Korea Macro Daily(Beta Mode)

Inflation Hits 30-Month High as Exports Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| KOSPI | 8,303.41 | -2.04% |

| KOSDAQ | 929.35 | +1.44% |

| USD/KRW | 1,539.25 | -0.60% |

| Samsung | 291,500.00 | -7.31% |

| SK Hynix | 2,333,000.00 | -8.87% |

| Brent Crude | 71.54 | -0.04% |

| Gold | 4,135.50 | +1.65% |

| Bitcoin | 61,471.20 | +2.45% |

| Korea Short-term Rate | 2.54% | +0.79% |

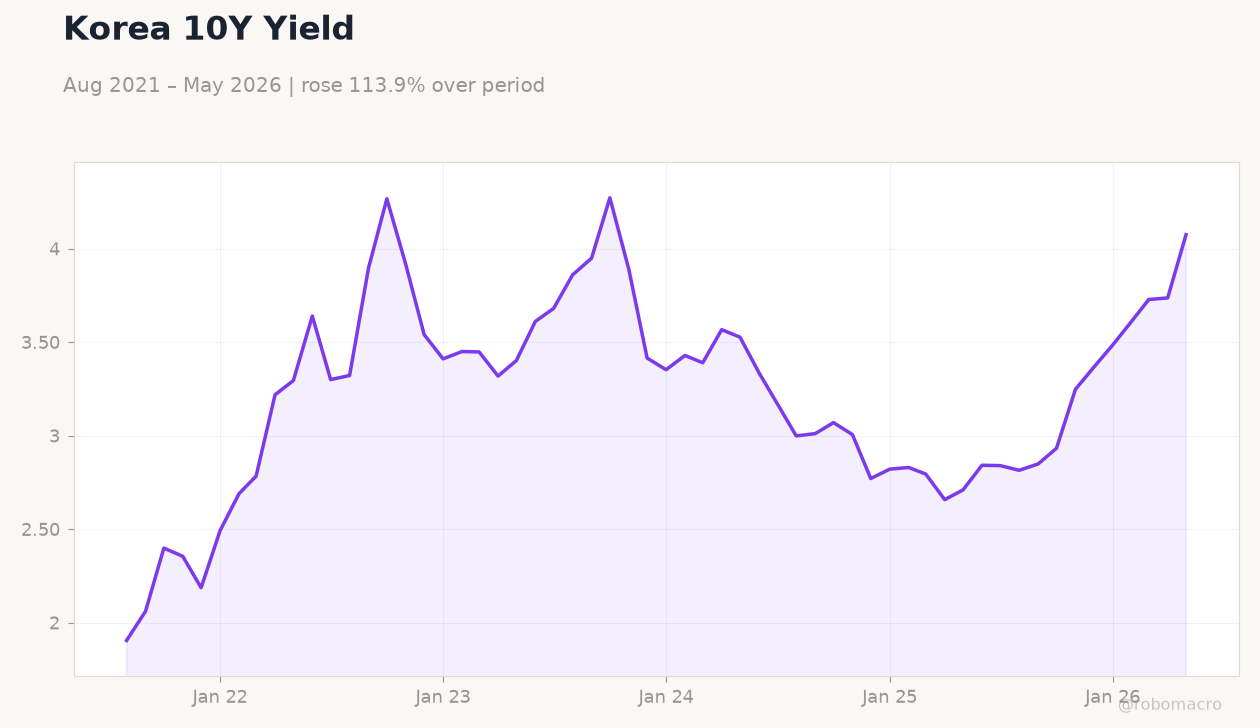

| Korea Long-term Rate | 4.08% | +9.04% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

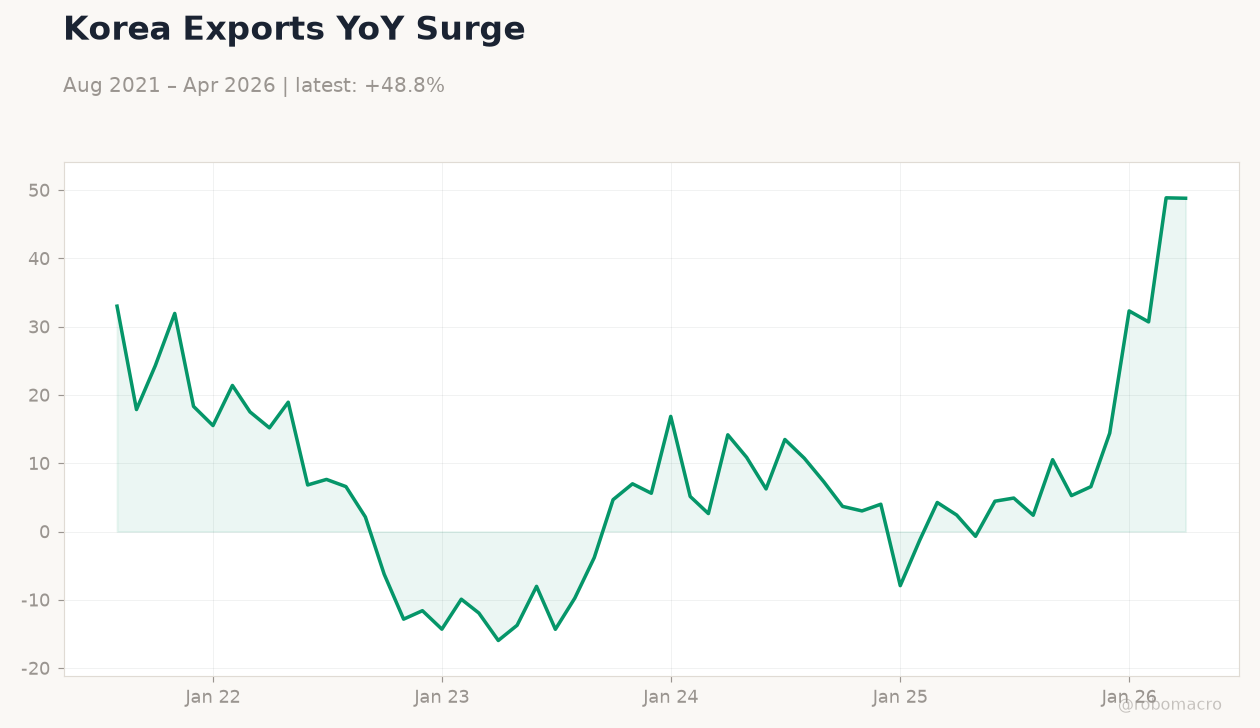

| Exports Year-over-Year | 53.40 | - | 70.90 |

| S&P Global Manufacturing PMI Index | 54.80 | - | 52.10 |

| BoK Gov Shin Speech | - | - | - |

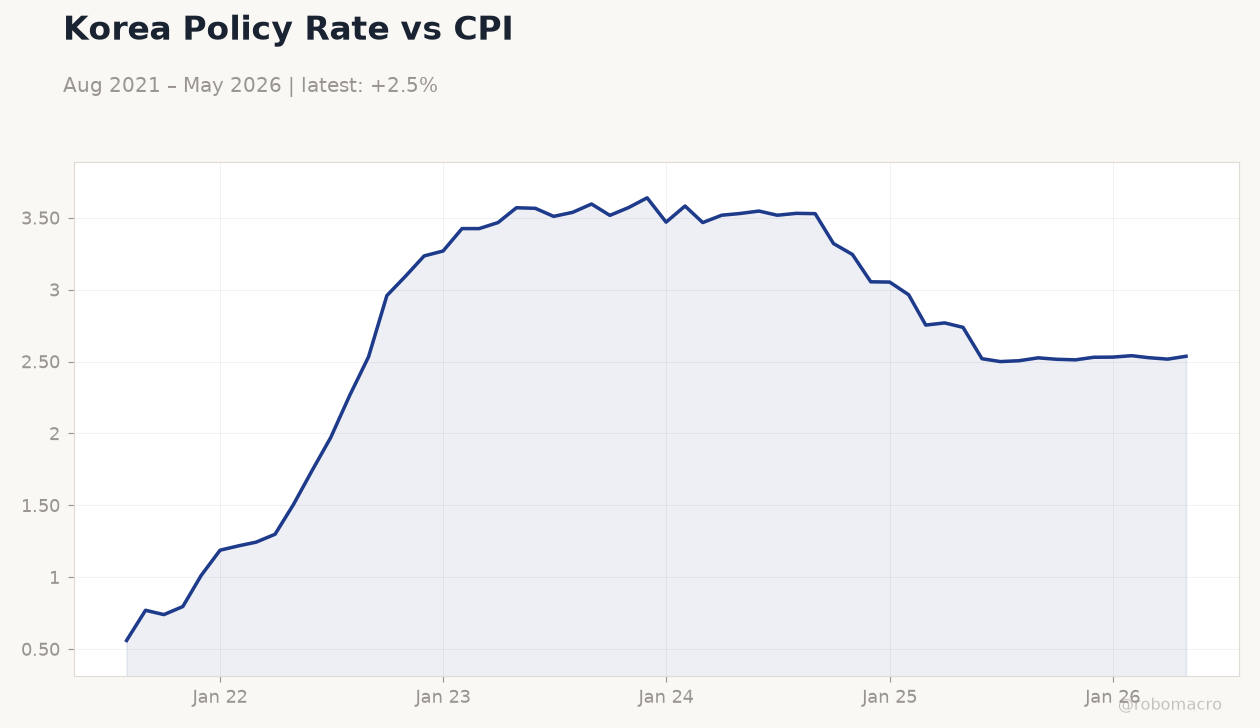

| Inflation Rate Year-over-Year | 3.10 | 3.20 | 3.20 |

Korea Policy Rate vs CPI | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.56–3.639 | Trend(6pt): 0.56,2.959,3.639,2.965,2.517,2.537

Korea Policy Rate vs CPI | Type: macro_line | Short-term Rate %: 2.537 (2026-05-01) | Range: 0.56–3.639 | Trend(6pt): 0.56,2.959,3.639,2.965,2.517,2.537

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- June inflation rose to 3.2% y/y, matching consensus and marking the highest reading in 30 months amid oil and harvest pressures.

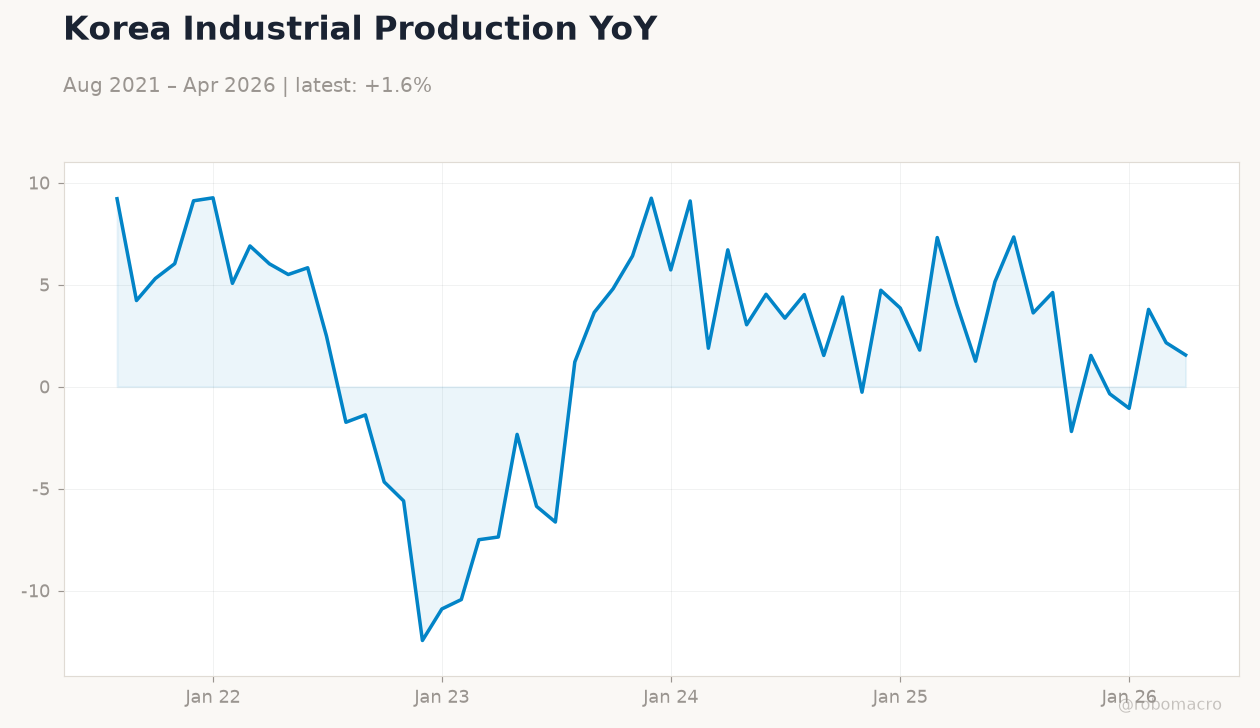

- Exports jumped to 70.9% y/y while manufacturing PMI fell to 52.1, signaling mixed external strength and domestic softening.

- KOSPI dropped 2.04% on semiconductor selloffs as USD/KRW eased 0.60% ahead of 24-hour won trading launch.

Yesterday's Recap

South Korea reported June inflation at 3.2% y/y, up from 3.1% and driven by higher oil prices linked to Iran tensions plus poor harvests. Exports surged 70.9% y/y, far above the prior 53.4%, reflecting robust global demand for Korean goods. The S&P Global Manufacturing PMI slipped to 52.1 from 54.8, pointing to cooling factory momentum.

Governor Shin delivered remarks that markets interpreted as neutral on near-term policy shifts. KOSPI fell 2.04% to 8,303.41 while KOSDAQ rose 1.44%, as Samsung and SK Hynix shares plunged 7.31% and 8.87% respectively on chip price concerns. USD/KRW declined 0.60% to 1,539.25.

Korea’s short-term rate held at 2.54% while the long-term rate climbed sharply to 4.08%.

The Day Ahead

No major data releases are scheduled for July 2. Attention turns to the July 7 start of 24-hour won trading, which authorities expect will deepen global investor access and reduce crisis-era perceptions. Market participants will monitor foreign flows into equities and any follow-up comments from BoK officials.

Semiconductor pricing trends and yen movements remain key external variables. The absence of immediate catalysts leaves KOSPI and KRW sensitive to overnight global risk sentiment.

Other Economic Notes

Record trade surpluses are colliding with foreign equity outflows, keeping the won under pressure despite strong export readings. Government bond yields rose the steepest among major markets this year, reflecting reduced odds of near-term BoK easing. BNK Group’s new 50 billion won fund targets strategic sectors, adding modest policy support for industrial upgrading.

Yen weakness at 40-year lows is amplifying competitiveness concerns for Korean exporters.

Global Macro News

Iran-related supply risks lifted Korean inflation via higher energy costs, echoing similar pressures across Asia. <i>↓ p.2</i>