Korea Macro Daily(Beta Mode)

KOSPI Plunges 5.8%, Won Tests 1,550 Line

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,411.21 | -5.81% |

| KOSDAQ | 851.37 | -4.10% |

| USD/KRW | 1,535.04 | -0.74% |

| Samsung | 339,500.00 | -5.30% |

| SK Hynix | 2,673,000.00 | -8.36% |

| Brent Crude | 72.60 | -3.53% |

| Gold | 4,096.30 | +1.63% |

| Bitcoin | 59,608.34 | -0.55% |

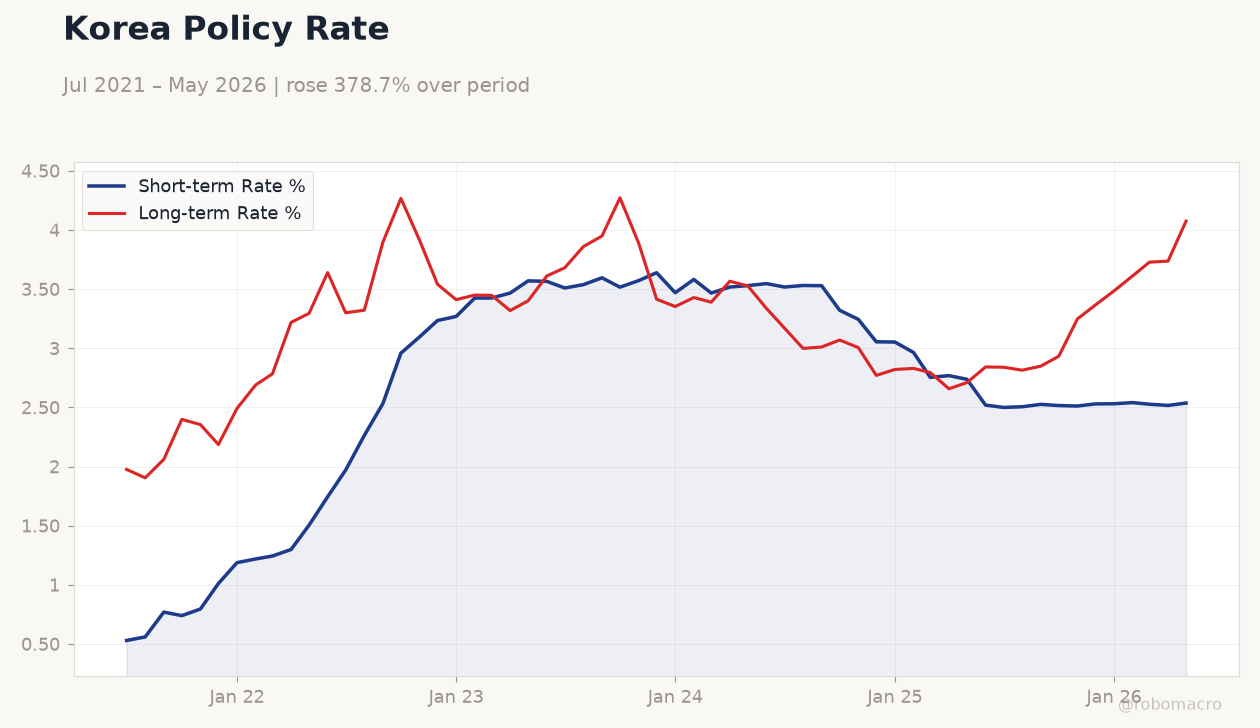

| Korea Short-term Rate | 2.54% | +0.79% |

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 106.10 | - | 106.60 |

| Business Confidence Index | 80 | - | 79 |

Korea Policy Rate | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537 | Long-term Rate %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075

Korea Policy Rate | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.53–3.639 | Trend(6pt): 0.53,2.533,3.572,3.053,2.527,2.537 | Long-term Rate %: 4.075 (2026-05-01) | Range: 1.905–4.272 | Trend(6pt): 1.976,3.897,3.89,2.821,3.728,4.075

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- KOSPI triggers circuit breaker on 5.81% drop to 8,411.21 as chip profit-taking intensifies.

- USD/KRW rebounds from 1,550 after suspected intervention; exports and inflation support BoK hike path.

- Consumer confidence rises to 106.6 while business confidence slips to 79; fuel price cap cut 150 won/liter.

Yesterday's Recap

South Korea’s equity markets suffered a sharp reversal on 27 June. KOSPI fell 5.81% to 8,411.21, activating the circuit breaker, while KOSDAQ declined 4.10% to 851.37. Samsung Electronics dropped 5.30% and SK Hynix plunged 8.36%, reflecting heavy profit-taking in AI-related chips.

USD/KRW eased 0.74% to 1,535.04 after authorities appeared to defend the 1,550 level. Consumer confidence improved to 106.6 from 106.1, but business confidence weakened to 79 from 80. Korea also lowered the fuel price cap by 150 won per liter as Brent crude retreated 3.53% to 72.60.

The Korea short-term rate stood at 2.54% and the long-term rate at 4.08%.

The Day Ahead

No major data releases are scheduled for 28 June. Markets will monitor any follow-through intervention signals near 1,550 on USD/KRW. Equity flows may remain sensitive to global semiconductor news after yesterday’s selloff.

The new 24-hour won trading regime begins to draw dealer attention for liquidity and risk-management implications. Tariff-rate quota expansions on food imports should continue to ease near-term CPI pressures. Participants await the next BoK speakers for any shift in forward guidance.

Other Economic Notes

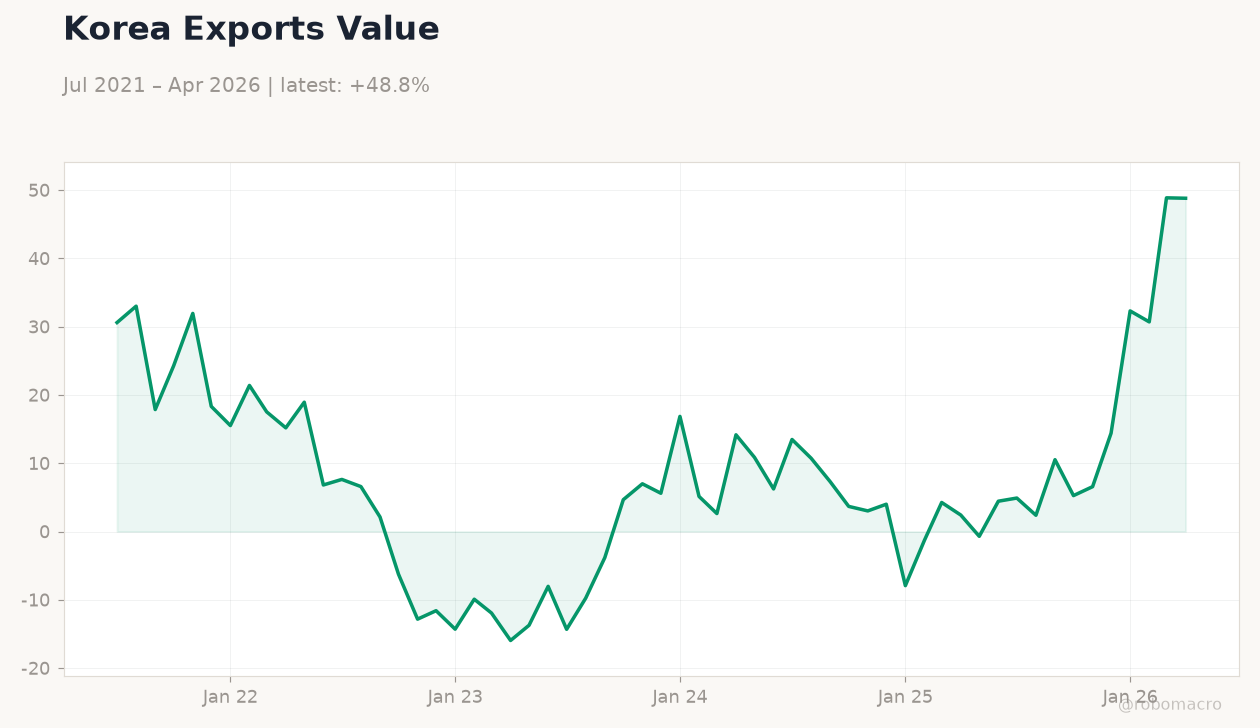

Strong May exports and firming inflation have kept alive market expectations for additional BoK rate hikes. The ETF market has surpassed 500 trillion won, overtaking KOSDAQ turnover and signaling deeper retail participation. SK Hynix’s planned Nasdaq ADR listing is viewed as a potential structural support for the won over time.

Expanded food import quotas and the fuel-cap reduction both target cost-of-living relief without altering the underlying export-driven growth narrative.

Global Macro News

Global chip demand concerns intensified after the KOSPI-led selloff, raising short-term risk alarms for AI supply chains. <i>↓ p.2</i>