Mexico Macro Daily(Beta Mode)

Peso Firms Amid Rate Declines

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 70,083.73 | +0.37% |

| USD/MXN | 17.30 | -0.44% |

| EUR/MXN | 20.35 | -0.20% |

| WTI Crude | 87.09 | -2.81% |

| Silver | 78.40 | -1.94% |

| Gold | 4,788.00 | -0.39% |

| Brent Crude | 90.82 | -4.88% |

| Bitcoin | 75,860.04 | -0.02% |

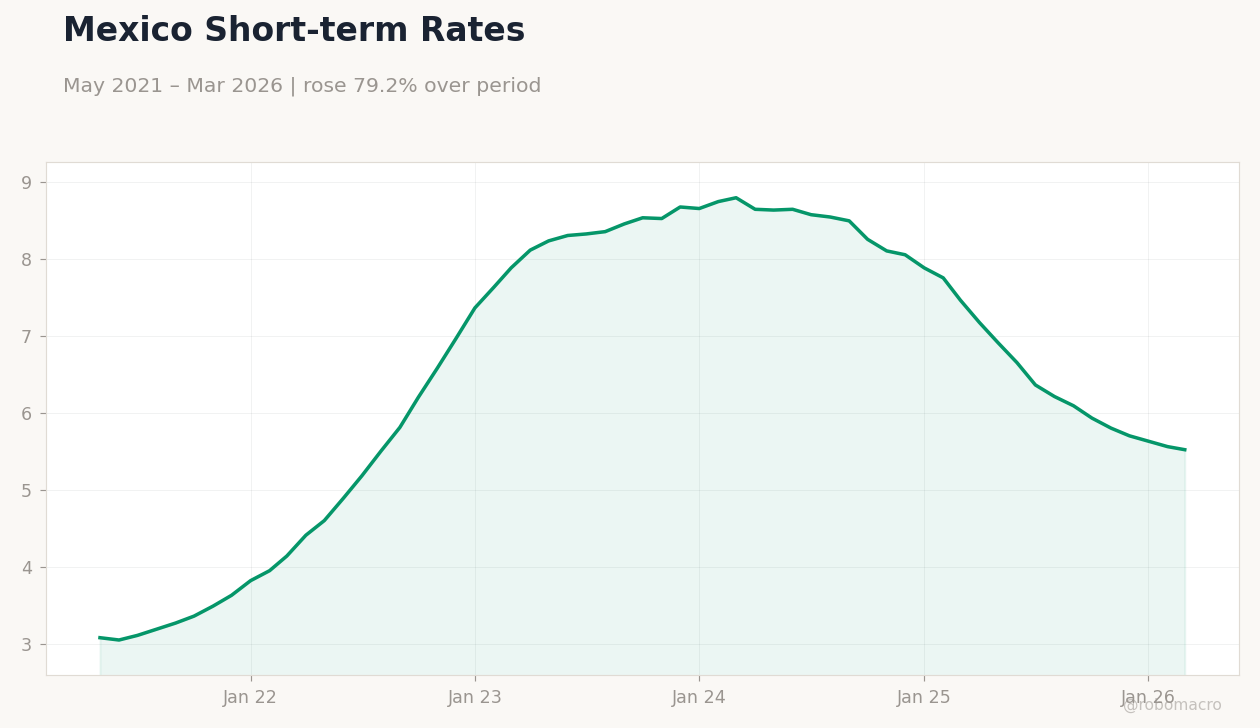

| Mexico Short-term Rate | 5.52% | -0.72% |

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Yields | Type: macro_line | Long-term Yield %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Mexico Long-term Yields | Type: macro_line | Long-term Yield %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa gained 0.37% to 70,083.73 on nearshoring support despite oil weakness.

- USD/MXN fell 0.44% to 17.30, driven by remittance strength and softer dollar.

- Long-term rates dropped 5.10% to 8.74%, signaling Banxico easing expectations.

Yesterday's Recap

Mexican markets displayed mixed performance, with the IPC Bolsa index advancing 0.37% to 70,083.73, lifted by nearshoring-related stocks amid global uncertainties. The USD/MXN rate decreased 0.44% to 17.30, supported by robust remittance data and a weakening dollar. EUR/MXN slipped 0.20% to 20.35, aligning with peso gains.

Mexico's short-term rate fell 0.72% to 5.52%, and the long-term rate declined 5.10% to 8.74%, as investors anticipated potential Banxico policy easing. No significant economic data was released, but a shooting incident at the Teotihuacán pyramids resulted in the death of a Canadian tourist and injuries to others, sparking concerns about tourism safety ahead of Mexico's World Cup co-hosting. Silver prices decreased 1.94% to 78.40, while gold eased 0.39% to 4,788.00, reflecting adjustments in safe-haven demand.

Trading volumes were subdued, with attention on US-Mexico trade relations under USMCA scrutiny.

The Day Ahead

No economic data releases are planned for today, providing space for markets to assess the recent violence's effects on tourism and broader sentiment. Focus will be on Banxico's potential signals regarding interest rate trajectories, given stable inflation trends. US economic indicators may affect cross-border capital flows, especially if they alter Fed rate cut probabilities.

USMCA tariff talks remain a key watchpoint, potentially impacting Mexican exports. Tomorrow also lacks major releases, though fluctuations in global oil prices could influence energy sector assets. Traders should monitor for any impromptu Banxico statements on currency stability.

Other Economic Notes

Nearshoring continues to drive Mexico's high-tech export growth, as US companies redirect from China due to tariffs, likely boosting foreign direct investment. Remittances provide ongoing support to consumer activity, but high fiscal deficits raise concerns over debt levels. Energy reforms encounter investor caution, with preferences for Pemex potentially limiting private sector involvement.

Recent violence poses risks to tourism, which could reduce GDP contributions as Mexico gears up for World Cup events. (cont...)