Korea Macro Daily(Beta Mode)

BoK Eyes Hike to Defend Weak Won

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,123.62 | +4.63% |

| KOSDAQ | 1,029.05 | +3.22% |

| USD/KRW | 1,518.55 | +0.08% |

| Samsung | 322,500.00 | +7.86% |

| SK Hynix | 2,150,000.00 | +2.33% |

| Brent Crude | 87.33 | -3.37% |

| Gold | 4,238.80 | +3.63% |

| Bitcoin | 64,665.27 | +0.38% |

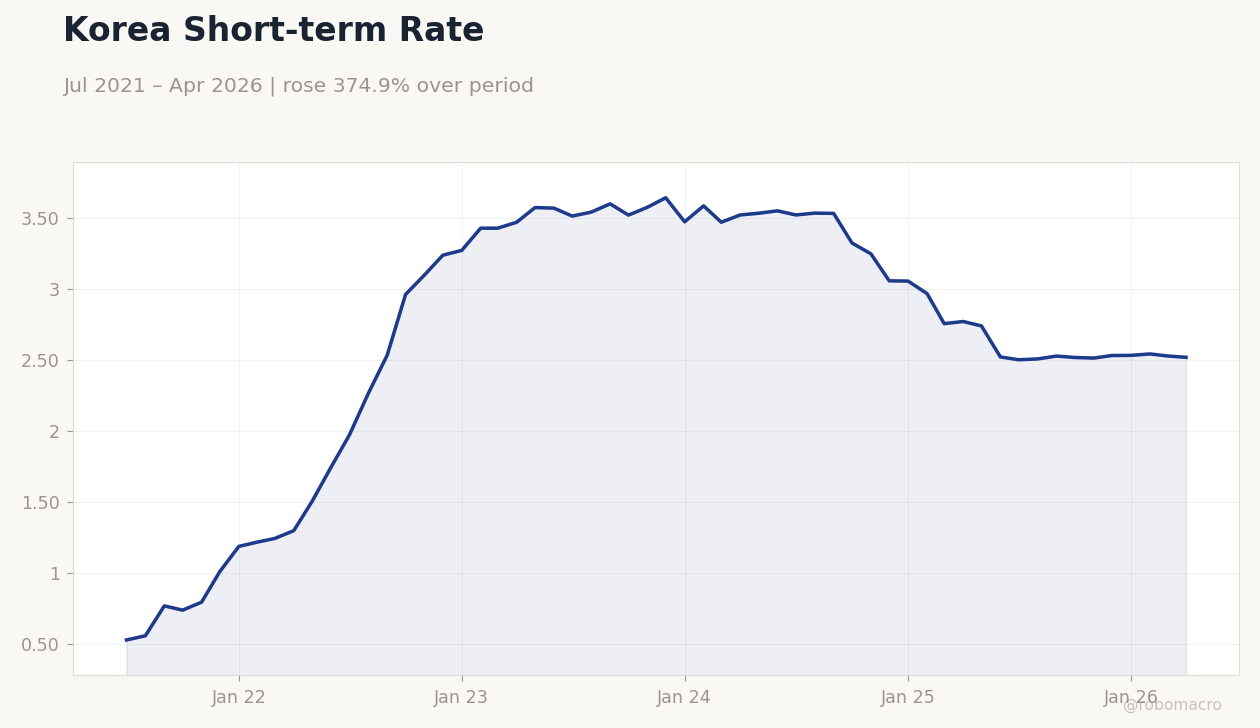

| Korea Short-term Rate | 2.52% | -0.40% |

| Korea Long-term Rate | 3.74% | +0.24% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-term Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Korea Short-term Rate | Type: macro_line | Policy Rate %: 2.517 (2026-04-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.517

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- KOSPI surged 4.63% to 8,123.62 on AI chip demand, with Samsung jumping 7.86%.

- BoK governor signals readiness for rate hikes amid elevated inflation and won pressure.

- Authorities unveil FX stabilization package as USD/KRW holds near 1,518.55.

Yesterday's Recap

Korean equities posted sharp gains as KOSPI climbed 4.63% to 8,123.62 and KOSDAQ rose 3.22% to 1,029.05, driven by semiconductor strength. Samsung Electronics advanced 7.86% to 322,500 while SK Hynix gained 2.33% to 2,150,000 on sustained HBM demand. The won edged 0.08% weaker against the dollar at 1,518.55 despite equity inflows.

Korea’s short-term rate eased 0.40% to 2.52% while the long-term rate rose 0.24% to 3.74%. Market moves reflected positioning ahead of potential BoK tightening to defend the currency. No major data releases occurred, leaving sentiment anchored to policy signals and tech flows.

The Day Ahead

Markets will monitor ongoing BoK communications for further hawkish cues on inflation and the won. FX stabilization measures announced recently are expected to remain in focus amid USD/KRW levels above 1,500. Semiconductor export trends and global chip demand will continue to influence KOSPI and KOSDAQ performance.

Investors await any updates on the 750 billion won power semiconductor investment program. Thin calendar leaves room for equity and currency volatility tied to external risk sentiment.

Other Economic Notes

Seoul committed over 500 billion won to next-generation power chip R&D to bolster long-term export competitiveness. The measures complement existing support for memory and foundry capacity amid global supply-chain shifts. Elevated USD/KRW continues to raise imported inflation risks, prompting authorities to blend FX intervention with potential monetary tightening.

Export-oriented growth remains the dominant channel linking Korea to global demand cycles.

Global Macro News

Softer US inflation prints have eased some external pressure on emerging-market currencies, yet the won remains sensitive to Fed policy divergence. Chinese demand for Korean memory chips shows tentative stabilization, supporting SK Hynix and Samsung outperformance. Brent crude fell 3.37% to 87.33, trimming energy import costs for Korea.

<i>↓ p.2</i>