Korea Macro Daily(Beta Mode)

Seoul Acts to Curb Won Speculation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,160.59 | -5.54% |

| KOSDAQ | 1,002.44 | -4.50% |

| USD/KRW | 1,526.67 | -0.42% |

| Samsung | 329,000.00 | -6.40% |

| SK Hynix | 2,070,000.00 | -9.92% |

| Brent Crude | 94.44 | +1.45% |

| Gold | 4,350.50 | +0.31% |

| Bitcoin | 63,247.03 | +0.01% |

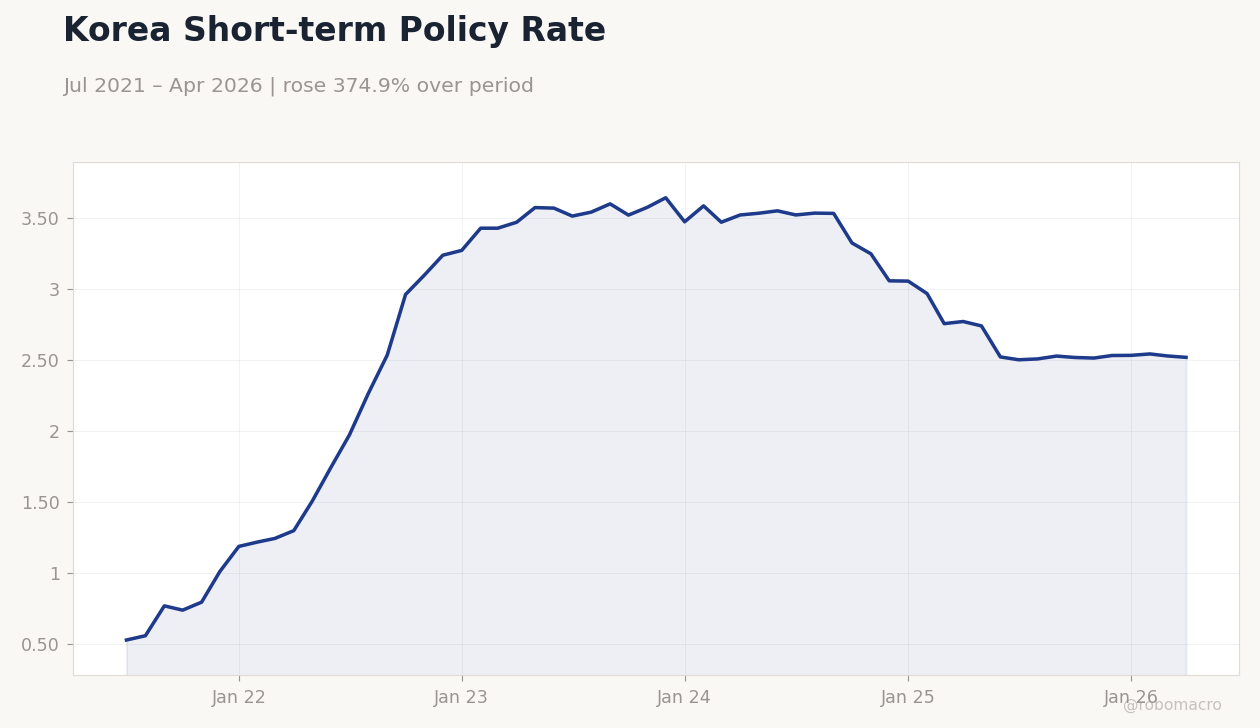

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-10) | |||

| Headline Unemployment Rate | 2.80 | - | 19:00 |

- Seoul unveiled measures to curb speculative won trading and summoned banks after USD/KRW hit 1,552 intraday.

- KOSPI fell 5.54% and KOSDAQ 4.50% as Samsung and SK Hynix dropped 6.40% and 9.92% on fading AI momentum.

- Headline inflation reached 3.1% amid surging fuel prices while the BoK base rate stayed at 2.52%.

Yesterday's Recap

South Korean authorities announced inspections of speculative won positions and ordered banks to tighten risk management after the currency briefly touched 2009-era lows. Regulators pledged to stamp out market disruption, prompting the won to close stronger with USD/KRW down 0.42% at 1,526.67. Equity markets sold off sharply, with the KOSPI losing 5.54% to 8,160.59 and the KOSDAQ falling 4.50% to 1,002.44 as semiconductor names led declines.

Samsung closed at 329,000 won and SK Hynix at 2,070,000 won after Nvidia’s new memory deal failed to offset broader AI-trade rotation. Korea’s short-term rate eased 0.40% to 2.52% while the long-term rate rose 0.24% to 3.74%. Fuel-driven price pressures lifted headline inflation to 3.1%, keeping real-rate calculations in focus for policymakers.

The Day Ahead

Markets will monitor the June 10 unemployment release due at 19:00 ET for any signs of labor-market softening. Traders await further statements from the Financial Supervisory Service on enforcement of the new anti-speculation rules. Equity desks will track semiconductor order flows after yesterday’s heavy volume in Samsung and SK Hynix.

Bond participants will watch whether the 3.74% long-term yield attracts fresh foreign inflows following the won’s rebound. Regional currency moves in Indonesia and elsewhere will remain a backdrop for won direction.

Other Economic Notes

Export-oriented growth remains tied to memory-chip cycles, leaving the economy exposed to sudden shifts in global AI spending. Authorities continue to balance currency-stability goals against the risk that tighter bank scrutiny could reduce market liquidity. Rising fuel costs have pushed inflation above the BoK’s comfort zone, complicating any near-term easing path even as growth momentum slows.

Global Macro News

Asian equities fell across the board, with South Korea’s decline the steepest as investors rotated out of last year’s AI leaders. Nvidia’s fresh memory-chip agreement with SK Hynix offered limited support after the broader sector pullback. The Indonesian rupiah also hit record lows, underscoring regional pressure on emerging-market currencies.

<i>↓ p.2</i>