Korea Macro Daily(Beta Mode)

Tech Bonuses Fuel BoK Inflation Concerns

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 9,052.42 | -0.13% |

| KOSDAQ | 966.59 | -3.43% |

| USD/KRW | 1,533.36 | +0.13% |

| Samsung | 351,000.00 | -3.17% |

| SK Hynix | 2,703,500.00 | +0.69% |

| Brent Crude | 80.59 | +0.93% |

| Gold | 4,172.90 | -1.21% |

| Bitcoin | 64,246.41 | +1.60% |

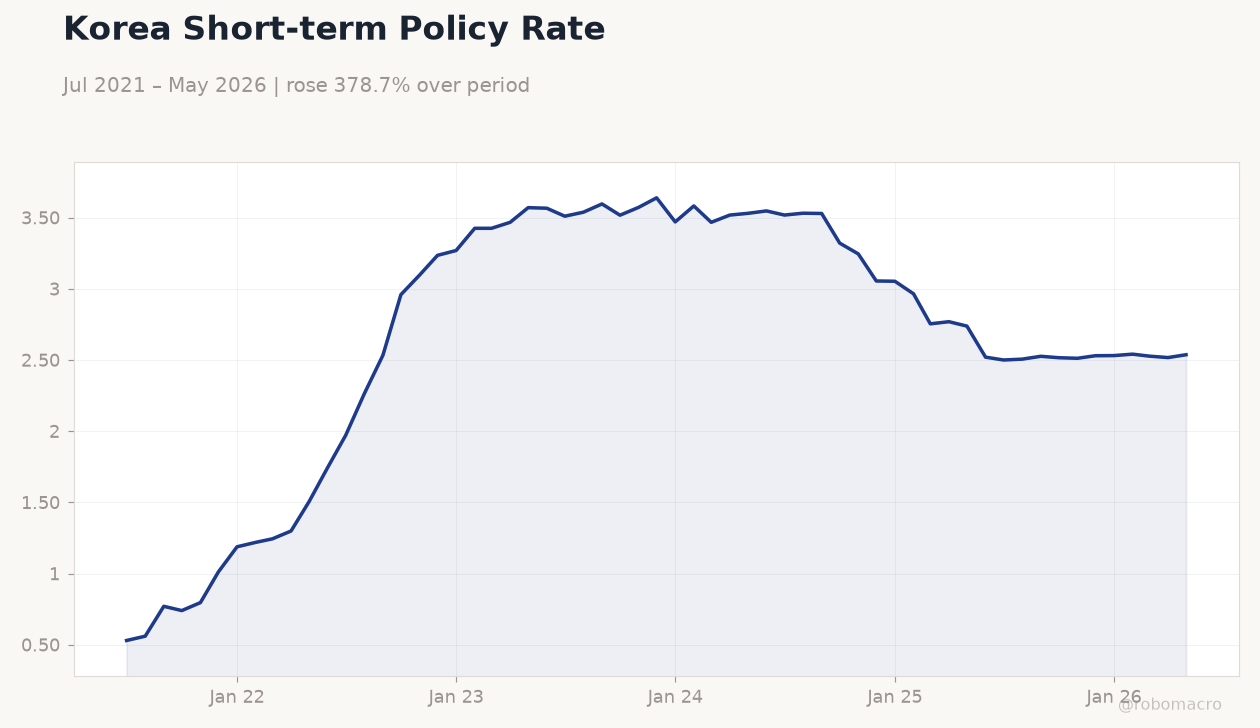

| Korea Short-term Rate | 2.54% | +0.79% |

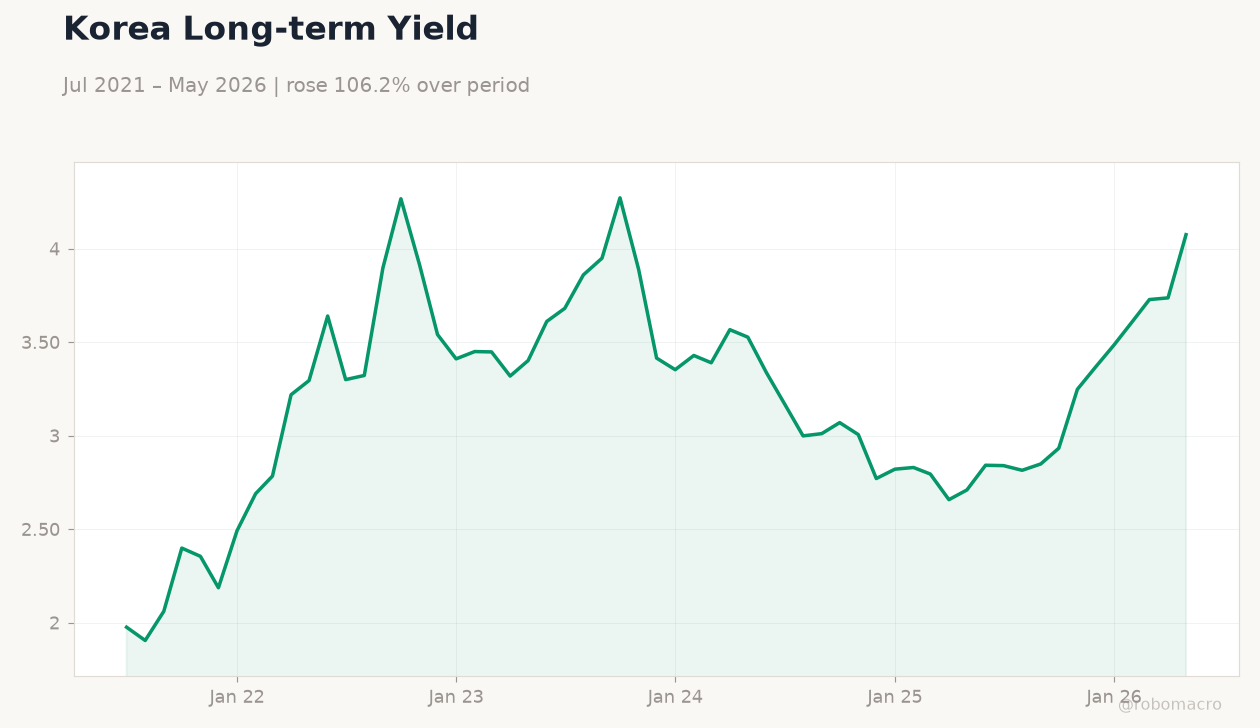

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 106.10 | - | - |

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-24) | |||

| Business Confidence Index | 80 | - | 13:00 |

- Semiconductor bonuses spark BoK warnings on wage-driven inflation risks amid AI boom.

- Won averages 1,520 per dollar in June, hitting 28-year highs and masking export weakness.

- KOSDAQ falls 3.43% as SK Hynix overtakes Samsung in market value.

Yesterday's Recap

Markets digested mixed signals from Korea’s tech sector. KOSPI slipped 0.13% to 9,052.42 while KOSDAQ dropped 3.43% to 966.59. Samsung shares fell 3.17% to 351,000 won even as SK Hynix rose 0.69% to 2,703,500 won and briefly became the nation’s most valuable listed company.

The won weakened 0.13% to 1,533.36 per dollar, extending June’s average above 1,520. Korea’s short-term rate held near 2.54% but the long-term rate jumped 9.04% to 4.08%. Consumer confidence data released yesterday showed no material change from the prior 106.1 print.

Equity losses concentrated in non-chip names while memory demand remained supportive.

The Day Ahead

Attention turns to the 24 June Business Confidence Index release at 13:00. Markets will parse any softening in the 80 reading for clues on domestic demand. No BoK speakers are scheduled before the next policy meeting.

Cross-border crypto tracking rules take effect, requiring central-bank reporting on stablecoin flows. Global chip supply updates from Taiwan could influence SK Hynix and Samsung share prices. Bond traders will watch long-term yields after yesterday’s sharp move higher.

Other Economic Notes

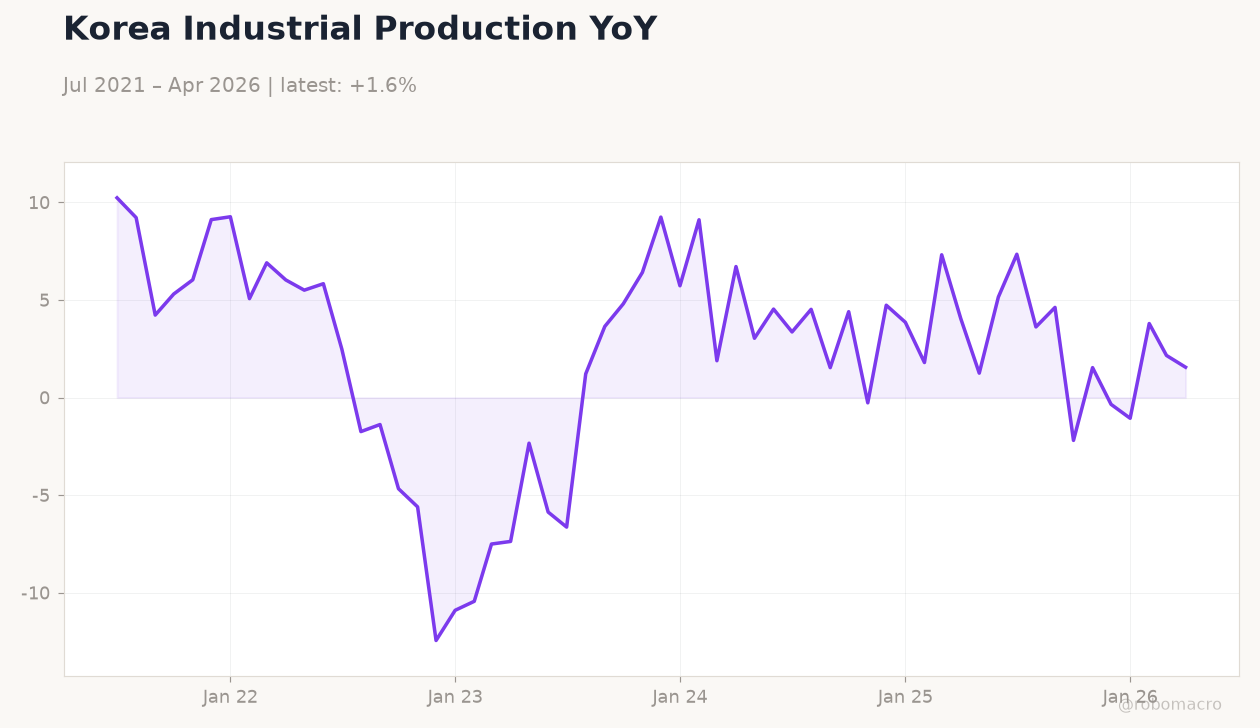

Semiconductor windfalls are offsetting broader export softness, with first-half chip shipments up sharply while non-tech goods lag. Quick-commerce volumes are projected to triple to 15 trillion won, adding to domestic price pressures. Export data for early June showed 9.2% growth, driven almost entirely by memory and shipbuilding orders.

Corporate earnings season highlights divergent performance between chipmakers and traditional manufacturers.

Global Macro News

Global AI demand continues to lift Korean memory prices and corporate bonuses, feeding domestic inflation concerns. Bitcoin rose 1.60% to 64,246 while gold fell 1.21%, reflecting shifting risk sentiment. Brent crude added 0.93% to 80.59, supporting Korea’s energy import bill.

<i>↓ p.2</i>