Mexico Macro Daily(Beta Mode)

Mexico Business Confidence Ticks Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,590.57 | +1.94% |

| USD/MXN | 17.52 | +0.42% |

| EUR/MXN | 20.30 | -0.86% |

| WTI Crude | 91.81 | -10.23% |

| Silver | 77.79 | +6.41% |

| Gold | 4,710.10 | +3.39% |

| Brent Crude | 99.50 | -9.44% |

| Bitcoin | 82,534.94 | +1.99% |

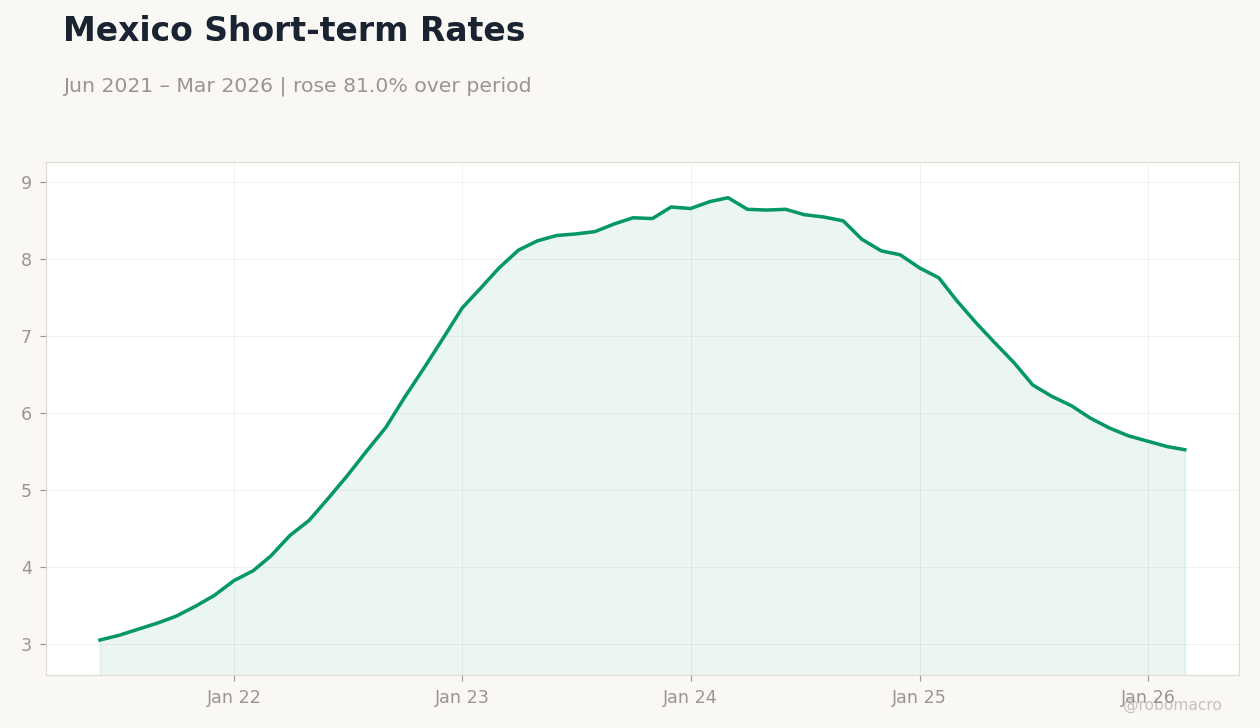

| Mexico Short-term Rate | 5.52% | -0.72% |

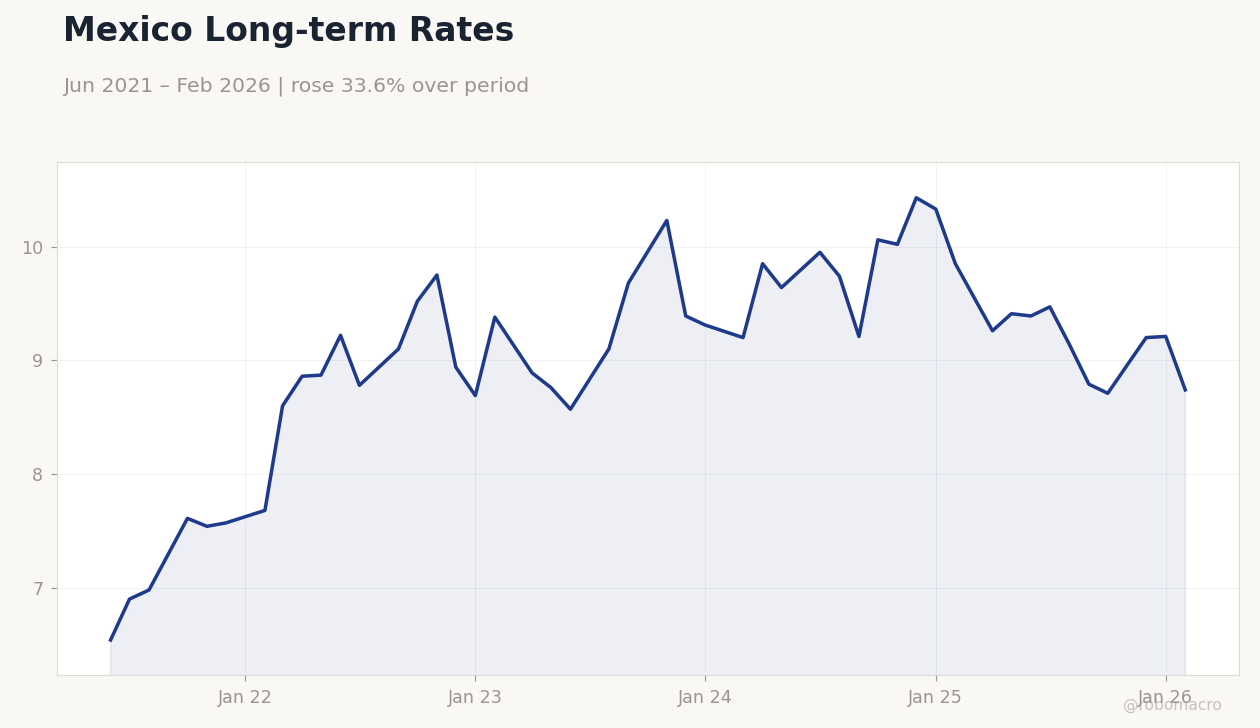

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47.80 | - | 47.90 |

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Mexico Long-term Rates | Type: macro_line | Long-term Rate %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-07) | |||

| Inflation Rate Month-over-Month | 0.86 | 0.25 | 04:00 |

| Inflation Rate Year-over-Year | 4.59 | 4.50 | 04:00 |

| Central Bank Interest Rate Decision | 6.75 | 6.50 | 11:00 |

| Friday (2026-05-08) | |||

| Consumer Confidence Index | 44.10 | - | 04:00 |

- Mexico's Business Confidence Index rose slightly to 47.9 in April, signaling modest improvement amid nearshoring trends.

- IPC Bolsa surged 1.94% on telecom gains, while USD/MXN strengthened 0.42% amid global USD rally.

- Oil prices plunged, with WTI down 10.23% and Brent 9.44%, pressuring Mexico's energy sector.

Yesterday's Recap

Mexico's Business Confidence Index for April edged up to 47.9 from 47.8 prior, reflecting cautious optimism among firms driven by USMCA-related investments despite global headwinds. The IPC Bolsa index climbed 1.94% to 68,590.57, supported by strong performances in consumer and telecom stocks amid robust beer demand from AB InBev's regional volumes. USD/MXN rose 0.42% to 17.52, as the peso weakened on broader USD strength and falling oil prices.

EUR/MXN declined 0.86% to 20.30, benefiting from euro softness. Mexico's short-term rate fell 0.72% to 5.52%, while the long-term rate dropped 5.10% to 8.74%, indicating market bets on easing amid disinflation signals. Commodity moves weighed on sentiment, with WTI Crude tumbling 10.23% to 91.81 and Brent Crude down 9.44% to 99.50, impacting Pemex-linked assets.

Overall, markets showed resilience, with Silver up 6.41% to 77.79 and Gold rising 3.39% to 4,710.10, offsetting some energy losses.

The Day Ahead

Investors eye Mexico's upcoming inflation data on May 7, with month-over-month expected at 0.25% versus 0.86% prior, potentially influencing Banxico's rate path. Year-over-year inflation is forecasted at 4.50% from 4.59%, a key gauge for core pressures amid food and energy volatility. Banxico's interest rate decision follows at 11:00 ET on May 7, with consensus pointing to a cut to 6.5% from 6.75%, aligning with global easing trends.

Consumer Confidence Index releases on May 8, building on April's 44.1 reading, to assess household sentiment post-Cinco de Mayo spending. No major events are slated for May 5 or 6, allowing markets to digest yesterday's data. Focus remains on US-Mexico trade dynamics under USMCA, especially with infrastructure investments announced.

Other Economic Notes

Mexico's infrastructure push gains traction as MIP Real Assets targets $12 billion for renewable energy projects, bolstering nearshoring amid USMCA stability. Remittances and consumer spending remain supportive, evidenced by AB InBev's volume beat in Mexico offsetting US sluggishness. Aviation growth lags regional peers like Argentina, highlighting needs for transport upgrades to sustain tourism and trade.