Korea Macro Daily(Beta Mode)

BoK Flags Higher Rates Amid Housing, Debt Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,203.84 | -9.99% |

| KOSDAQ | 891.52 | -7.94% |

| USD/KRW | 1,542.20 | +0.20% |

| Samsung | 351,000.00 | -3.17% |

| SK Hynix | 2,703,500.00 | +0.69% |

| Brent Crude | 73.13 | -5.12% |

| Gold | 4,015.70 | -2.77% |

| Bitcoin | 60,640.27 | -3.24% |

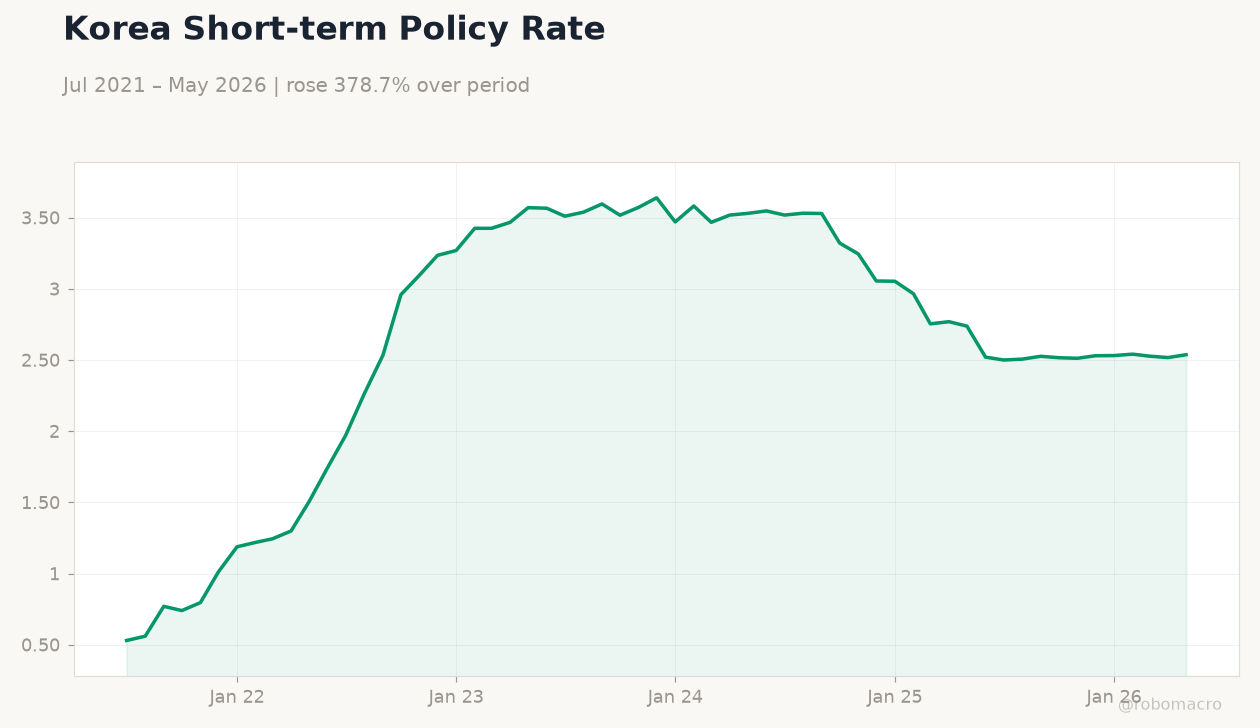

| Korea Short-term Rate | 2.54% | +0.79% |

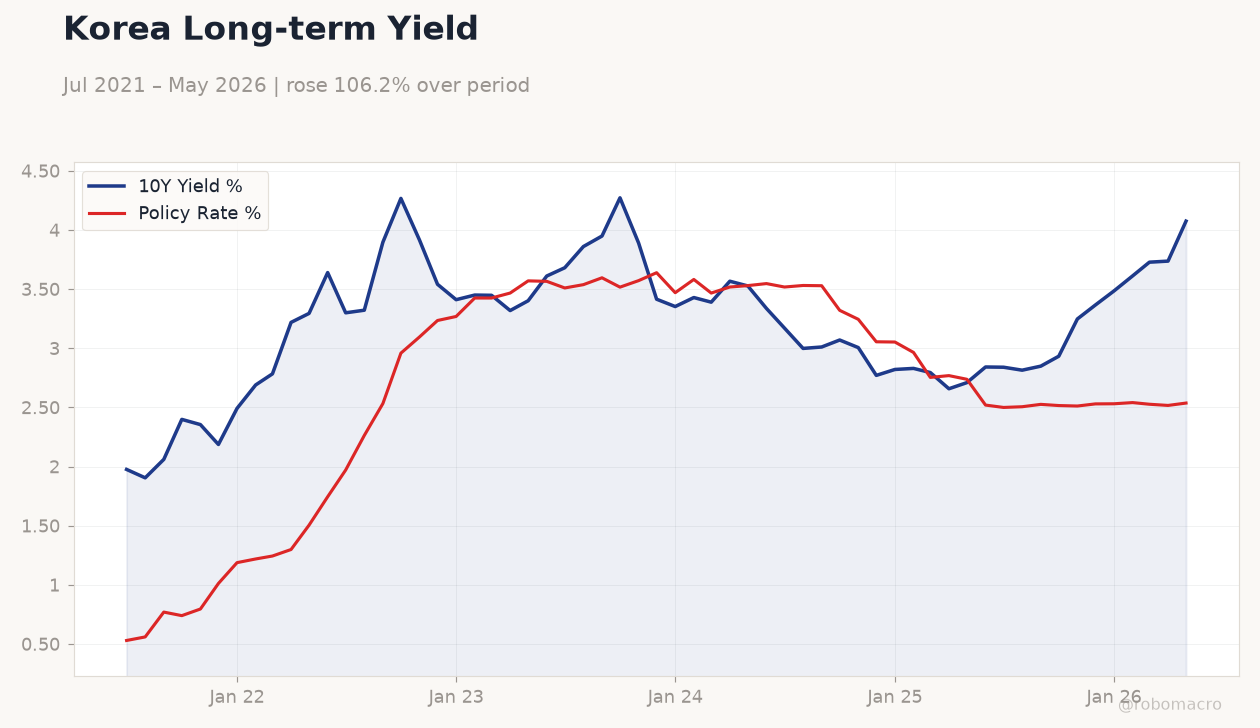

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 106.10 | - | 106.60 |

| Business Confidence Index | 80 | - | - |

Korea Long-term Yield | Type: macro_line | 10Y Yield %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075 | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Korea Long-term Yield | Type: macro_line | 10Y Yield %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075 | Policy Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Consumer confidence edged up to 106.6 in May while BoK reiterated need for tighter policy amid rising household debt and housing pressures.

- KOSPI plunged 9.99% to 8,203.84 and KOSDAQ fell 7.94% to 891.52 as hawkish BoK signals and Fed hike expectations weighed on sentiment.

- USD/KRW rose 0.20% to 1,542.20 with the short-term rate at 2.54% and long-term yields jumping 9.04% to 4.08%.

Yesterday's Recap

South Korea’s Consumer Confidence Index improved to 106.6 from 106.1, reflecting modest resilience in household sentiment. Equity markets sold off sharply, with KOSPI dropping nearly 10% and KOSDAQ declining almost 8% amid valuation concerns and rate sensitivity. The won weakened further against the dollar as markets priced greater odds of BoK holding or hiking.

Samsung shares fell 3.17% while SK Hynix gained 0.69%, highlighting divergent semiconductor performance. Short-term rates held at 2.54% but long-term yields surged, signaling tighter financial conditions ahead. News flow centered on BoK warnings that higher rates remain necessary to address housing imbalances and debt vulnerabilities.

No major data surprises altered the hawkish tilt priced into markets.

The Day Ahead

Markets enter a data-light session with no scheduled Korean releases or BoK speeches. Focus will remain on won movements and any follow-through from yesterday’s BoK comments on debt risks. Global cues from U.S.

yields and Fed rhetoric will drive USD/KRW and KTB trading. Equity investors will monitor Samsung buyback developments for potential support after the sharp selloff. Semiconductor supply-chain updates could influence SK Hynix and broader tech sentiment.

Other Economic Notes

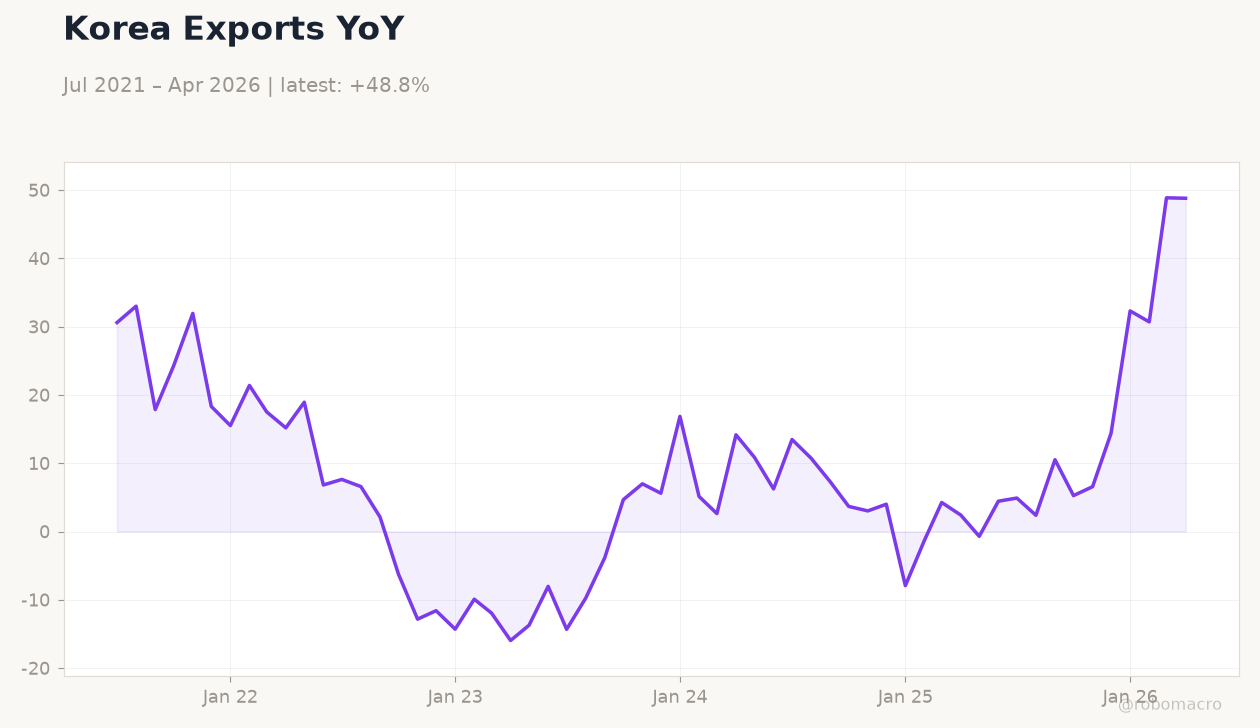

BoK communications stress that policy must stay vigilant against housing market excesses and elevated household leverage. Export-oriented growth continues to hinge on semiconductor demand, which remains the dominant driver of trade surpluses. Rising long-term yields reflect markets adjusting to a less dovish BoK path than previously anticipated.

Self-employed borrowers face growing arrears risks if rates stay elevated, a key stability concern highlighted by the central bank.

Global Macro News

Hawkish BoK expectations intensified after officials flagged the need for higher rates to curb housing and debt risks. The won slipped to over two-week lows as markets also priced greater odds of Fed tightening. <i>↓ p.2</i>