Korea Macro Daily(Beta Mode)

KOSPI Hits Record as Won Slumps, BoK Hike Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,726.60 | +2.11% |

| KOSDAQ | 1,018.68 | -1.48% |

| USD/KRW | 1,527.96 | +0.97% |

| Samsung | 346,500.00 | +1.02% |

| SK Hynix | 2,521,000.00 | +5.84% |

| Brent Crude | 78.61 | -0.44% |

| Gold | 4,276.40 | -1.26% |

| Bitcoin | 64,305.17 | -1.97% |

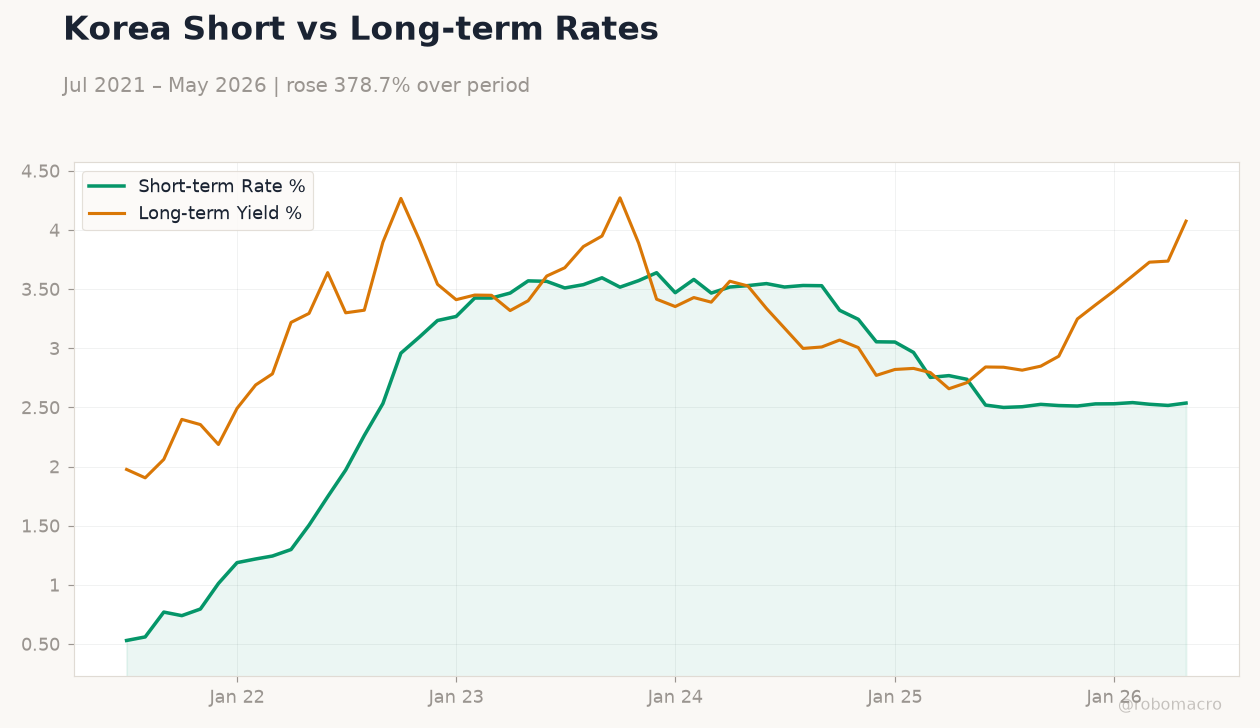

| Korea Short-term Rate | 2.54% | +0.79% |

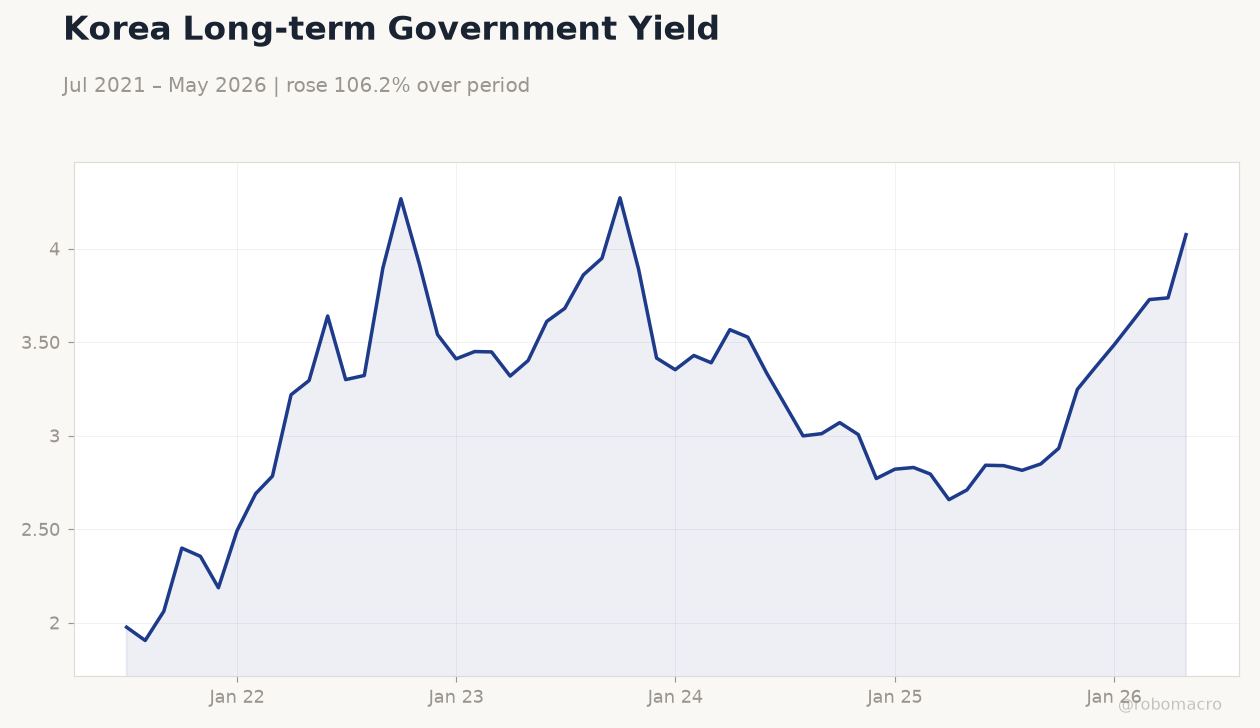

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Long-term Government Yield | Type: macro_line | 10Y Yield %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075

Korea Long-term Government Yield | Type: macro_line | 10Y Yield %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- KOSPI closes at record 8,726.60 after 2.11% surge led by SK Hynix

- BoK governor flags persistent inflation risks from tech-sector bonuses and wages

- Authorities direct banks to tighten controls as USD/KRW jumps 0.97% to 1,527.96

Yesterday's Recap

KOSPI advanced 2.11% to close at an all-time high of 8,726.60 while SK Hynix shares jumped 5.84% to 2,521,000 on sustained AI demand. KOSDAQ fell 1.48% to 1,018.68 as broader market participation narrowed. USD/KRW rose 0.97% to 1,527.96, prompting Korean authorities to urge banks to strengthen FX risk controls amid the won’s slump.

Samsung Electronics gained 1.02% to 346,500 while the Korea short-term rate edged up 0.79% to 2.54% and the long-term rate climbed 9.04% to 4.08%. Brent crude slipped 0.44% to 78.61 and gold declined 1.26% to 4,276.40. News flow highlighted BoK minutes that returned a rate-hike option to the table and warnings that large semiconductor bonuses could add to wage pressures.

No economic data releases occurred.

The Day Ahead

Markets will monitor any follow-up comments from BoK officials on inflation persistence after yesterday’s minutes. Equity flows may remain concentrated in memory-chip names given SK Hynix’s record run. Currency traders will watch for further intervention signals as USD/KRW holds above 1,520.

Bond yields are likely to stay sensitive to any shift in hike probabilities priced by futures. No major data prints are scheduled.

Other Economic Notes

Korea’s inflation outlook remains elevated as the tech boom lifts wages and bonus payments at Samsung and SK Hynix. Export strength in chips and ships continues to support the current-account surplus despite softer import growth. Savings-bank deposits have surpassed 100 trillion won, reflecting higher rate sensitivity among households.

The weak won is boosting demand for dollar-denominated insurance products while raising hedging costs for corporates.

Global Macro News

A potential US-Iran peace deal is viewed as unlikely to reduce BoK rate-hike bets given lingering Middle East uncertainty. Mizuho Bank announced support for joint Japan-South Korea energy procurement projects, which could ease LNG import costs over time. Kakao’s alliance with banks on a won-stablecoin project aims to reduce FX settlement frictions.

<i>↓ p.2</i>