Mexico Macro Daily(Beta Mode)

Peso Gains Amid Trade Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,529.22 | -0.66% |

| USD/MXN | 17.77 | -0.64% |

| EUR/MXN | 20.41 | -0.46% |

| WTI Crude | 93.42 | -17.29% |

| Silver | 77.46 | +7.85% |

| Gold | 4,824.70 | +3.60% |

| Brent Crude | 92.45 | -15.39% |

| Bitcoin | 71,703.14 | -0.33% |

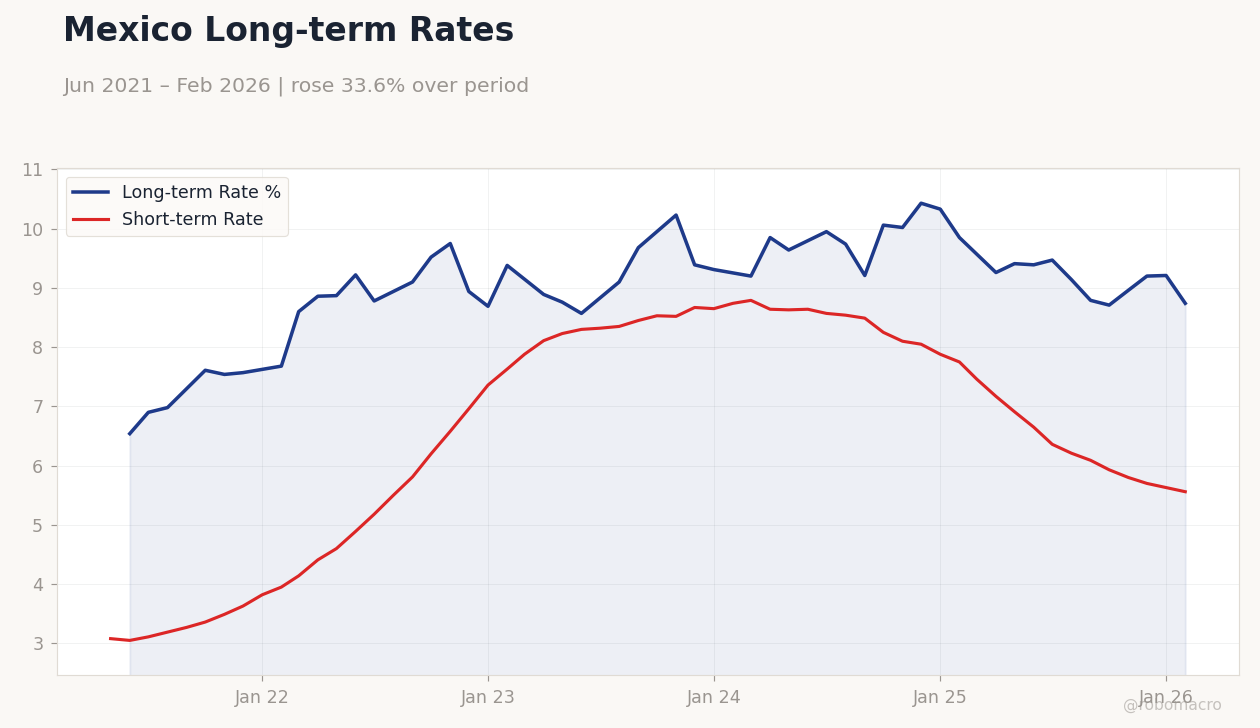

| Mexico Short-term Rate | 5.56% | -1.24% |

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 44.40 | - | - |

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74 | Short-term Rate: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.56

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74 | Short-term Rate: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-09) | |||

| Inflation Rate Month-over-Month | 0.50 | 0.88 | 04:00 |

| Inflation Rate Year-over-Year | 4.02 | 4.61 | 04:00 |

- Peso strengthened on robust US-Mexico trade hitting $147B, offsetting IPC dip from crude volatility.

- Consumer Confidence held steady at prior 44.4, with no new actuals, amid high rates.

- Tariff risks and nearshoring boost highlighted in news, alongside fiscal reform calls.

Yesterday's Recap

Mexican markets showed mixed signals with IPC Bolsa closing at 68,529.22, down 0.66%, weighed by steep crude drops—WTI to $93.42 (-17.29%) and Brent to $92.45 (-15.39%). USD/MXN declined 0.64% to 17.77, driven by strong US-Mexico trade at $147 billion, eclipsing China and Canada volumes. EUR/MXN fell 0.46% to 20.41, supported by remittances and nearshoring.

Precious metals shone: silver up 7.85% to $77.46, gold up 3.60% to $4,824.70, aiding mining stocks despite index pressure. Consumer Confidence Index remained at previous 44.4 with no consensus or actual reported, signaling stable sentiment under elevated rates. Short-term rate at 5.56% (-1.24% change), long-term at 8.74% (-5.10%), reflecting easing bets.

Bitcoin eased 0.33% to $71,703.14, with limited local impact.

The Day Ahead

Focus shifts to tomorrow's inflation releases at 04:00 ET: Month-over-Month expected at 0.88% (prev. 0.5%), Year-over-Year at 4.61% (prev. 4.02%), both medium impact.

Deviations could spark USD/MXN moves amid energy swings. No events today, markets to absorb trade and tariff updates. USMCA dynamics in spotlight, with Trump's metal tariffs on steel, aluminum, copper potentially hitting exports.

Other Economic Notes

BBVA urges tax reform to curb informality, noting growth limits from investment and social spending cuts without changes. US-Mexico trade surged to $147 billion, reducing China and Canada shares, enhancing nearshoring and peso support. UN expert warns of toxic crisis from US waste exports to Mexico due to lax standards.

Telefónica sells Mexico operations to Melisa Acquisition for $450 million, subject to conditions. Advance Metals reports 33Moz silver resource in Mexico, signaling mining potential.

Global Macro News

Fed likely to keep rates high longer on energy inflation, pressuring EM currencies like MXN. Trump's new tariffs on metals risk USMCA frictions amid record Mexico-US trade. Oil plunges exacerbate Mexico's inflation woes, mirroring RBNZ's steady rates under shock pressures.

(cont...)