Korea Macro Daily(Beta Mode)

BoK Flags Need for Higher Rates on Debt Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,471.02 | +3.26% |

| KOSDAQ | 909.31 | +2.00% |

| USD/KRW | 1,544.64 | +0.61% |

| Samsung | 340,500.00 | +9.84% |

| SK Hynix | 2,580,000.00 | +0.98% |

| Brent Crude | 75.00 | +1.71% |

| Gold | 4,041.60 | +1.29% |

| Bitcoin | 60,101.00 | -1.47% |

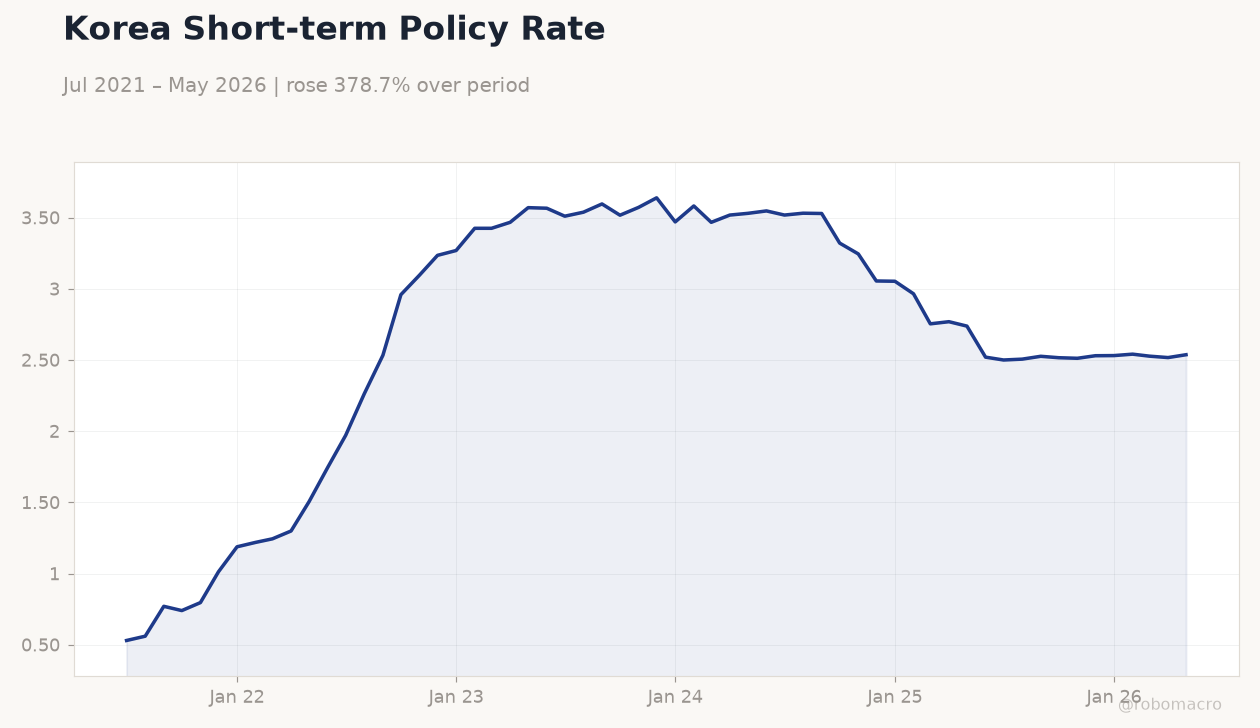

| Korea Short-term Rate | 2.54% | +0.79% |

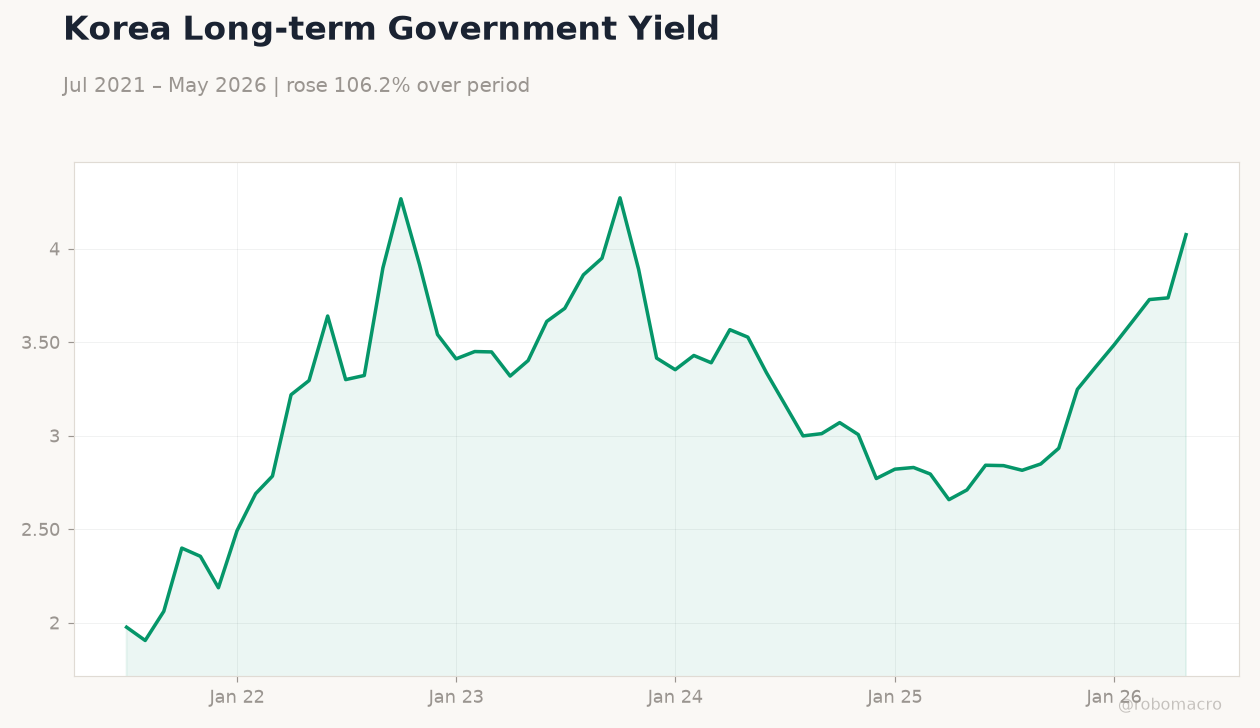

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 106.10 | - | 106.60 |

| Business Confidence Index | 80 | - | 79 |

Korea Short-term Policy Rate | Type: macro_line | Percent: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Korea Short-term Policy Rate | Type: macro_line | Percent: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- KOSPI surged 3.26% to 8,471.02 as Samsung jumped 9.84%, while USD/KRW rose 0.61% to 1,544.64.

- Consumer confidence edged up to 106.6 but business confidence fell to 79 on June 24.

- BoK reiterated need for higher rates to address housing and household debt risks.

Yesterday's Recap

South Korea released June consumer confidence at 106.6, up from 106.1, while business confidence slipped to 79 from 80. Equity markets posted strong gains with KOSPI advancing 3.26% to 8,471.02 and KOSDAQ rising 2.00% to 909.31, led by Samsung Electronics climbing 9.84% to 340,500. The won weakened as USD/KRW climbed 0.61% to 1,544.64.

Short-term rates rose 0.79% to 2.54% and long-term rates jumped 9.04% to 4.08%. SK Hynix gained 0.98% amid ongoing semiconductor demand. Brent crude and gold both advanced, supporting broader risk sentiment.

Treasury issuance details showed July supply lifted to 16 trillion won, bringing first-half totals to 124 trillion won. Household debt-to-GDP remains above major-economy averages, keeping stability concerns elevated.

The Day Ahead

No major data releases are scheduled for June 25. Markets will monitor follow-through buying in semiconductors after yesterday’s rally. Treasury supply increases to 16 trillion won in July may pressure longer yields.

Investors await any further BoK commentary on financial stability. Equity flows could remain supported by JPMorgan’s raised KOSPI target of 12,500. Attention stays on won volatility near two-week lows.

AI chip expansion effects on the property market and record US-held financial assets reported for 2025 will also feature in sentiment.

Other Economic Notes

Korea’s household debt-to-GDP ratio exceeds the major economy average, keeping financial stability in focus. Financial assets held in the US reached a fresh record high in 2025 per BoK data. July treasury issuance was lifted to 16 trillion won, bringing first-half supply to 124 trillion won.

AI chip expansion continues to spill into the domestic property market. Export-oriented sectors remain the primary growth driver amid steady global chip demand. Manufacturing sentiment surveys pointed to a July dip, raising caution on won and KOSPI momentum.