Mexico Macro Daily(Beta Mode)

Mexican Peso Weakens on Security Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,716.85 | -0.13% |

| USD/MXN | 17.34 | +0.19% |

| EUR/MXN | 20.30 | -0.46% |

| WTI Crude | 92.69 | +0.61% |

| Silver | 77.75 | +1.75% |

| Gold | 4,762.50 | +1.36% |

| Brent Crude | 101.68 | +3.25% |

| Bitcoin | 78,909.75 | +3.35% |

| Mexico Short-term Rate | 5.52% | -0.72% |

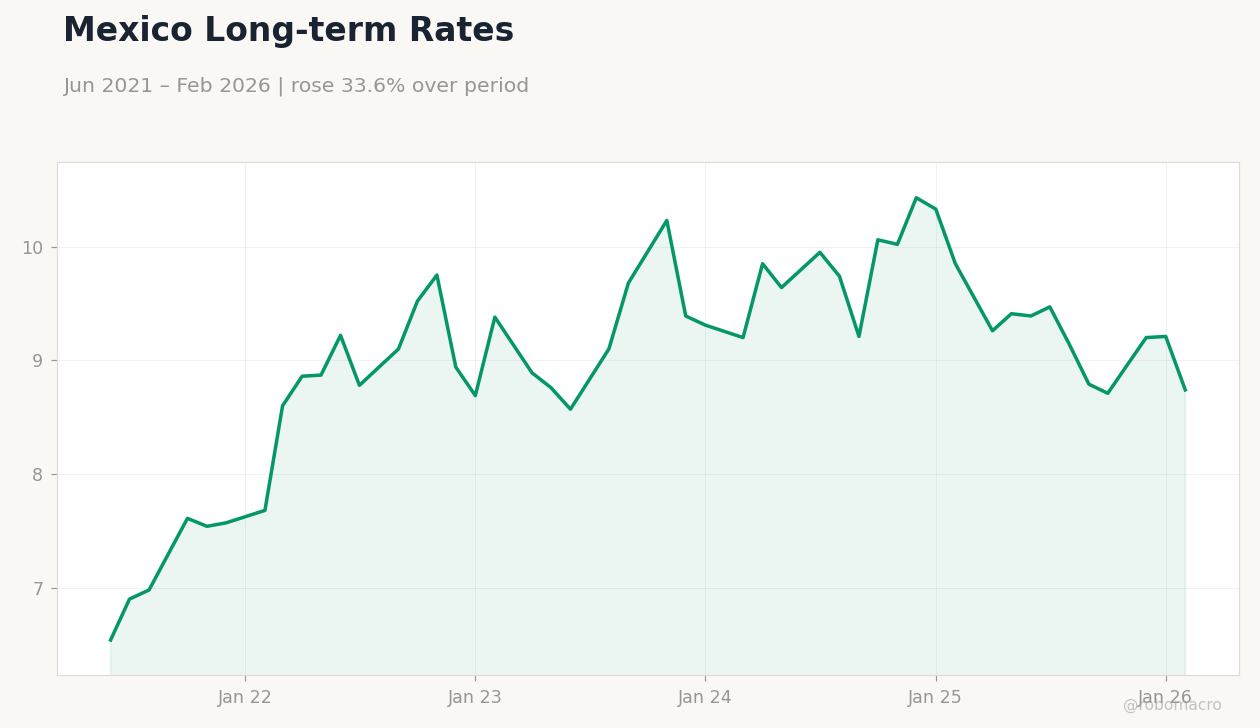

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Rates | Type: macro_line | Short-term Rate %: 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.52

Mexico Short-term Rates | Type: macro_line | Short-term Rate %: 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.52

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexican peso depreciated amid violence at tourist site, raising economic concerns ahead of World Cup.

- Bond yields fell sharply, signaling market bets on Banxico easing despite sticky inflation.

- Global oil gains supported Mexico's energy sector, but equities edged lower on risk aversion.

Yesterday's Recap

Mexican markets closed mixed as security incidents dominated headlines, with a deadly shooting at Teotihuacán pyramids killing a Canadian tourist and injuring others, prompting fears of tourism fallout weeks before Mexico co-hosts the World Cup. The IPC Bolsa index dipped 0.13% to 68,716.85, reflecting investor caution amid broader risk-off sentiment. USD/MXN rose 0.19% to 17.34, weakening the peso on concerns over US-Mexico relations following reports of two CIA agents killed in a post-drug raid crash near Chihuahua.

EUR/MXN fell 0.46% to 20.30, partially offsetting dollar strength. Mexico's short-term rate dropped 0.72% to 5.52%, and long-term rate plunged 5.10% to 8.74%, as yields compressed on safe-haven flows. No major economic data releases occurred, leaving markets to digest news of Japan's plan to import 1 million barrels of Mexican oil, a positive for Pemex amid diversification from Middle East supplies.

Overall, trading volumes were subdued, with precious metals like silver up 1.75% to 77.75 and gold up 1.36% to 4,762.50 providing some offset to equity weakness.

The Day Ahead

The calendar remains light with no scheduled Mexican economic releases or events, shifting focus to potential ripple effects from ongoing investigations into the Teotihuacán shooting and CIA agents' deaths. Markets may monitor any updates on Mexico's probe into possible US constitutional breaches in anti-drug operations, which could strain USMCA trade ties. Broader attention turns to global developments, including any fallout from South Korea's rate cut amid US tariff pressures.

Without domestic catalysts, peso dynamics will likely hinge on oil prices, with Brent crude up 3.25% to 101.68 yesterday. Traders should watch for ad-hoc statements from Mexican officials on tourism recovery efforts, especially joint initiatives with Brazil and others for Cuba relief that could extend to regional stability. Expect low volatility unless external shocks emerge.

Other Economic Notes

Security concerns from the pyramid attack and CIA incident underscore vulnerabilities in Mexico's tourism sector, a key GDP driver, potentially denting remittances and foreign investment as the World Cup approaches. (cont...)