Mexico Macro Daily(Beta Mode)

IPC Gains, Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,087.64 | +0.60% |

| USD/MXN | 18.02 | -0.66% |

| EUR/MXN | 20.85 | +0.92% |

| WTI Crude | 102.79 | -0.09% |

| Silver | 73.41 | +4.39% |

| Gold | 4,614.90 | +1.96% |

| Brent Crude | 106.96 | -5.16% |

| Bitcoin | 66,568.37 | -0.18% |

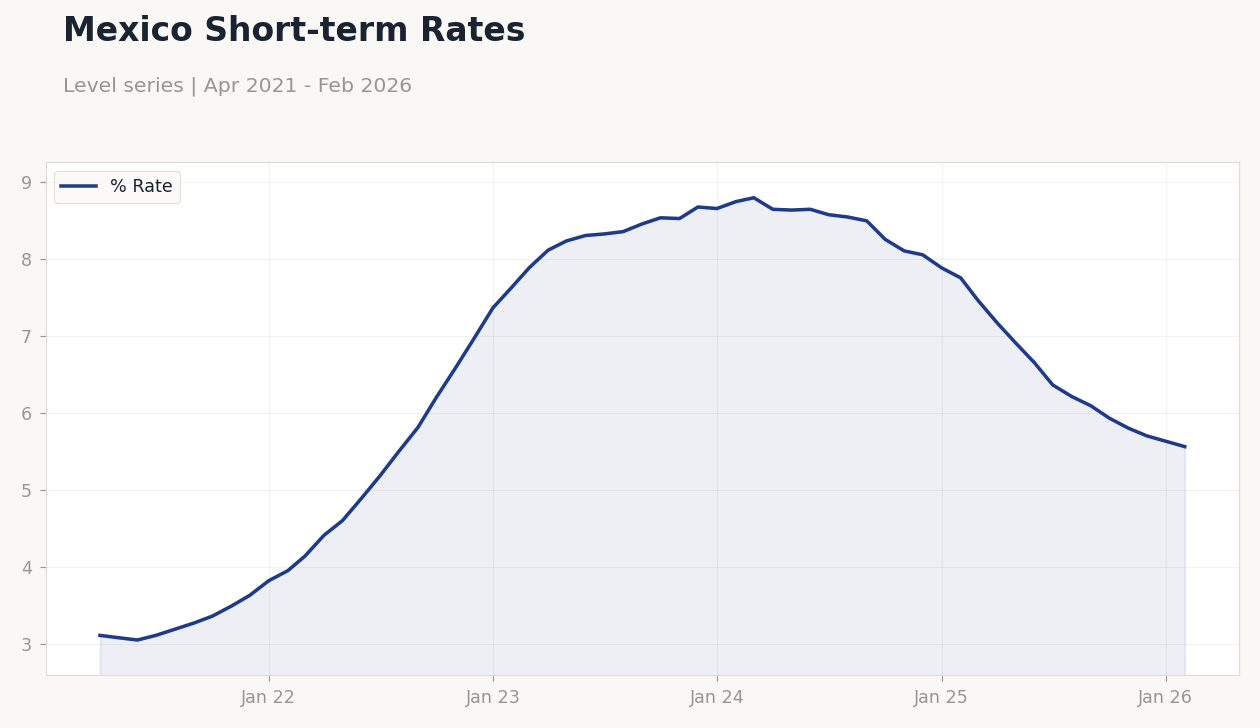

| Mexico Short-term Rate | 5.56% | -1.24% |

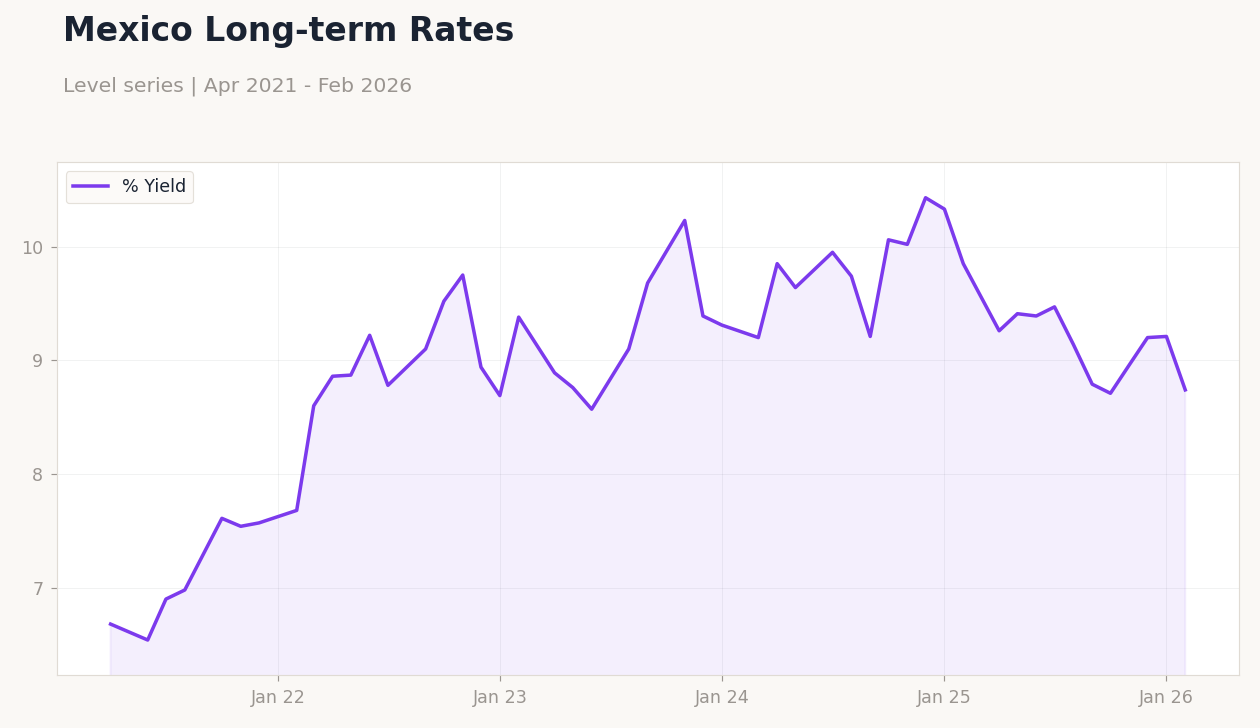

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Rates | Type: macro_line | % Rate: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.11,4.89,8.35,8.25,5.7,5.56

Mexico Short-term Rates | Type: macro_line | % Rate: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.11,4.89,8.35,8.25,5.7,5.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-01) | |||

| Business Confidence Index | 48.10 | - | 04:00 |

- Mexican stocks rose 0.60% amid commodity boosts, despite mixed global sentiment.

- Peso firmed against dollar, down 0.66% to 18.02, on safe-haven flows.

- Yields declined, reflecting stable Banxico outlook amid volatility.

Yesterday's Recap

Mexican markets displayed strength on March 30 with no major data releases. The IPC Bolsa index advanced 0.60% to 67,087.64, supported by commodity-linked gains as silver jumped 4.39% to 73.41 and gold rose 1.96% to 4,614.90, aiding mining sectors. The peso appreciated versus the dollar, with USD/MXN falling 0.66% to 18.02, driven by emerging market inflows despite geopolitical risks.

EUR/MXN increased 0.92% to 20.85 due to euro gains. Oil prices were mixed: WTI crude slipped 0.09% to 102.79, while Brent crude dropped 5.16% to 106.96, weighing on energy stocks. Bitcoin dipped 0.18% to 66,568.37, with limited impact on local markets.

Bond yields eased, with the short-term rate down 1.24% to 5.56% and long-term rate falling 5.10% to 8.74%, consistent with steady Banxico expectations.

The Day Ahead

On April 1, Mexico's Business Confidence Index releases at 04:00 ET, following a prior 48.1 reading with no consensus available. This medium-impact gauge may reflect sentiment in manufacturing and services, influenced by nearshoring and USMCA ties. A positive surprise could support equities and the peso, while weakness might pressure yields amid global uncertainties.

No events today, so focus shifts to digesting international developments like Middle East tensions. Markets may monitor for any impromptu Banxico insights on inflation.

Other Economic Notes

Nearshoring sustains investment inflows to Mexico, bolstered by USMCA amid supply chain realignments, though U.S. tariff uncertainties persist. Remittances provide peso stability and aid consumption despite elevated rates.

Energy reforms encounter legislative delays, balancing Pemex dominance with private sector involvement in oil output. Global surveys signal manufacturing and services slowdowns from war effects, potentially affecting Mexican exports.

Global Macro News

War shockwaves are disrupting global economies, with March surveys showing weakened manufacturing and services activity worldwide, which could impact Mexico's trade. (cont...)