as KOSPI flirts with 8,800–9,000 levels.

Stablecoin initiatives by Shinhan and other banks reflect ongoing financial innovation amid won internationalization efforts. These dynamics collectively point to a growth-inflation mix that favors external resilience over rapid domestic easing.

Global Macro News

Global chip demand remains robust, underpinning Korea’s export outperformance and differentiating it from softer regional peers. <i>↓ p.2</i>