Korea Macro Daily(Beta Mode)

Won Weakens as FX Oversight Tightens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 7,730.82 | -4.52% |

| KOSDAQ | 951.63 | -1.67% |

| USD/KRW | 1,520.56 | -0.34% |

| Samsung | 299,000.00 | -1.16% |

| SK Hynix | 2,101,000.00 | +2.59% |

| Brent Crude | 89.09 | -4.31% |

| Gold | 4,233.80 | +3.06% |

| Bitcoin | 63,451.85 | +3.26% |

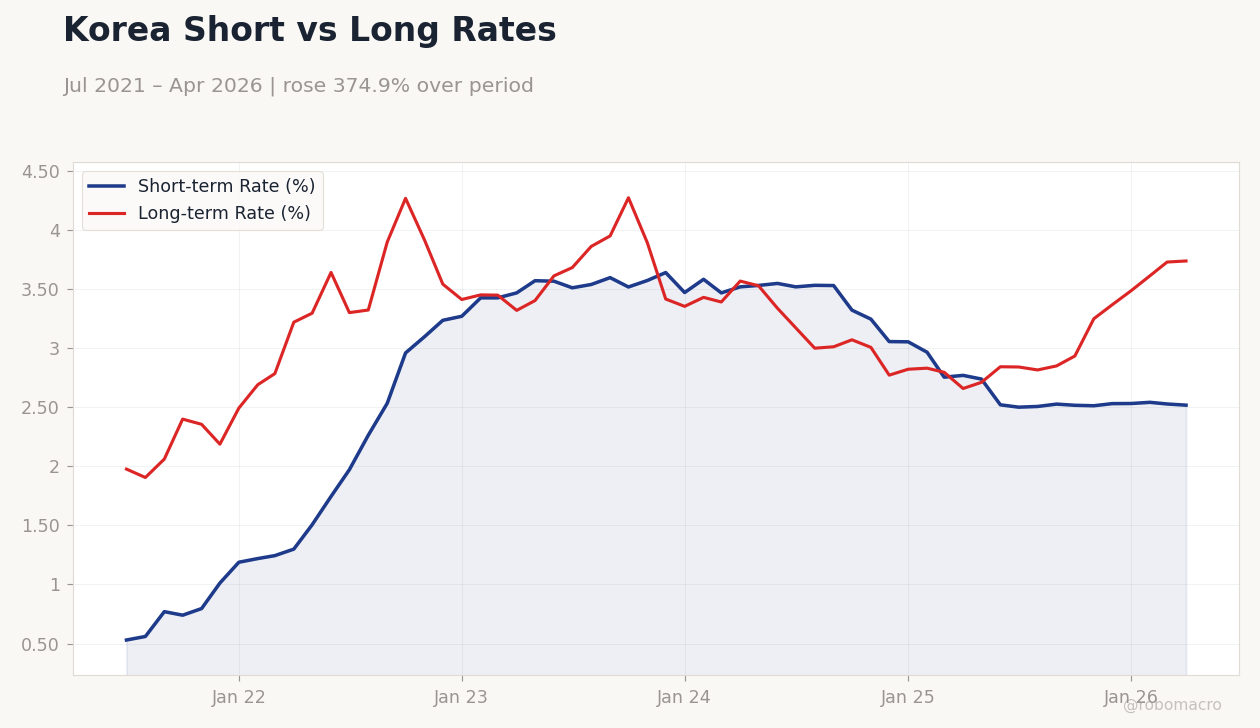

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

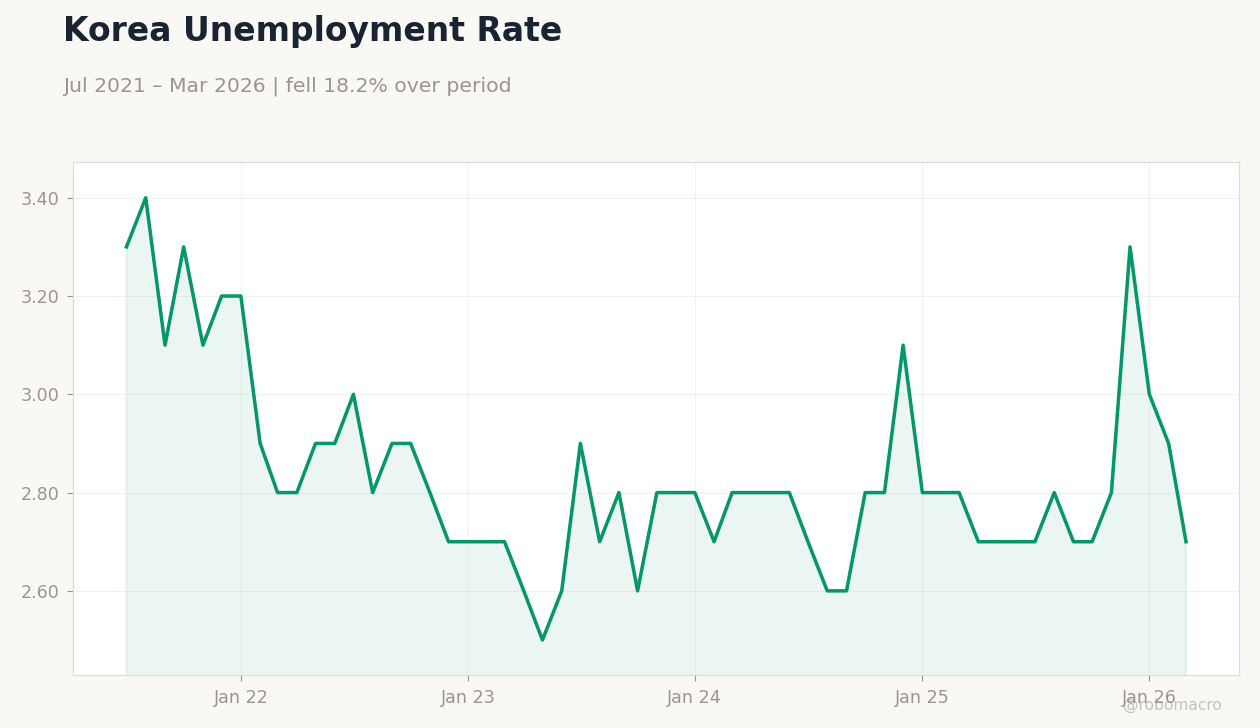

| Headline Unemployment Rate | 2.80 | - | 2.80 |

Korea Short vs Long Rates | Type: macro_line | Short-term Rate (%): 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517 | Long-term Rate (%): 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,3.737

Korea Short vs Long Rates | Type: macro_line | Short-term Rate (%): 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517 | Long-term Rate (%): 3.737 (2026-04-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,3.737

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Unemployment holds steady at 2.8% while KOSPI falls 4.52% amid won pressure.

- Authorities inspect FX banks and expand won support measures to curb volatility.

- BoK maintains 2.52% base rate and shifts focus from retail investor blame.

Yesterday's Recap

South Korea’s headline unemployment rate printed at 2.8% on June 10, matching the prior reading and showing no deterioration in labor-market conditions. Equity markets sold off sharply, with the KOSPI declining 4.52% to 7,730.82 while the KOSDAQ fell 1.67% to 951.63. The won traded at 1,520.56 per dollar, down 0.34% on the day, extending its slide toward crisis-era lows near 1,530.

Samsung shares dropped 1.16% to 299,000 won, whereas SK Hynix rose 2.59% to 2,101,000 won on continued chip-export strength. Short-term rates eased 0.40% to 2.52% while long-term yields edged up 0.24% to 3.74%. News flow highlighted the first FX-bank inspection in 14 years and stepped-up pension hedging to counter foreign equity outflows.

The Day Ahead

No major data releases are scheduled for June 11 or 12, leaving markets to digest ongoing won-support operations and regulatory scrutiny. Traders will monitor further statements from fiscal and monetary authorities on leveraged investment risks. Semiconductor export figures and any updates on provincial policy finance expansion to 164 trillion won by 2028 may influence sentiment.

Market participants also watch for signs of additional FX-bank inspections or pension-hedging adjustments.

Other Economic Notes

The government is boosting provincial policy finance to 164 trillion won by 2028 to address regional imbalances. BoK analysis flags “compound polarization” as income gaps widen across households and regions. Regulators are weighing caps on overdraft accounts at 50 million won to limit leveraged stock trading.

These measures coincide with efforts to stabilize the won without direct capital controls.

Global Macro News

Brent crude fell 4.31% to 89.09 dollars per barrel, easing imported inflation risks for Korea. Gold rose 3.06% to 4,233.80 dollars per ounce as investors sought safe-haven assets amid geopolitical tensions. Bitcoin gained 3.26% to 63,451.85 dollars, reflecting broader risk-on flows outside traditional equities.

<i>↓ p.2</i>