Mexico Macro Daily(Beta Mode)

Power Reforms Ease Trade Jitters

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 69,237.87 | +0.88% |

| USD/MXN | 17.34 | +0.12% |

| EUR/MXN | 20.30 | -0.18% |

| WTI Crude | 95.53 | -0.33% |

| Silver | 75.81 | +0.46% |

| Gold | 4,738.50 | +0.71% |

| Brent Crude | 99.31 | -5.48% |

| Bitcoin | 77,893.25 | -0.48% |

| Mexico Short-term Rate | 5.52% | -0.72% |

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

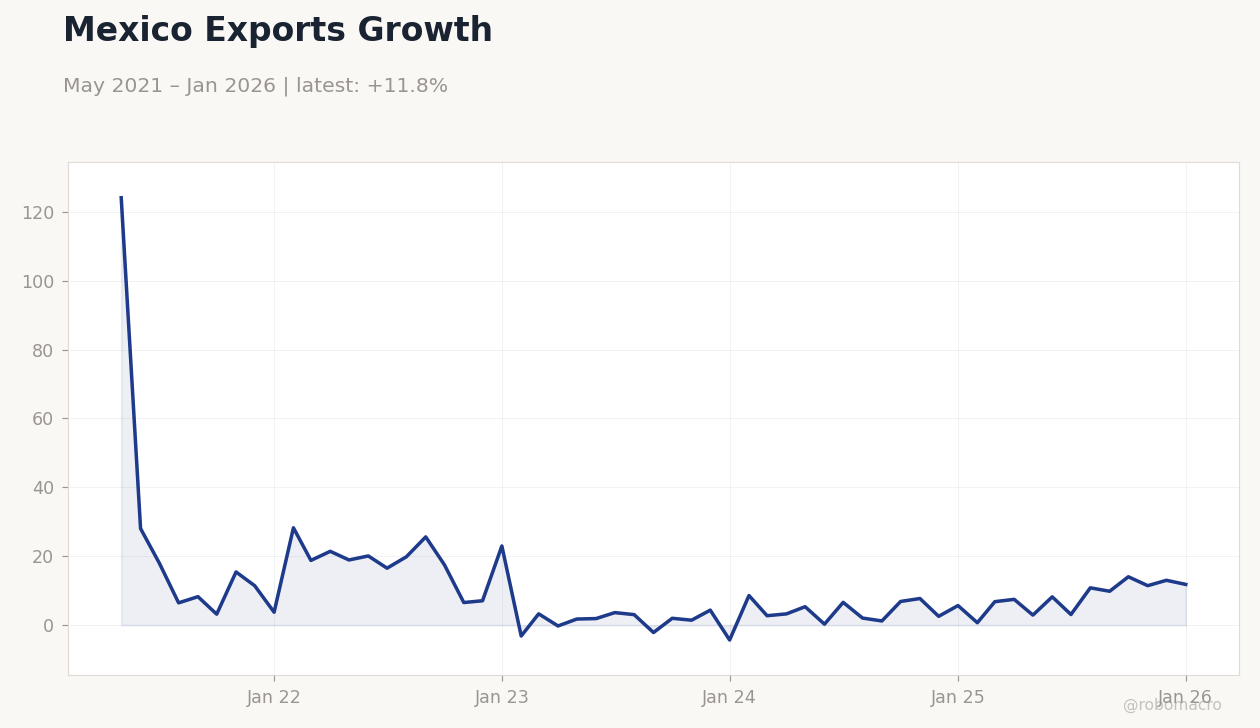

Mexico Exports Growth | Type: macro_line | Exports (YoY %): 11.82 (2026-01-01) | Range: -4.322–124.1 | Trend(5pt): 124.1,16.53,-2.152,7.722,11.82

Mexico Exports Growth | Type: macro_line | Exports (YoY %): 11.82 (2026-01-01) | Range: -4.322–124.1 | Trend(5pt): 124.1,16.53,-2.152,7.722,11.82

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexico revises electricity rules to ease private generator tensions ahead of North American trade talks, boosting market sentiment.

- IPC Bolsa rises 0.88% amid nearshoring optimism, while USD/MXN edges up 0.12% on global rate caution.

- Influx of Chinese EVs into Mexico accelerates before tariff shifts, highlighting USMCA trade dynamics.

Yesterday's Recap

Mexican markets showed resilience yesterday with the IPC Bolsa index climbing 0.88% to close at 69,237.87, driven by gains in export-oriented sectors amid easing trade tensions from revised power regulations. The USD/MXN pair ticked up 0.12% to 17.34, reflecting mild peso pressure from global commodity volatility, while EUR/MXN dipped 0.18% to 20.30 on euro weakness. Mexico's short-term rate fell 0.72% to 5.52%, aligning with recent Banxico stability, and the long-term rate dropped sharply by 5.10% to 8.74%, signaling investor bets on easing fiscal risks.

No major data releases occurred, allowing focus on news-driven moves like the influx of Chinese electric vehicles ahead of potential tariffs. Commodity ties influenced sentiment, with Brent Crude plunging 5.48% to 99.31 amid oversupply fears, though gold rose 0.71% to 4,738.50, providing a hedge for Mexican miners. Overall, equities outperformed amid quiet economic calendars, underscoring nearshoring inflows as a key support.

The Day Ahead

Today's calendar remains light with no scheduled Mexican data releases or events, shifting attention to ongoing trade developments under USMCA. Investors will monitor any follow-up announcements on power rule revisions, which could impact energy sector stocks and foreign investment flows. Broader focus turns to global cues, including US import rerouting trends avoiding tariffs, potentially affecting Mexico's manufacturing exports.

Without domestic catalysts, peso and IPC movements may hinge on commodity prices and international rate decisions. Expect low volatility unless unexpected news emerges on Chinese EV influx or oil import deals with Japan.

Other Economic Notes

Tax evasion in Mexico's cigarette market costs the government 13,500 million pesos annually, with illicit trade comprising 20% of total volume, straining fiscal revenues amid broader anti-evasion efforts. Nearshoring trends gain momentum as Chinese EVs flood into Mexico to preempt tariff changes, positioning the country as a key assembly hub for North American markets. Japan's plan to import 1 million barrels of Mexican oil diversifies energy ties, reducing Middle East dependency and bolstering Mexico's export revenues in a volatile global oil landscape.