Korea Macro Daily(Beta Mode)

Chip Bonuses Fuel BoK Inflation Concerns

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 9,114.55 | +0.69% |

| KOSDAQ | 968.40 | +0.19% |

| USD/KRW | 1,531.51 | +0.01% |

| Samsung | 351,000.00 | -3.17% |

| SK Hynix | 2,703,500.00 | +0.69% |

| Brent Crude | 76.87 | -1.32% |

| Gold | 4,127.00 | -1.31% |

| Bitcoin | 62,497.58 | -2.27% |

| Korea Short-term Rate | 2.54% | +0.79% |

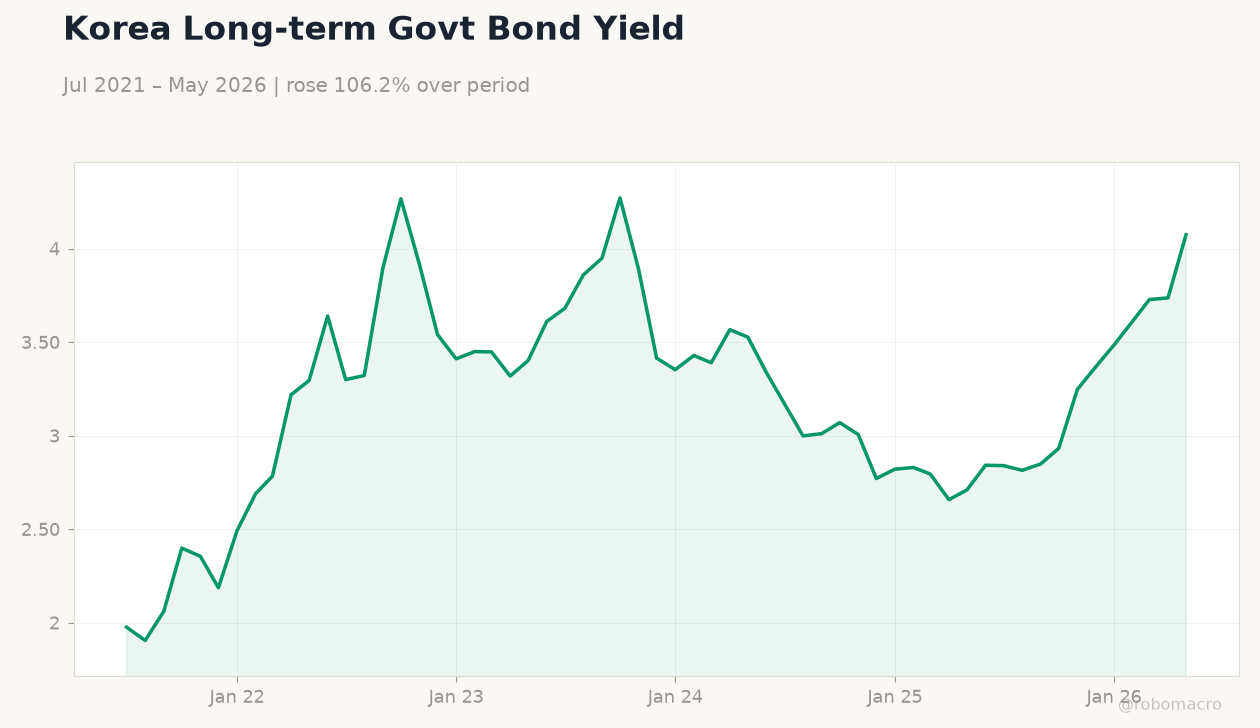

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 106.10 | - | 106.60 |

Korea Policy Rate vs CPI | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Korea Policy Rate vs CPI | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-24) | |||

| Business Confidence Index | 80 | - | 13:00 |

- Consumer confidence edged up to 106.6 in May while KRW stayed weak near 1,531.51 against USD on Fed hike bets.

- KOSPI rose 0.69% to 9,114.55 but Samsung fell 3.17% as SK Hynix overtook it in market value.

- BoK flagged wage-driven inflation risks from semiconductor bonuses amid 2.54% policy rate.

Yesterday's Recap

South Korea’s Consumer Confidence Index rose to 106.6 from 106.1 on 22 June, showing modest household resilience. Equity markets closed mixed with KOSPI advancing 0.69% to 9,114.55 on selective semiconductor buying while KOSDAQ gained 0.19% to 968.40. Samsung Electronics dropped 3.17% to 351,000 won as foreign selling intensified, allowing SK Hynix to surpass it as the nation’s most valuable listed firm with a 0.69% gain.

USD/KRW held steady at 1,531.51, reflecting persistent depreciation pressures tied to expectations of higher US rates. Korea’s short-term rate stood at 2.54% and the long-term rate reached 4.08%, signaling tighter financial conditions. Corporate profit growth accelerated in Q1 per BoK data, yet export momentum remained concentrated in chips and autos.

The Day Ahead

Markets await the 24 June Business Confidence Index release at 13:00, which last printed at 80 and may highlight manufacturing caution. No major data prints are scheduled for 23 June itself. Traders will monitor any follow-up comments from BoK officials on wage pressures in the semiconductor sector.

Global risk sentiment and USD direction will continue to drive KRW flows ahead of the FOMC. Bond yields may stay elevated given the recent steepening in the Korea curve.

Other Economic Notes

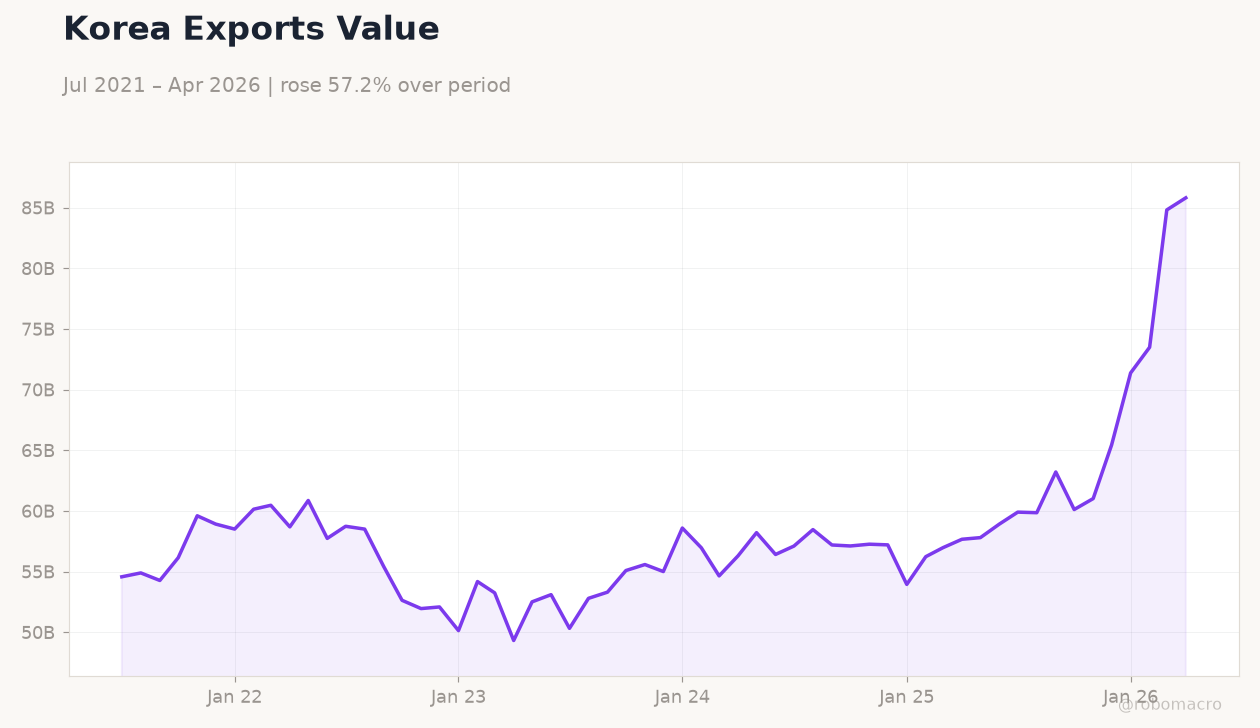

Semiconductor windfalls have lifted Q1 corporate sales and profits, yet the resulting bonus surge now poses a direct inflation challenge for policymakers. Export data through mid-June showed 9% annual growth led by memory chips, supporting the external sector despite soft industrial production prints. Indonesia-South Korea cooperation deals worth $102 billion span shipbuilding, autos and energy, broadening trade channels.

Unpaid domestic labor reached an annual economic value above 582 trillion won, underscoring structural labor-market gaps.

Global Macro News

The Federal Reserve’s hawkish tilt kept upward pressure on USD/KRW and capped won appreciation despite occasional verbal intervention by Korean officials. <i>↓ p.2</i>