Mexico Macro Daily(Beta Mode)

Peso Rallies, Yields Tumble

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 69,595.13 | -0.61% |

| USD/MXN | 17.21 | -1.25% |

| EUR/MXN | 20.30 | -0.20% |

| WTI Crude | 97.02 | -2.08% |

| Silver | 77.58 | +2.72% |

| Gold | 4,797.50 | +1.16% |

| Brent Crude | 98.88 | -0.48% |

| Bitcoin | 74,456.00 | -0.04% |

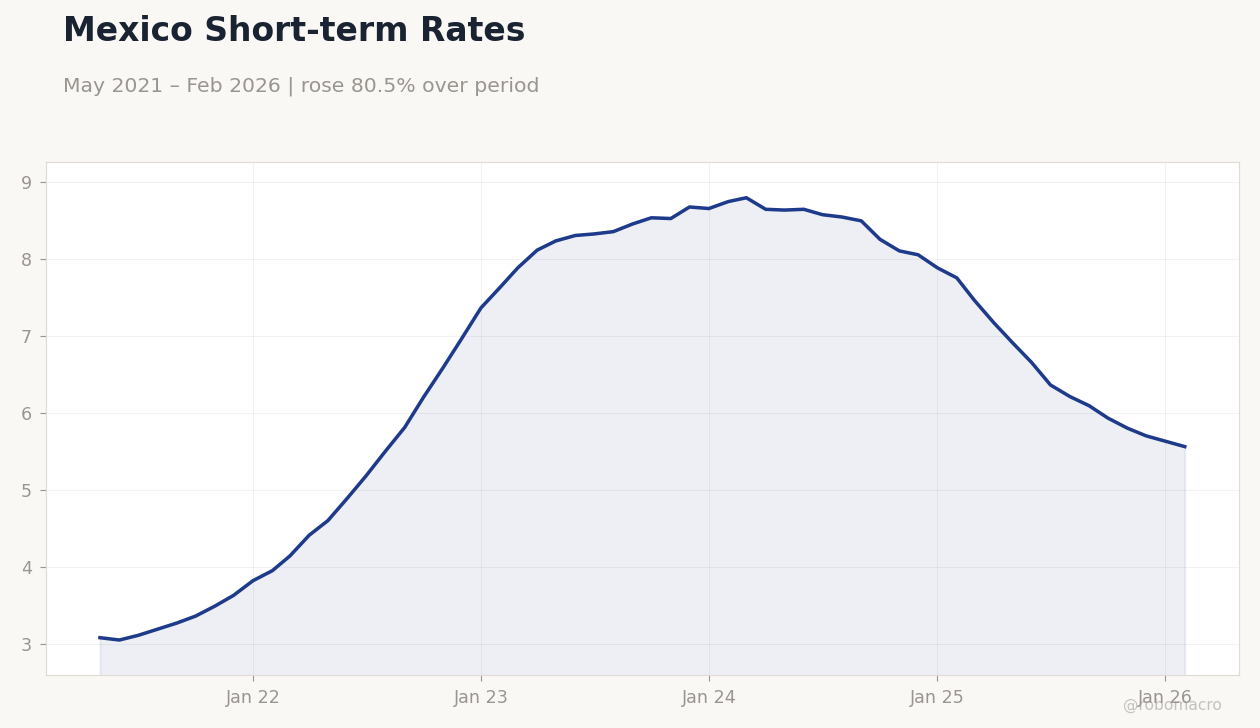

| Mexico Short-term Rate | 5.56% | -1.24% |

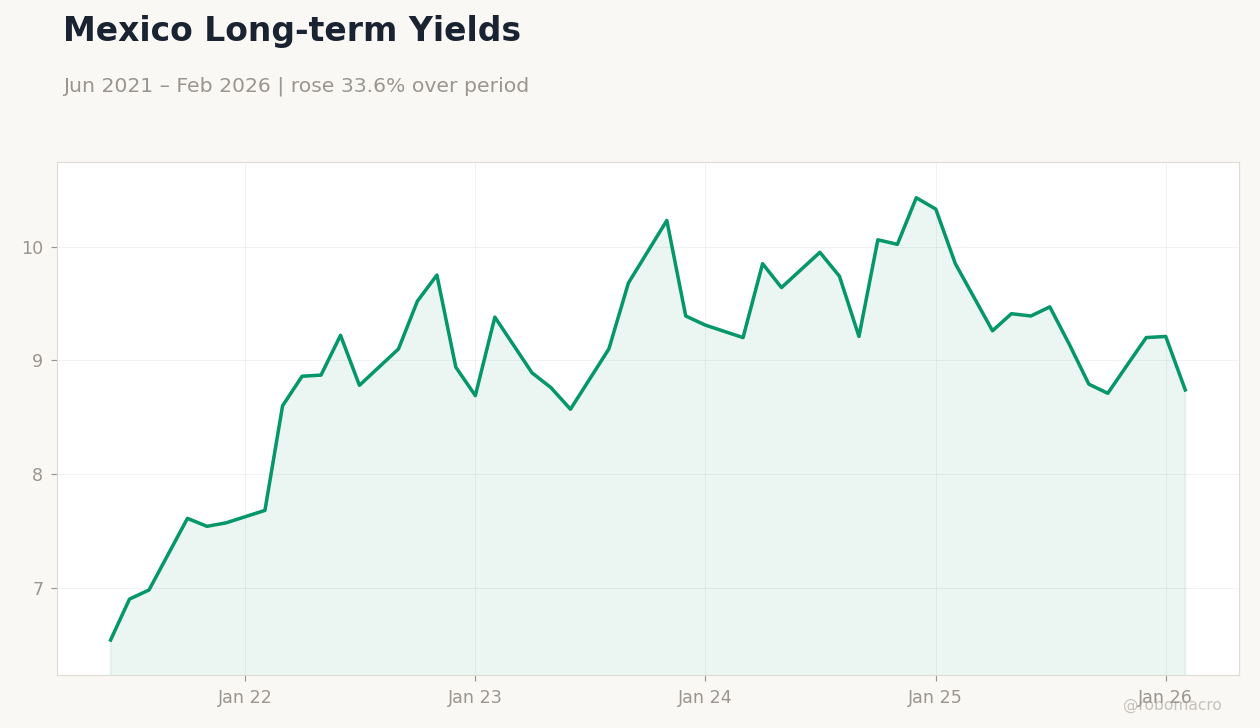

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Rates | Type: macro_line | Short-term Rate %: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.56

Mexico Short-term Rates | Type: macro_line | Short-term Rate %: 5.56 (2026-02-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.56

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- USD/MXN fell 1.25% to 17.21 amid global risk appetite and lower oil prices.

- Mexico rates declined sharply, with long-term yields down 5.10% to 8.74%.

- IPC Bolsa dipped 0.61% to 69,595.13, tracking commodity weakness.

Yesterday's Recap

Mexican markets showed mixed performance with the IPC Bolsa closing down 0.61% at 69,595.13, pressured by declines in energy-linked stocks as WTI Crude dropped 2.08% to 97.02. The peso strengthened notably, with USD/MXN falling 1.25% to 17.21, supported by broader emerging market inflows despite no major data releases. EUR/MXN edged lower by 0.20% to 20.30, reflecting euro weakness against the dollar.

Short-term rates decreased 1.24% to 5.56%, while long-term rates plunged 5.10% to 8.74%, indicating market bets on Banxico easing. Precious metals provided some offset, with silver up 2.72% to 77.58 and gold rising 1.16% to 4,797.50 on safe-haven demand. Brent Crude fell 0.48% to 98.88, adding to commodity sector drags, while Bitcoin held steady with a minimal 0.04% decline to 74,456.00.

Overall, trading volumes remained subdued without economic data catalysts.

The Day Ahead

With no scheduled Mexican data releases tomorrow, markets will likely focus on global cues, including any updates on US-Mexico trade tensions under USMCA. Attention may turn to commodity price movements, particularly oil, given ongoing Middle East conflicts like the Iran war impacting Brent and WTI. Peso dynamics could be influenced by US Treasury yields and Federal Reserve commentary on interest rates.

Banxico observers will watch for any unscheduled statements, though none are anticipated. Broader emerging market sentiment, including China's trade data, might affect IPC Bolsa flows. Expect light volatility unless external shocks arise.

Other Economic Notes

Nearshoring trends continue to support Mexican manufacturing, with potential boosts from USMCA auto rules amid tariff threats. Remittances remain a key consumption driver, though peso strength could moderate inflows. Fiscal discipline under the current administration aims to cap deficits, aiding bond market stability.

Global Macro News

Global interest rate caution persists, with US Treasury Secretary Bessent urging the Federal Reserve to hold rates steady amid the Iran war, potentially strengthening the dollar and pressuring USD/MXN. (cont...)