Mexico Macro Daily(Beta Mode)

Mexico Trade Surplus Surges, IPC Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,269.29 | -1.06% |

| USD/MXN | 17.38 | -0.21% |

| EUR/MXN | 20.35 | -0.10% |

| WTI Crude | 103.25 | +3.32% |

| Silver | 73.05 | -0.21% |

| Gold | 4,576.90 | -0.32% |

| Brent Crude | 107.50 | -3.38% |

| Bitcoin | 77,597.23 | +1.63% |

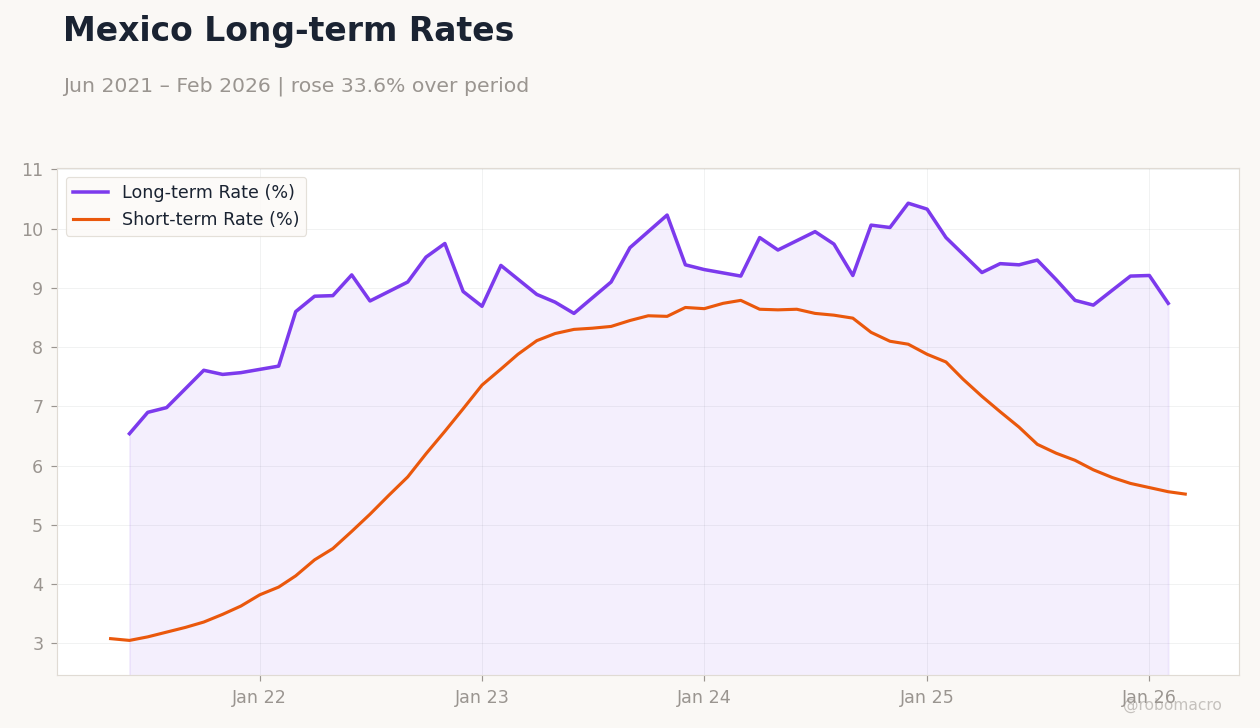

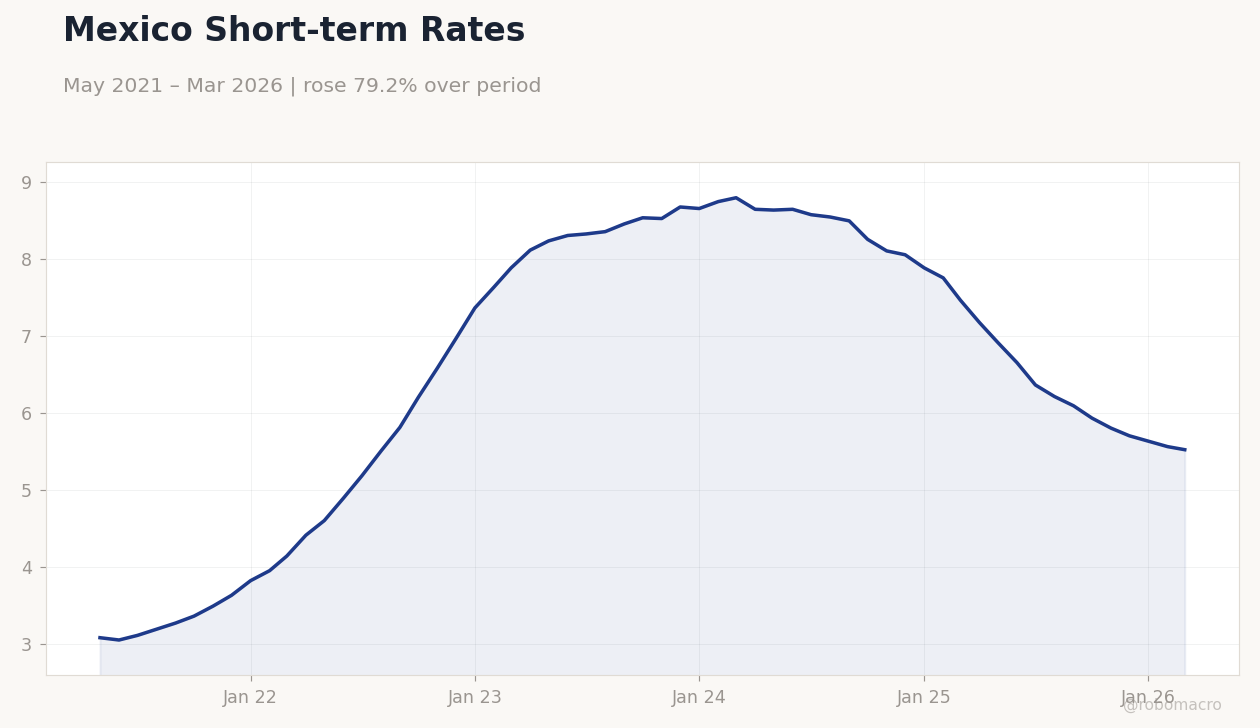

| Mexico Short-term Rate | 5.52% | -0.72% |

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

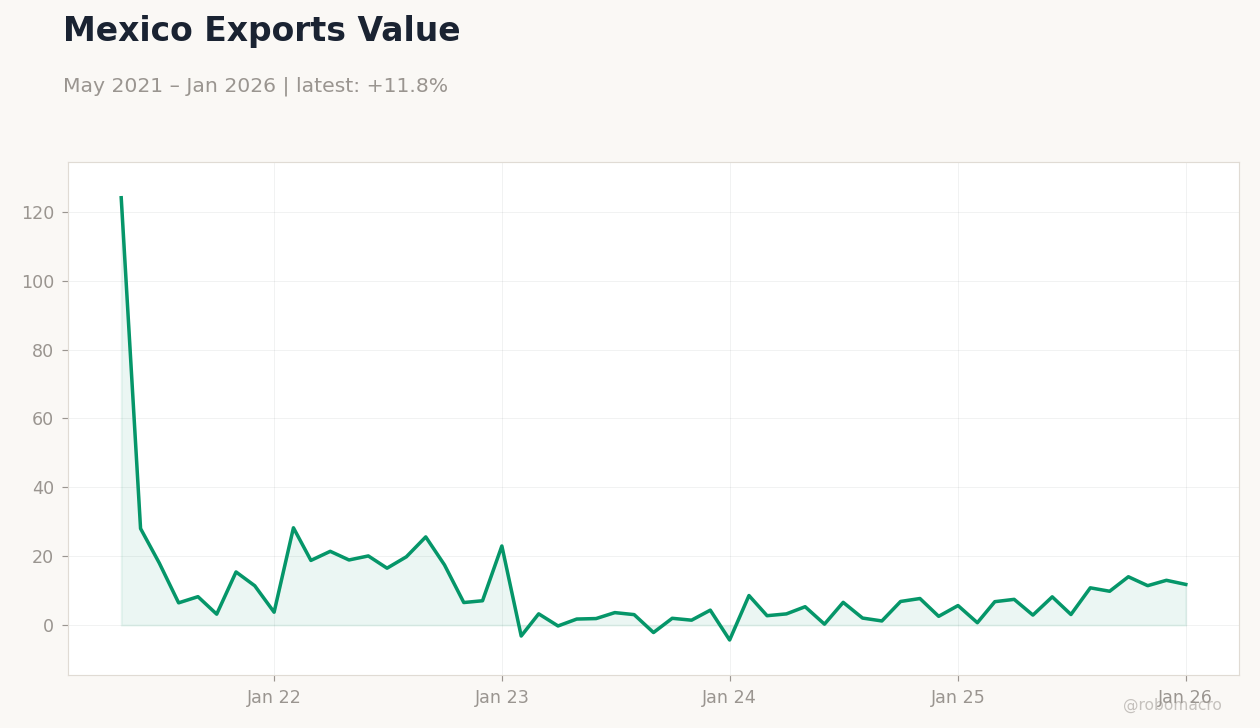

| Trade Balance | -463m | 720m | 5,932m |

Mexico Short-term Rates | Type: macro_line | Short-term Rate (%): 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.52

Mexico Short-term Rates | Type: macro_line | Short-term Rate (%): 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.08,5.18,8.45,8.1,5.63,5.52

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-04-30) | |||

| GDP Growth Quarter-over-Quarter Preliminary | 0.90 | -0.50 | 04:00 |

| GDP Growth Year-over-Year Preliminary | 1.80 | 0.80 | 04:00 |

- Mexico's trade balance hit $5.932B surplus, beating consensus and boosting peso amid inflows.

- IPC Bolsa fell 1.06% on oil volatility, with energy stocks under pressure.

- Banxico holds at 5.52%, eyes on GDP data for policy cues.

Yesterday's Recap

Mexico reported a trade balance of $5.932 billion in March, far exceeding the consensus estimate of $0.72 billion and reversing the previous deficit of -$0.463 billion, driven by strong exports in manufacturing and automotive sectors under USMCA. This positive surprise bolstered the peso, with USD/MXN closing at 17.38 after a 0.21% decline, reflecting increased foreign inflows. However, the IPC Bolsa index fell 1.06% to 67,269.29, weighed down by declines in commodity-exposed stocks amid volatile oil prices.

EUR/MXN edged down 0.10% to 20.35, while Mexico's short-term rate dropped 0.72% to 5.52% and long-term rate plunged 5.10% to 8.74%, signaling easing yield pressures. WTI crude surged 3.32% to $103.25, benefiting Pemex-linked assets, but Brent crude fell 3.38% to $107.50, creating mixed signals for energy trade. Gold and silver dipped slightly by 0.32% and 0.21% respectively, as safe-haven demand waned.

Overall, markets reflected cautious optimism on trade data but broader risk-off from global macro headwinds.

The Day Ahead

No major economic releases are scheduled for today, April 29, providing a brief respite for markets to digest yesterday's trade surplus. Attention shifts to tomorrow's preliminary GDP figures on April 30, with quarter-over-quarter growth expected at -0.5% versus the previous 0.9%, potentially signaling a slowdown in nearshoring momentum. Year-over-year GDP is forecasted at 0.8%, down from 1.8%, which could pressure Banxico's growth outlook and influence peso volatility.

Investors will monitor any spillover from global central bank decisions, such as potential rate holds elsewhere. Banxico has no speeches planned, keeping focus on data-driven policy cues. Markets may trade sideways absent fresh catalysts.

Other Economic Notes

Nearshoring trends continue to support Mexico's economy, with studies highlighting job creation from projects like Pacifico Mexinol in Sinaloa, estimating eight indirect jobs per direct one. Security concerns persist as cartel activities, including illegal logging in Sierra Tarahumara and arrests of Jalisco New Generation leaders, disrupt rural economies and deter foreign investment. Preparations for the 2026 World Cup, including airport renovations in Mexico City, are boosting infrastructure spending and tourism prospects.

(cont...)