Korea Macro Daily(Beta Mode)

Exports Jump as Won Weakens Further

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,476.48 | +0.97% |

| KOSDAQ | 916.18 | -0.48% |

| USD/KRW | 1,553.32 | +0.75% |

| Samsung | 320,500.00 | -4.04% |

| SK Hynix | 2,615,000.00 | -1.32% |

| Brent Crude | 71.14 | -2.44% |

| Gold | 4,044.60 | +0.54% |

| Bitcoin | 60,750.03 | +3.74% |

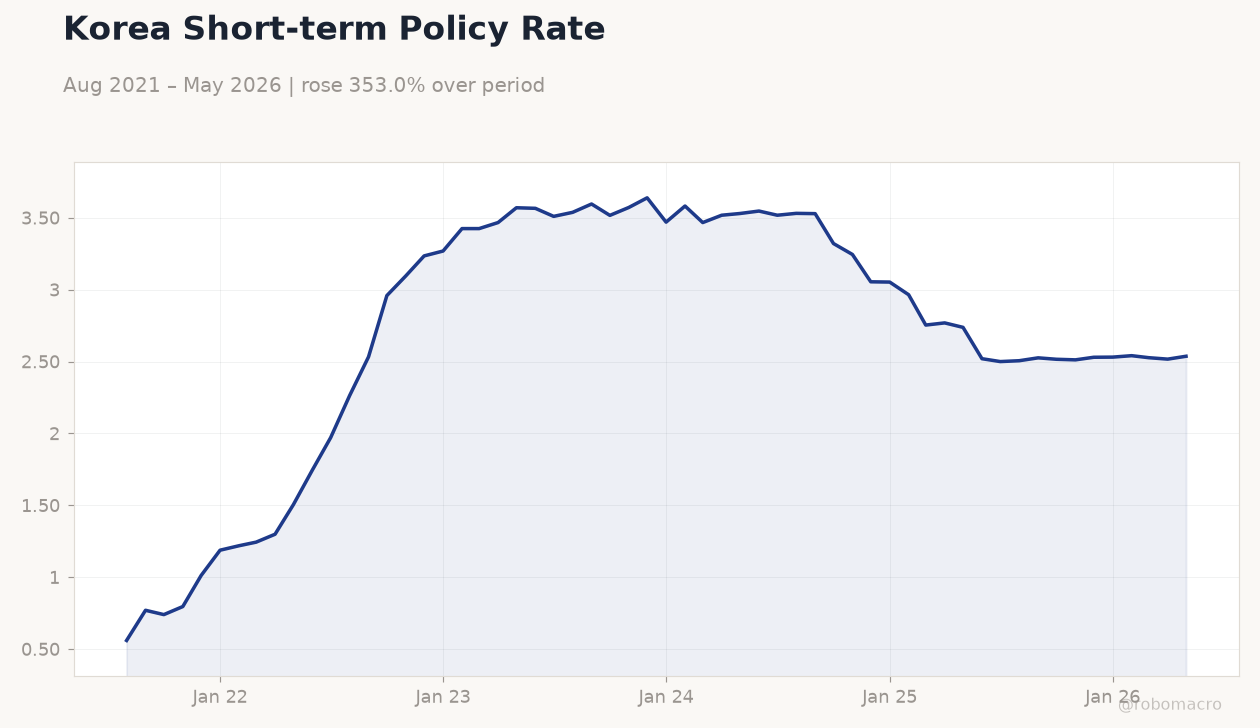

| Korea Short-term Rate | 2.54% | +0.79% |

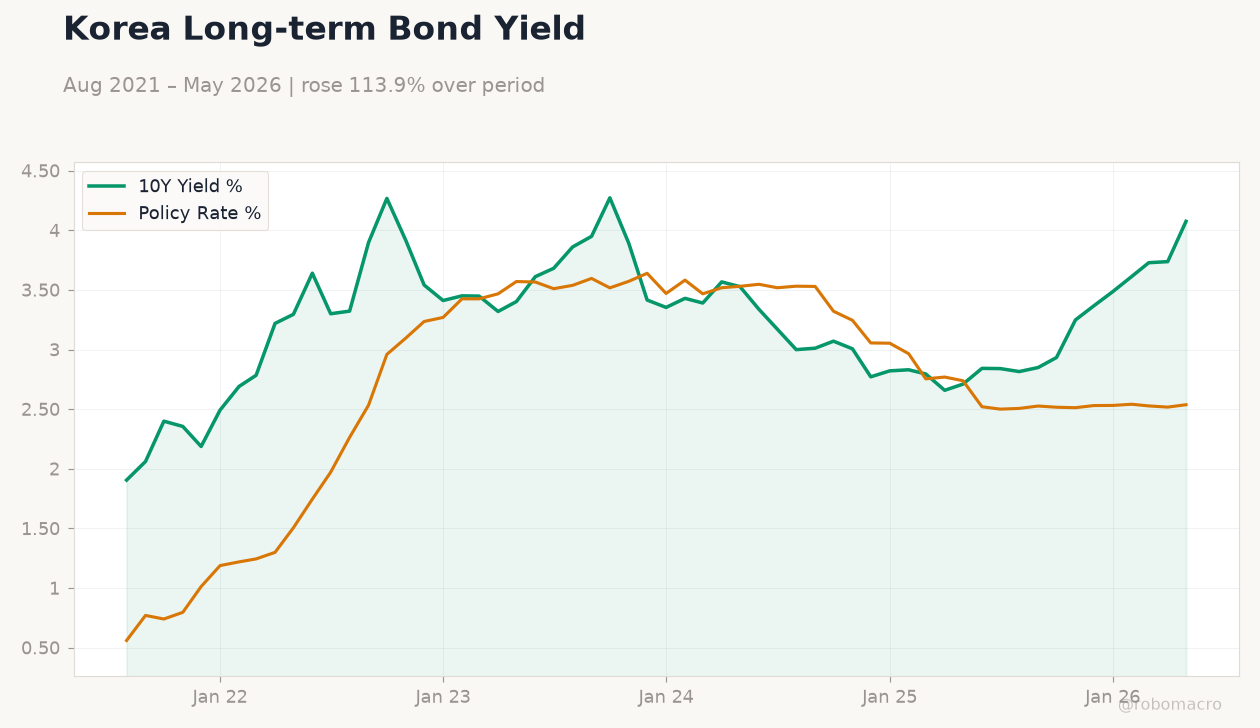

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

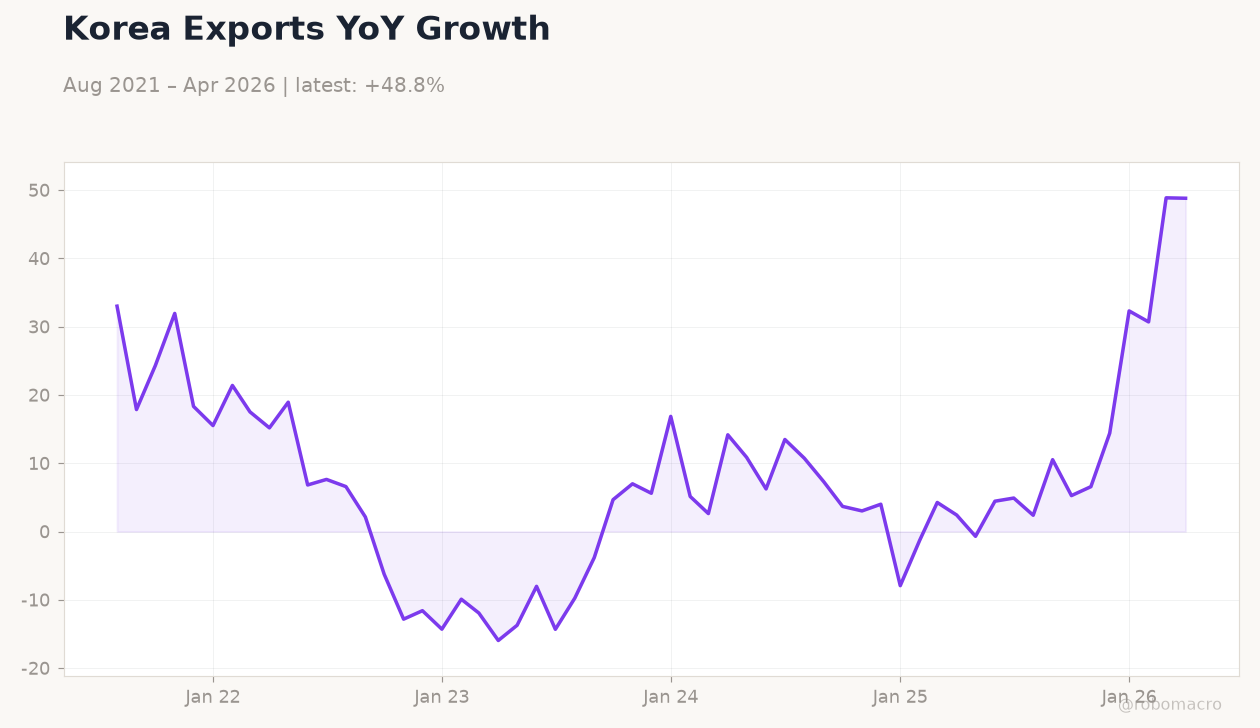

| Exports Year-over-Year | 53.40 | - | 70.90 |

| S&P Global Manufacturing PMI Index | 54.80 | - | 52.10 |

| BoK Gov Shin Speech | - | - | - |

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.56–3.639 | Trend(6pt): 0.56,2.959,3.639,2.965,2.517,2.537

Korea Short-term Policy Rate | Type: macro_line | Policy Rate %: 2.537 (2026-05-01) | Range: 0.56–3.639 | Trend(6pt): 0.56,2.959,3.639,2.965,2.517,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 3.10 | 3.20 | 19:00 |

- South Korea exports jumped to 70.9% y/y while manufacturing PMI fell to 52.1 in June.

- KOSPI rose 0.97% to 8,476.48 but USD/KRW climbed 0.75% to 1,553.32 on foreign outflows.

- BoK base rate held at 2.54% as markets await July inflation data due today.

Yesterday's Recap

South Korea posted a sharp exports acceleration to 70.9% y/y on June 30, up from 53.4% prior, driven by sustained AI chip demand. The S&P Global Manufacturing PMI slipped to 52.1 from 54.8, signaling some moderation in factory momentum. Governor Shin delivered remarks that reinforced steady policy stance without new forward guidance.

KOSPI advanced 0.97% while KOSDAQ slipped 0.48%, with Samsung falling 4.04% despite sector tailwinds. The won weakened further as USD/KRW rose to 1,553.32 amid ongoing foreign equity sales. Short-term rates edged up 0.79% to 2.54% while long-term yields surged 9.04% to 4.08%.

Brent crude declined 2.44% to $71.14, offering limited relief to import costs.

The Day Ahead

June inflation is scheduled for release at 19:00 ET with consensus at 3.2% y/y versus 3.1% prior. Markets will parse any deviation for clues on BoK timing. No additional domestic data prints are listed for the session.

Global yen moves and U.S. tech performance will likely drive USD/KRW and KOSPI flows. Traders also monitor 24-hour won trading preparations ahead of next week’s launch.

Other Economic Notes

Authorities sold $13.6 billion in reserves to cap won depreciation amid the dollar surge. Yen weakness near 40-year lows is shifting Korean spending patterns toward domestic consumption and away from pure export reliance. Banks are expanding London and Seoul desks to support round-the-clock won trading starting next week.

Strategic funds such as BNK Group’s 50 billion won vehicle target AI and semiconductor supply chains.

Global Macro News

Japan’s yen hit multi-decade lows, intensifying competitive pressure on Korean exporters and widening interest-rate differentials. Foreign investors continued net selling of Korean equities, pushing the won to its weakest levels since the global financial crisis. South Korea’s record semiconductor exports provided a partial offset but failed to stabilize the currency.

<i>↓ p.2</i>