Mexico Macro Daily(Beta Mode)

Banxico Cuts, Peso Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,061.34 | -1.65% |

| USD/MXN | 18.03 | +1.44% |

| EUR/MXN | 20.75 | +0.96% |

| WTI Crude | 96.52 | +2.16% |

| Silver | 68.24 | +0.83% |

| Gold | 4,450.60 | +1.72% |

| Brent Crude | 103.99 | -3.72% |

| Bitcoin | 66,681.15 | -3.07% |

| Mexico Short-term Rate | 5.56% | -1.24% |

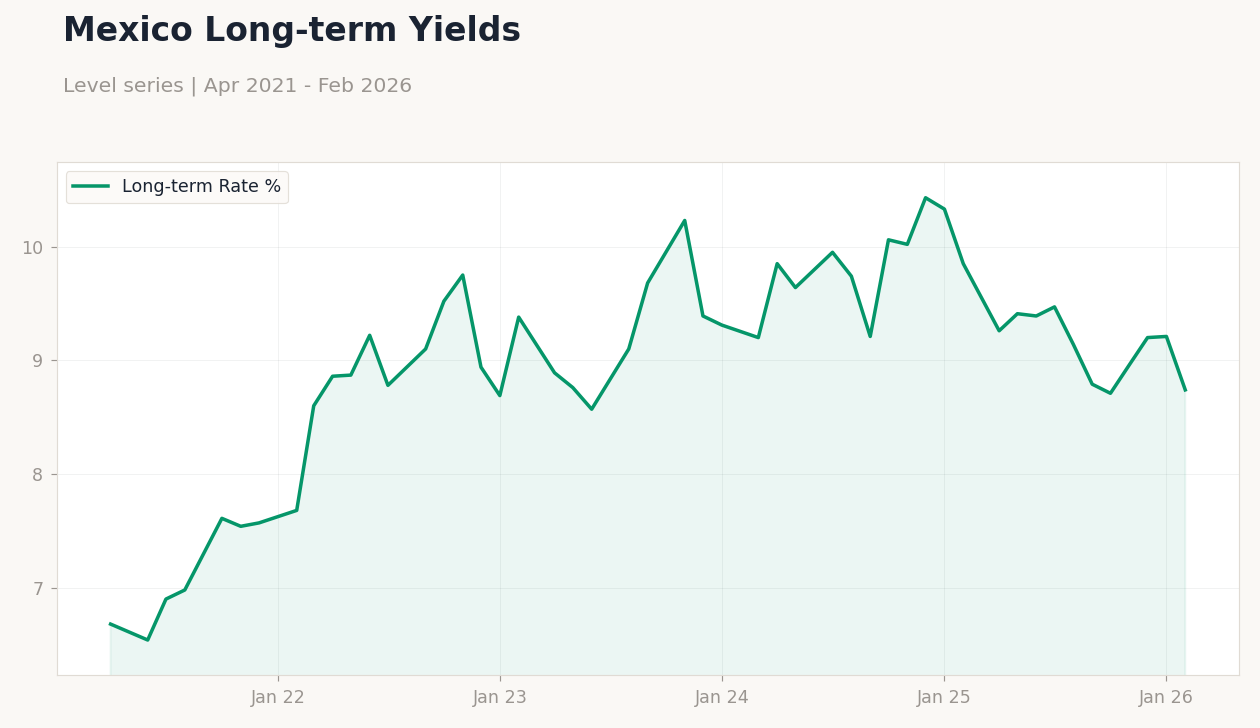

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Central Bank Interest Rate Decision | 7 | 7 | 6.75 |

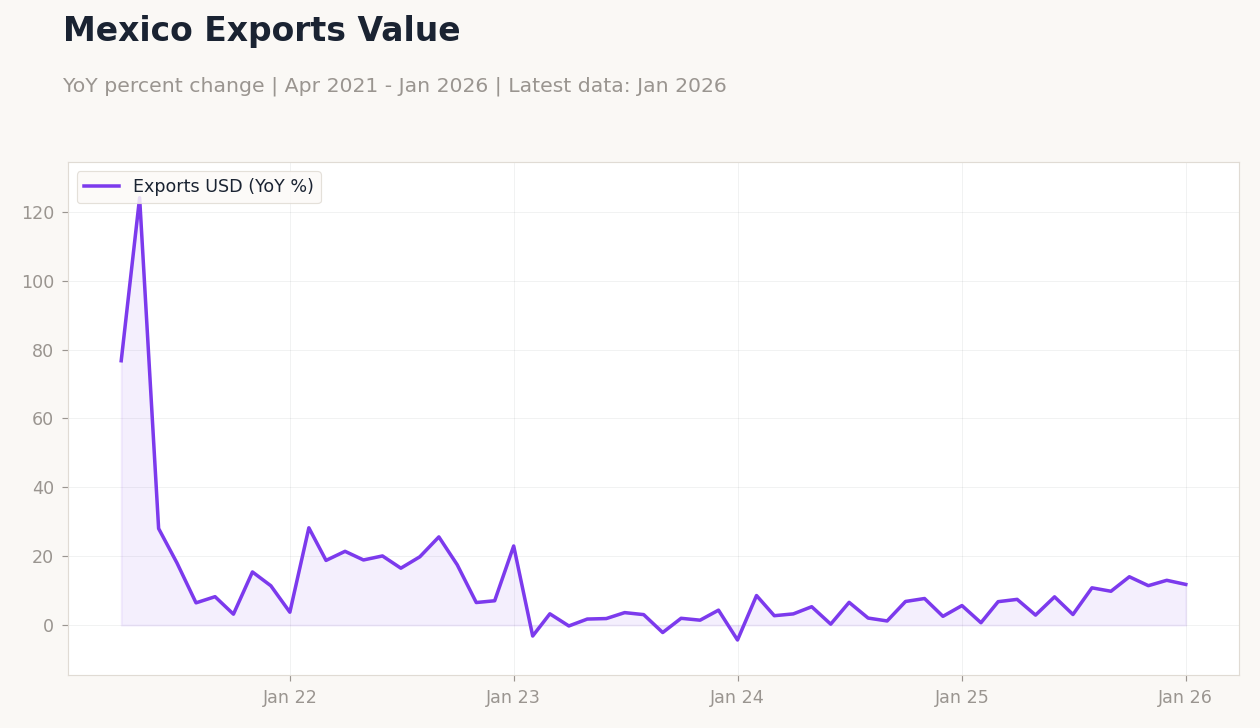

| Trade Balance | -6,481m | 1,200m | - |

Banxico Policy Rate | Type: macro_line | Short-term Rate %: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.11,4.89,8.35,8.25,5.7,5.56

Banxico Policy Rate | Type: macro_line | Short-term Rate %: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.11,4.89,8.35,8.25,5.7,5.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Banxico unexpectedly cut rates to 6.75% amid easing inflation pressures, defying consensus hold at 7%.

- IPC Bolsa fell 1.65% on global risk-off sentiment, while USD/MXN rose 1.44% as the peso depreciated.

- Trade balance data pending release, with markets eyeing potential surplus to support FX stability.

Yesterday's Recap

Banxico surprised markets by lowering its key interest rate to 6.75% from 7%, against consensus expectations of a hold, signaling confidence in moderating inflation despite external risks. The decision triggered a sell-off in Mexican equities, with the IPC Bolsa index closing down 1.65% at 67,061.34, driven by profit-taking in export-oriented sectors amid US trade uncertainties. The peso weakened sharply, pushing USD/MXN up 1.44% to 18.03, as investors reassessed Banxico's dovish pivot in a high global yield environment.

EUR/MXN climbed 0.96% to 20.75, reflecting broader EM currency pressures. Mexico's short-term rate fell 1.24% to 5.56%, aligning with the policy easing, while long-term rates dropped 5.10% to 8.74%, flattening the yield curve. Trade balance figures for February were scheduled but not yet released, leaving markets without fresh export-import insights to counterbalance the rate cut's impact.

Overall, the session highlighted Mexico's sensitivity to monetary policy shifts amid mixed commodity prices, with WTI crude up 2.16% to 96.52 and Brent down 3.72% to 103.99 providing some offset to energy-linked stocks, while gold rose 1.72% to 4,450.60 and silver gained 0.83% to 68.24. Bitcoin declined 3.07% to 66,681.15.

The Day Ahead

Today's calendar is light, with the trade balance release at 4:00 AM ET potentially providing insights into export performance amid peso volatility. Investors will monitor any follow-up statements from Banxico officials on the decision's rationale, which could influence FX moves. Attention also turns to US-Mexico trade dynamics under USMCA, especially with recent news on border immigration declines that may ease logistical pressures.

Broader EM sentiment may drive flows, given global central bank updates from peers like the South African Reserve Bank holding rates. Tomorrow remains quiet, with no events listed, shifting focus to end-of-week positioning ahead of potential Q1 GDP previews.

Other Economic Notes

Nearshoring trends continue to bolster Mexico's manufacturing sector, with US firms relocating operations to capitalize on USMCA advantages amid geopolitical tensions. Remittances remain a key support for consumption, though softening global growth could cap inflows. (cont...)