Mexico Macro Daily(Beta Mode)

IPC Dips Amid Infrastructure Push

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,986.63 | -1.03% |

| USD/MXN | 17.88 | +0.19% |

| EUR/MXN | 20.51 | -0.36% |

| WTI Crude | 114.86 | +2.18% |

| Silver | 72.22 | -0.60% |

| Gold | 4,685.30 | +0.61% |

| Brent Crude | 110.70 | +0.85% |

| Bitcoin | 68,333.32 | -0.76% |

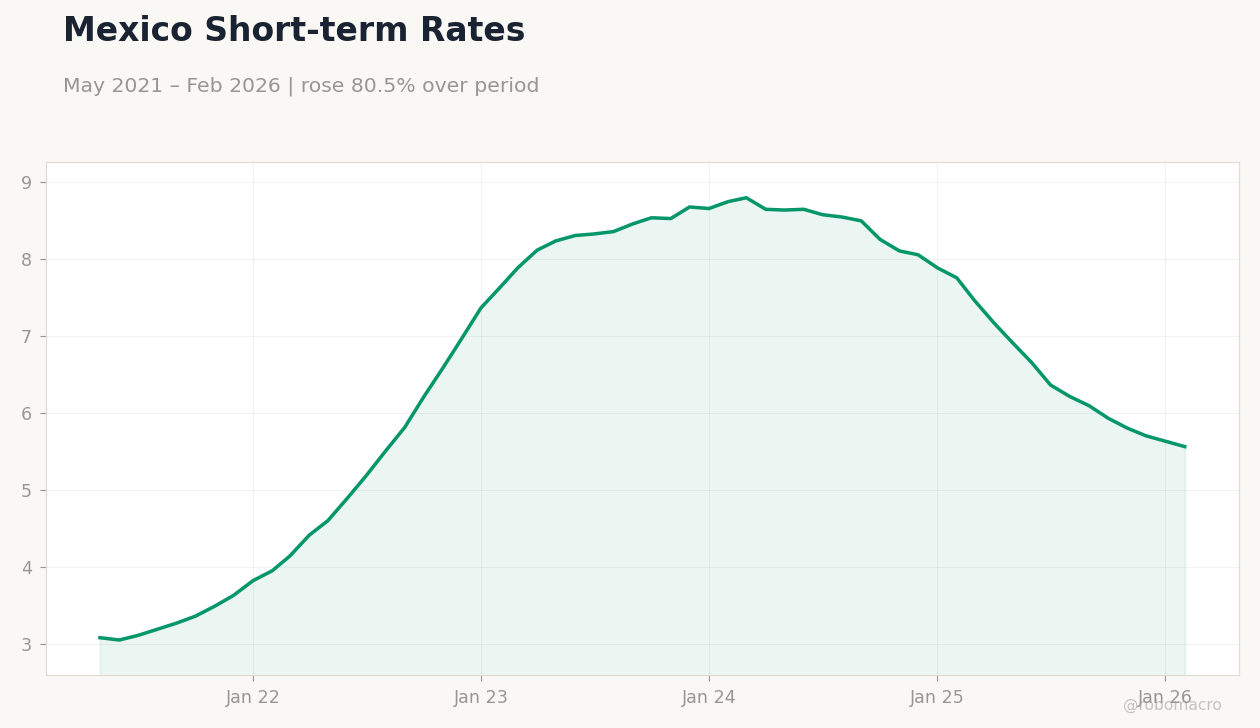

| Mexico Short-term Rate | 5.56% | -1.24% |

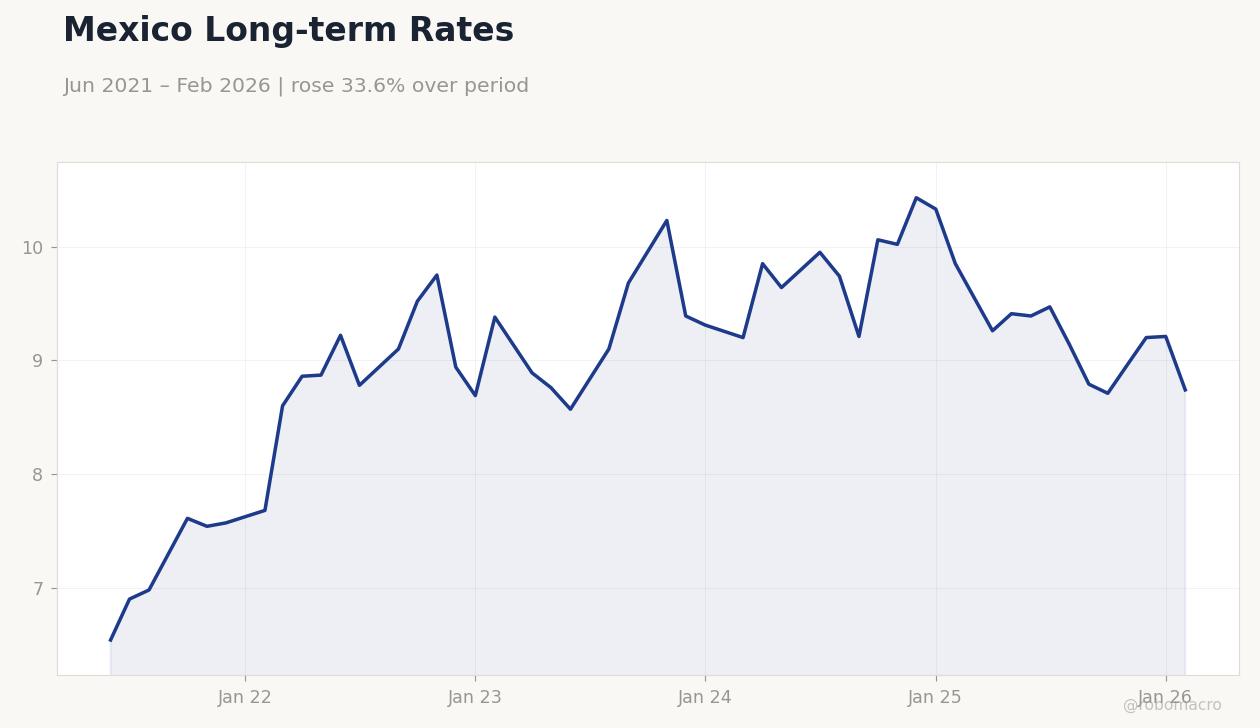

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-08) | |||

| Consumer Confidence Index | 44.40 | - | 04:00 |

| Thursday (2026-04-09) | |||

| Inflation Rate Month-over-Month | 0.50 | 0.88 | 04:00 |

| Inflation Rate Year-over-Year | 4.02 | 4.61 | 04:00 |

- Mexican equities fell 1.03% as global caution weighed, while a new infrastructure law aims to unlock private investment.

- Peso weakened slightly with USD/MXN up 0.19%, but bond rates declined sharply on easing bets.

- No major data releases yesterday; focus shifts to upcoming consumer confidence and inflation figures.

Yesterday's Recap

Mexican markets closed lower amid a risk-off global tone, with the IPC Bolsa index dropping 1.03% to 68,986.63, pressured by declines in energy and materials sectors. The peso softened modestly, as USD/MXN rose 0.19% to 17.88, reflecting broader EM currency weakness, while EUR/MXN fell 0.36% to 20.51 on euro softness. Bond yields tumbled, with the short-term rate down 1.24% to 5.56% and long-term rate plunging 5.10% to 8.74%, signaling market expectations for monetary easing.

Commodity moves were mixed: WTI Crude surged 2.18% to 114.86 and Brent Crude rose 0.85% to 110.70, boosting oil-related sentiment, but silver dipped 0.60% to 72.22 despite gold's 0.61% gain to 4,685.30. Bitcoin fell 0.76% to 68,333.32, adding to the cautious mood. No economic data was released, leaving markets to digest the new infrastructure law announcement, which seeks to accelerate strategic projects and attract private capital.

The Day Ahead

Tomorrow brings Mexico's Consumer Confidence Index at 04:00 ET, with prior reading at 44.4 and no consensus forecast, offering insights into household sentiment amid rising costs. Thursday features the monthly Inflation Rate at 04:00 ET, expected at 0.88% MoM versus 0.5% previous, alongside the yearly rate projected at 4.61% from 4.02%. These prints could influence Banxico's policy outlook, especially if inflation surprises higher.

No events are slated for today, allowing markets to focus on global cues like potential Fed signals.

Other Economic Notes

The new infrastructure law represents a pivotal shift, aiming to unblock investments, enable private capital inflows, and expedite long-term strategic projects critical for growth. This could enhance nearshoring trends by improving logistics and energy infrastructure, potentially supporting US-Mexico trade under USMCA amid ongoing auto and energy disputes. Broader fiscal discipline remains key, with Pemex debt challenges underscoring the need for reforms to sustain investor confidence.