Korea Macro Daily(Beta Mode)

Won Hits 17-Year Low as KOSPI Falls 5.5%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,160.59 | -5.54% |

| KOSDAQ | 1,002.44 | -4.50% |

| USD/KRW | 1,559.42 | +1.72% |

| Samsung | 329,000.00 | -6.40% |

| SK Hynix | 2,070,000.00 | -9.92% |

| Brent Crude | 93.09 | -2.04% |

| Gold | 4,365.30 | -2.47% |

| Bitcoin | 61,744.32 | +1.44% |

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Korea Short-term Policy Rate | Type: macro_line | Short-term Rate (%): 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-10) | |||

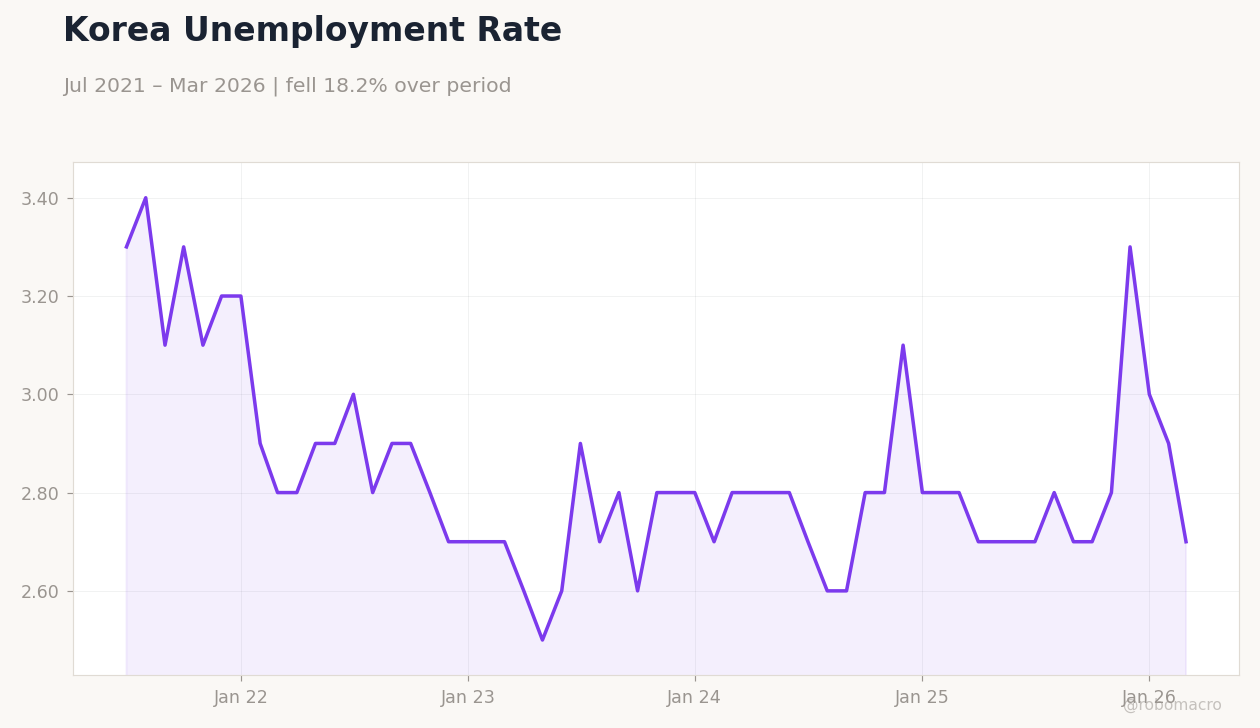

| Headline Unemployment Rate | 2.80 | - | 19:00 |

- South Korea announced measures to curb speculative won trading and stabilize the currency after USD/KRW breached 1,560.

- KOSPI plunged 5.54% to 8,160.59 while KOSDAQ fell 4.50%, led by Samsung (-6.40%) and SK Hynix (-9.92%).

- Inflation rose to 3.1% as fuel prices surged, complicating policy amid heavy foreign equity outflows.

Yesterday's Recap

Seoul markets suffered sharp losses as foreign investors sold aggressively across equities and the won. KOSPI closed at 8,160.59, down 5.54%, while KOSDAQ dropped 4.50% to 1,002.44. USD/KRW jumped 1.72% to 1,559.42, its weakest level in 17 years.

Samsung and SK Hynix led the decline with drops of 6.40% and 9.92%, respectively. The government unveiled steps to deter speculative trading in the won and announced readiness to intervene. Korea’s short-term rate eased 0.40pp to 2.52% while the long-term rate rose 0.24pp to 3.74%.

Brent crude fell 2.04% to 93.09, offering limited relief on the inflation front.

The Day Ahead

Markets will monitor the June 10 release of the headline unemployment rate, last reported at 2.8%. Officials are expected to provide further details on the new foreign-exchange stabilization tools. Equity traders will watch semiconductor order flows and any additional comments from the Ministry of Economy and Finance.

Bond markets will focus on supply auctions and foreign demand after yesterday’s yield steepening. The won remains the primary variable for both local and regional sentiment.

Other Economic Notes

Export-oriented growth faces headwinds from the stronger dollar and softer semiconductor prices. Foreign selling has accelerated since the won began underperforming regional peers. Inflation at 3.1% adds pressure on household purchasing power while limiting the scope for rate relief.

Authorities are prioritizing currency stability over immediate growth support. Semiconductor exposure remains the dominant driver of both equity performance and external balances.

Global Macro News

Asian equities fell broadly, with South Korea’s decline the steepest in the region. The Indonesian rupiah also hit record lows, underscoring dollar strength across emerging markets. Japan’s policy outlook continues to point toward gradual tightening, supporting further yen appreciation pressure.

<i>↓ p.2</i>