Korea Macro Daily(Beta Mode)

KOSPI Sets Record on Chip Rally, Won Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,864.24 | +1.58% |

| KOSDAQ | 1,031.96 | +1.30% |

| USD/KRW | 1,538.68 | +1.83% |

| Samsung | 362,500.00 | +4.62% |

| SK Hynix | 2,685,000.00 | +6.51% |

| Brent Crude | 79.36 | -0.24% |

| Gold | 4,227.50 | -3.01% |

| Bitcoin | 63,017.53 | -3.94% |

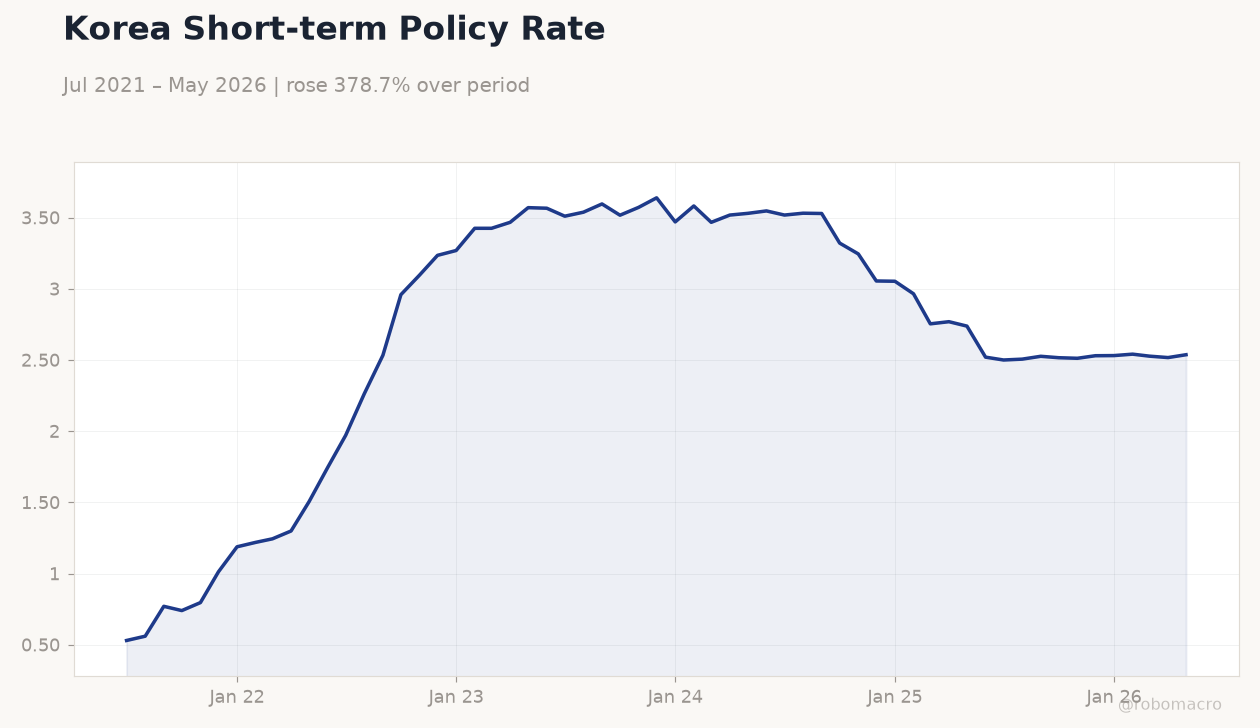

| Korea Short-term Rate | 2.54% | +0.79% |

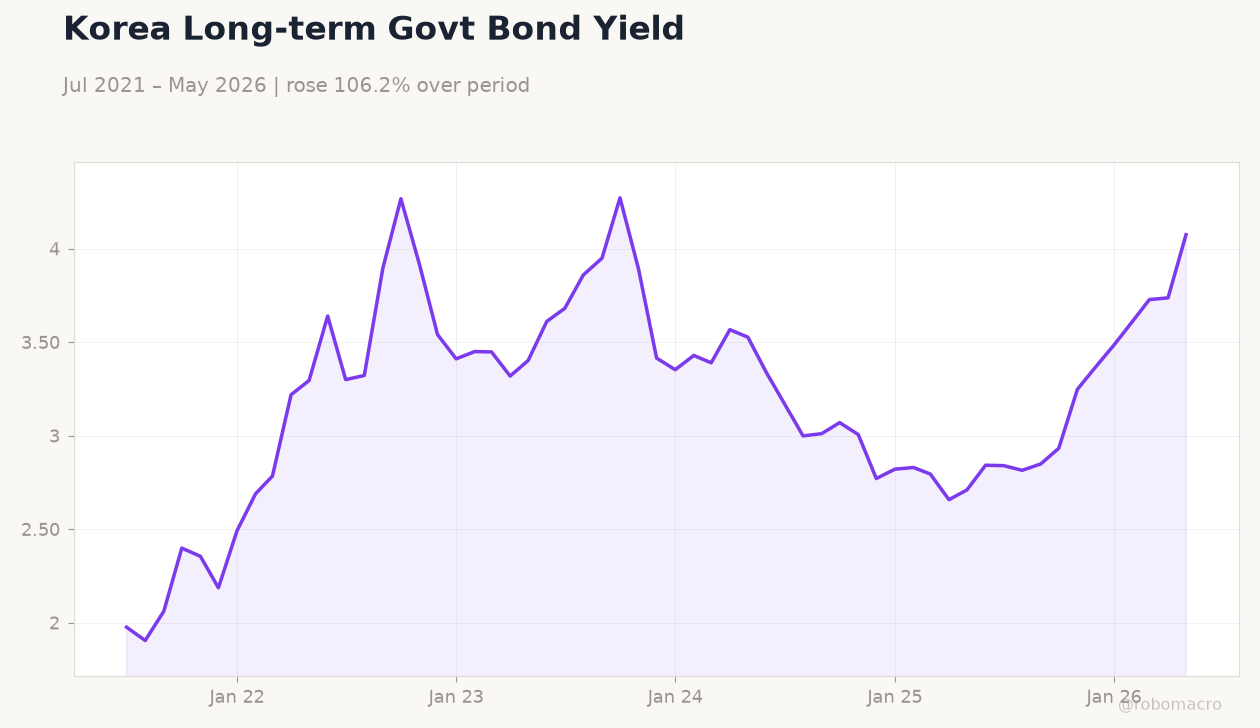

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- KOSPI rose 1.58% to 8,864.24 while KOSDAQ gained 1.30%, led by Samsung (+4.62%) and SK Hynix (+6.51%).

- USD/KRW climbed 1.83% to 1,538.68 as Korea short-term and long-term rates increased 0.79% and 9.04%.

- BoK Governor Shin maintains hike signals despite Fed pressure, with inflation seen staying elevated from tech-driven wage gains.

Yesterday's Recap

Korean equities posted sharp gains on semiconductor strength, with KOSPI closing at a record 8,864.24 and KOSDAQ at 1,031.96. Samsung Electronics and SK Hynix surged on sustained HBM demand, pushing the benchmark past prior highs despite softer breadth elsewhere. The won depreciated sharply to 1,538.68 against the dollar amid rising Treasury yields and global rate repricing.

Korea short-term rates edged up to 2.54% while long-term yields jumped to 4.08%, reflecting tighter external conditions. No domestic data releases occurred, leaving market focus on BoK communications and external policy signals. Bank loan delinquency rates reached a 10-year high in April, highlighting pockets of household stress.

Overall, the session reflected semiconductor outperformance offsetting broader macro caution.

The Day Ahead

Markets enter a data-light session with no scheduled Korean releases or BoK speakers. Attention will center on any follow-up comments from Governor Shin regarding inflation persistence and rate-hike indicators. Global equity futures and USD/KRW moves will likely dictate near-term sentiment given the absence of local catalysts.

Traders will also monitor U.S. policy signals for implications on BoK timing. Semiconductor earnings momentum remains the dominant equity driver.

Other Economic Notes

Korea’s inflation outlook stays elevated as the tech boom lifts wages, according to central bank assessments. Savings bank deposit rates have topped 4% with funds exceeding 100 trillion won, signaling competition for liquidity. Shinhan Bank closed a 240 billion won solar project financing, underscoring green investment flows.

Export resilience in chips continues to support the external sector even as domestic credit metrics show strain.

Global Macro News

The U.S. Fed’s hawkish hold has strengthened arguments for a possible BoK rate hike in July by narrowing policy divergence. Wall Street futures rallied on an apparent U.S.-Iran deal, lifting Nikkei and KOSPI to records in early trade.

<i>↓ p.2</i>