Korea Macro Daily(Beta Mode)

FX Probes Intensify as Won Volatility Spikes

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,096.93 | +8.18% |

| KOSDAQ | 967.81 | +6.19% |

| USD/KRW | 1,525.81 | -0.20% |

| Samsung | 302,500.00 | -6.06% |

| SK Hynix | 2,048,000.00 | -7.54% |

| Brent Crude | 95.45 | +4.37% |

| Gold | 4,087.30 | -4.05% |

| Bitcoin | 61,322.88 | -0.52% |

| Korea Short-term Rate | 2.52% | -0.40% |

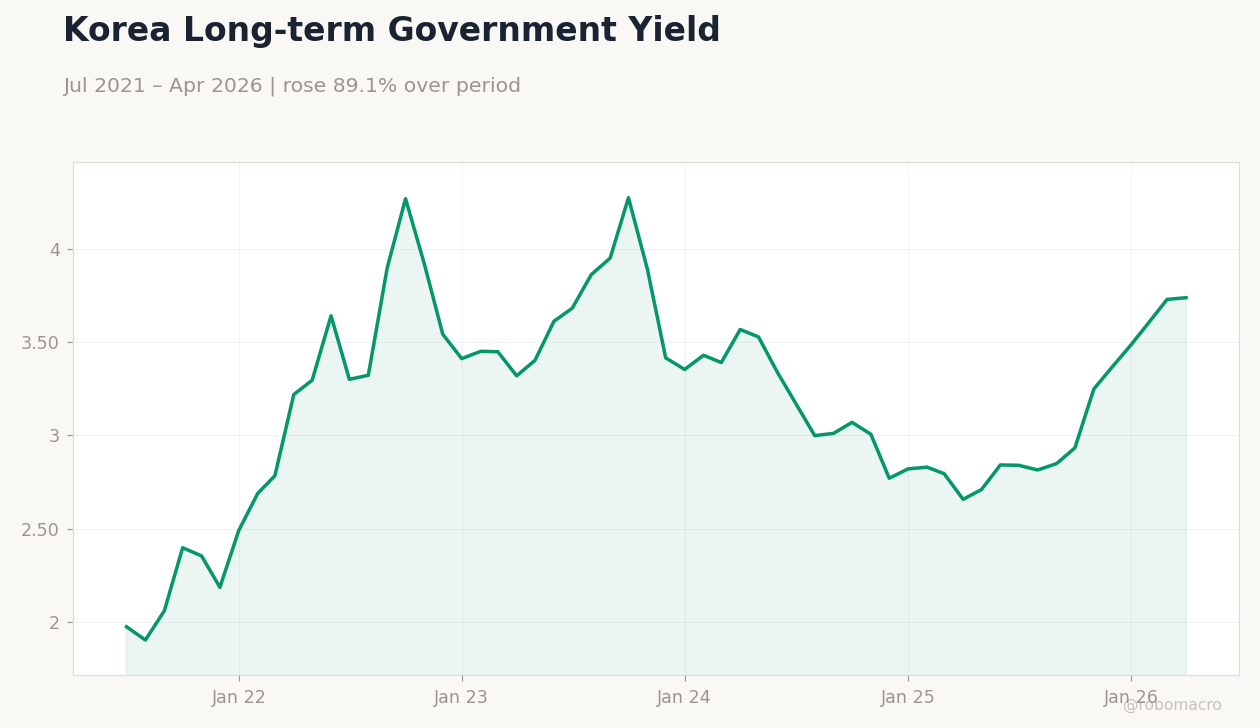

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517 | 10Y Yield %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,3.737

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517 | 10Y Yield %: 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,3.737

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

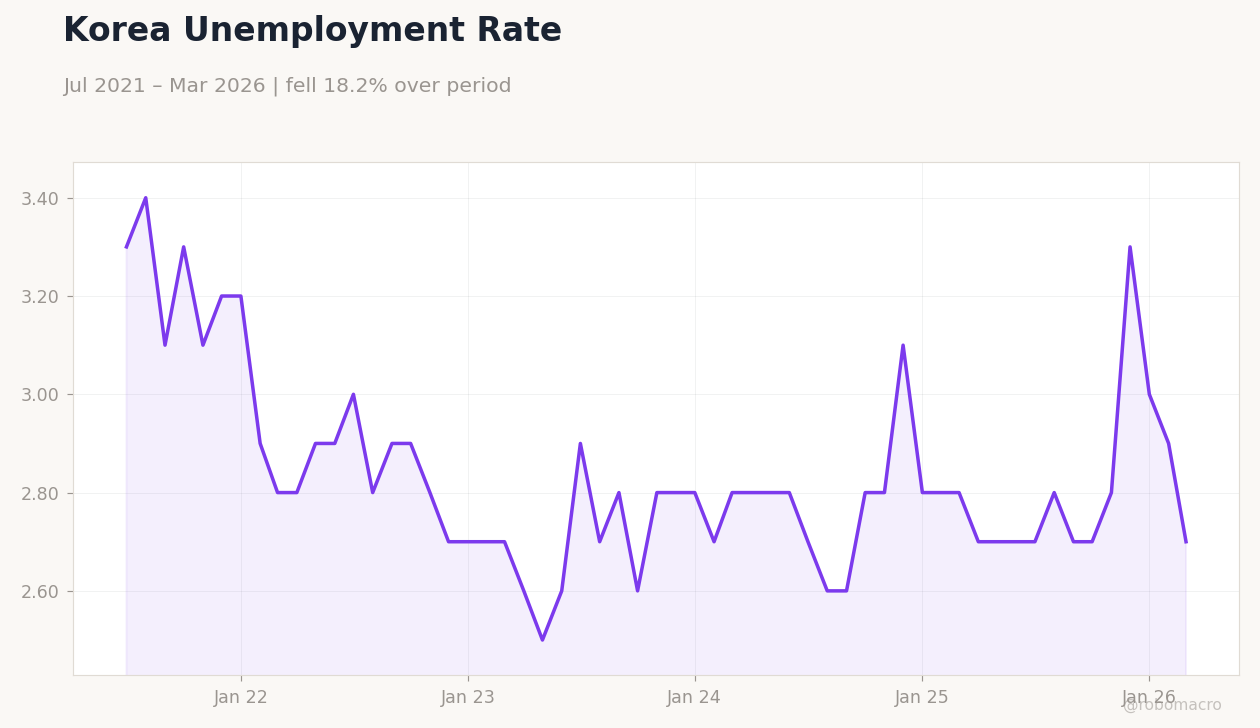

| Headline Unemployment Rate | 2.80 | - | 15:00 |

- South Korea launches first FX bank inspections in 14 years after won slide

- KOSPI jumps 8.18% to 8,096.93 while Samsung and SK Hynix fall sharply

- Unemployment rate due today with BoK base rate steady at 2.52%

Yesterday's Recap

South Korea opened inspections of major FX banks to curb destabilising won trades following persistent foreign equity outflows and expanded pension hedging. The won slipped further despite stepped-up official support, with USD/KRW closing at 1,525.81. Equities diverged sharply as KOSPI rose 8.18% to 8,096.93 while KOSDAQ gained 6.19% to 967.81.

Samsung fell 6.06% to 302,500 and SK Hynix dropped 7.54% to 2,048,000 amid leveraged-investment concerns. Korea’s short-term rate held at 2.52% while the long-term rate rose to 3.74%. Q1 GDP was revised higher to 1.8% q/q, confirming a solid start to the year.

Authorities also flagged closer monitoring of leverage risks in equity markets.

The Day Ahead

The May headline unemployment rate releases at 15:00 ET and will test labour-market resilience after recent growth upgrades. Markets await any follow-up statements from fiscal and financial regulators on FX stability measures. No BoK MPC members are scheduled to speak.

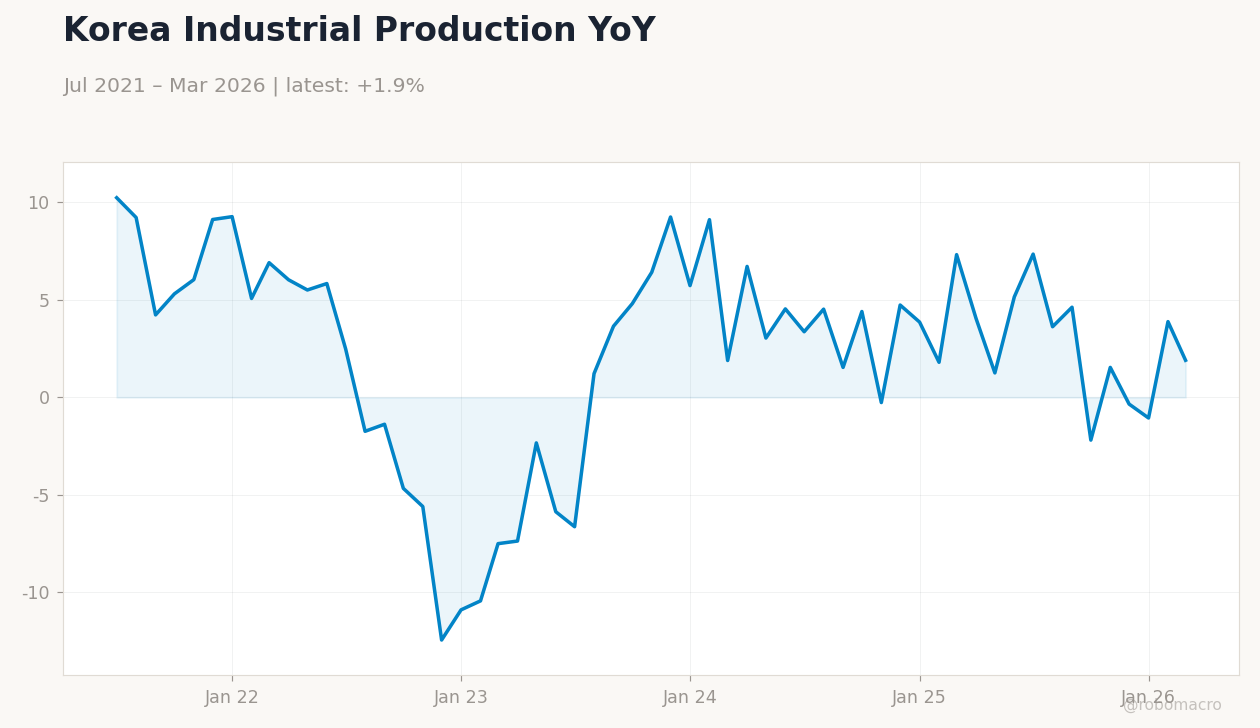

Export and import data already released this month showed resilience, supporting the view that external demand remains firm. Focus stays on won flows and potential further regulatory steps to limit speculative positions.

Other Economic Notes

Foreign capital outflows continue to pressure the won even as authorities defend the currency through direct intervention and inspections. Nvidia’s Jensen Huang secured an AI factory deal with SK, reinforcing semiconductor export momentum. Shipbuilding and US-bound exports posted solid gains last month, cushioning the external account.

Coupon programmes worth 9.1 trillion won lifted sales by 2.8 trillion won, providing a modest domestic demand boost. Leverage risks in equities have drawn coordinated attention from fiscal, monetary and financial supervisors.

Global Macro News

Brent crude rose 4.37% to 95.45, lifting Korea’s import bill and widening the terms-of-trade gap. Gold fell 4.05% to 4,087.30 as risk appetite improved globally. Bitcoin eased 0.52% to 61,322.88, offering little safe-haven support for the won.

<i>↓ p.2</i>