Mexico Macro Daily(Beta Mode)

IPC Softens, Commodities Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 70,036.66 | -0.30% |

| USD/MXN | 17.23 | +0.22% |

| EUR/MXN | 20.22 | -0.15% |

| WTI Crude | 101.66 | +3.66% |

| Silver | 88.15 | +3.12% |

| Gold | 4,732.40 | +0.29% |

| Brent Crude | 107.14 | +2.81% |

| Bitcoin | 80,474.16 | -1.53% |

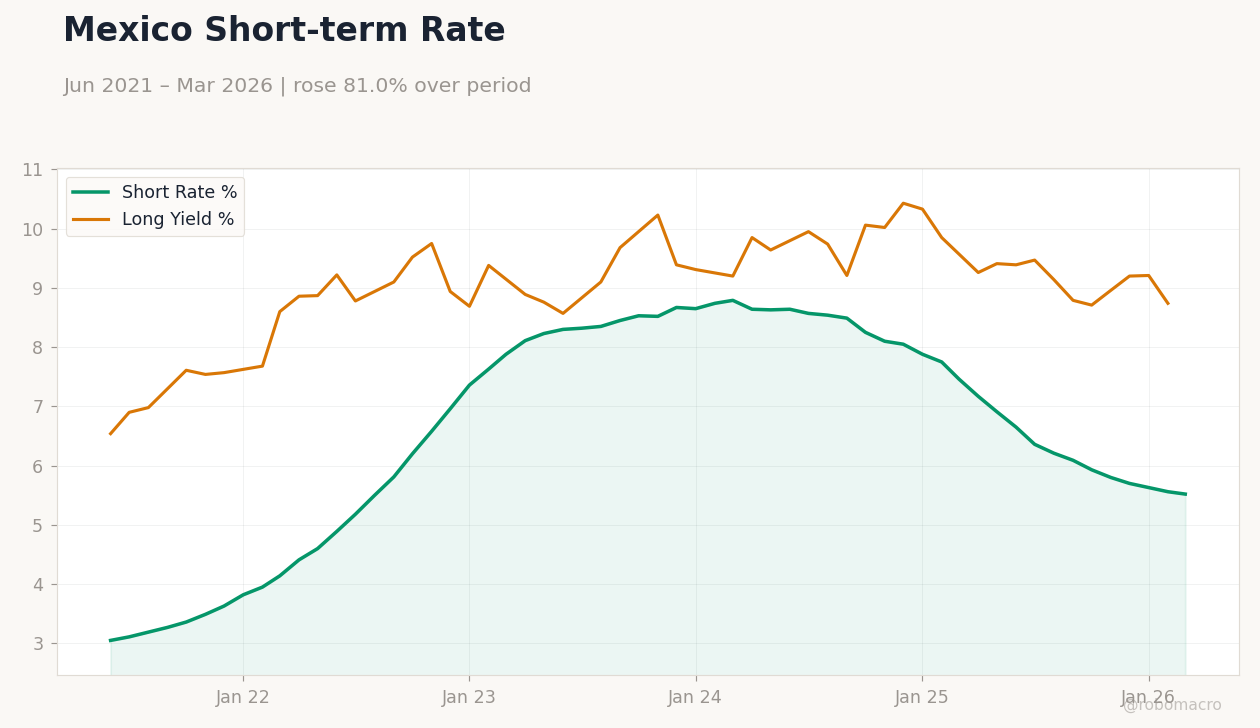

| Mexico Short-term Rate | 5.52% | -0.72% |

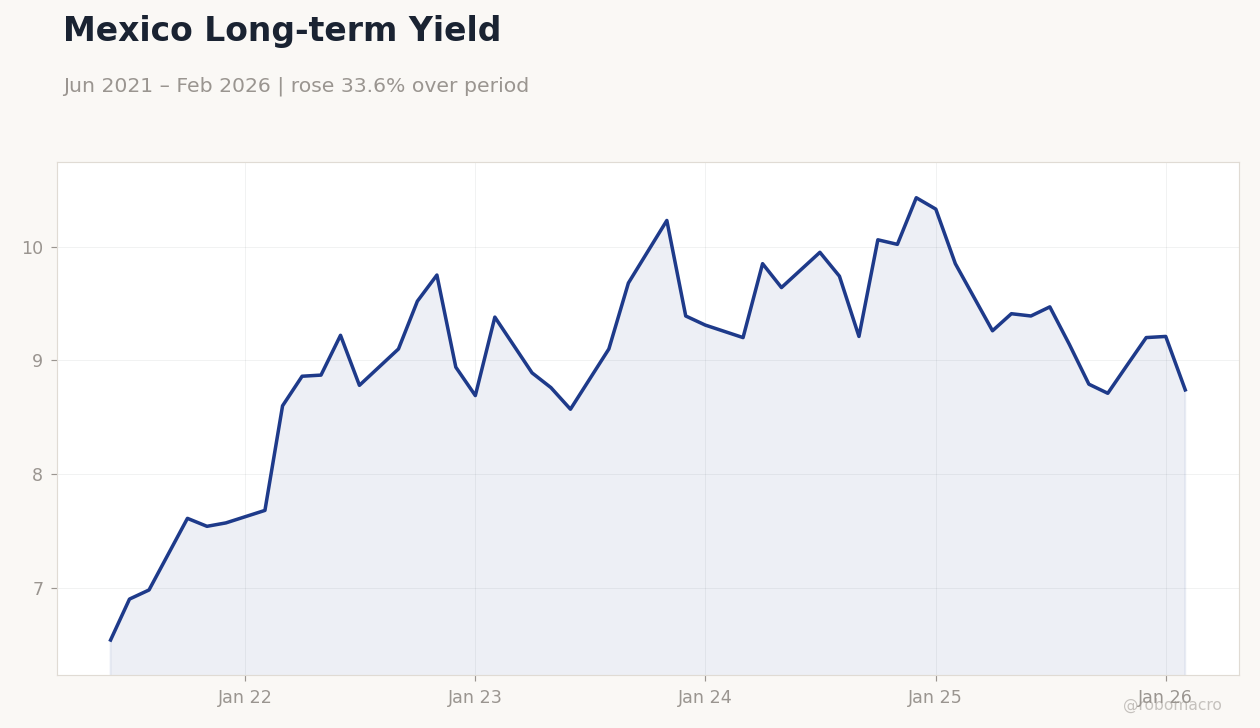

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Yield | Type: macro_line | 10Y Yield %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Mexico Long-term Yield | Type: macro_line | 10Y Yield %: 8.74 (2026-02-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa dipped 0.30% amid global volatility, while USD/MXN rose 0.22% on emerging market pressures.

- Bond rates eased notably, with short-term at 5.52% (-0.72%) and long-term at 8.74% (-5.10%), signaling potential Banxico shifts.

- Commodities surged, led by WTI crude (+3.66%) and silver (+3.12%), bolstering Mexico's export outlook despite border challenges.

Yesterday's Recap

Mexican markets displayed mixed signals on May 11, with the IPC Bolsa index settling at 70,036.66 following a 0.30% drop, attributed to profit-taking in major sectors and lighter trading activity. The peso weakened slightly against the dollar, as USD/MXN climbed 0.22% to 17.23, influenced by higher U.S. yields impacting emerging currencies.

Conversely, EUR/MXN declined 0.15% to 20.22, aided by eurozone resilience. Bond yields fell, with the short-term rate decreasing 0.72% to 5.52% and the long-term rate dropping 5.10% to 8.74%, reflecting market anticipation of softer monetary policy from Banxico. Commodity strength provided a lift, as WTI crude advanced 3.66% to 101.66 and silver rose 3.12% to 88.15, supporting export-oriented firms.

No key economic data was released, but border-related news, including migrant deaths in Texas rail yards and sewage contamination from the Tijuana River affecting U.S. beaches, underscored ongoing US-Mexico trade frictions under USMCA. A Padres prospect's guilty plea in a smuggling case further highlighted immigration tensions.

Despite these, markets held firm, underpinned by nearshoring momentum and robust trade flows.

The Day Ahead

May 12 features no major Mexican economic indicators, giving markets space to absorb recent commodity upticks and global headlines. Traders may watch for impromptu Banxico statements, though none are planned, which could sway peso movements. Focus could turn to US-Mexico logistics updates, such as tightening trucking capacity noted by Uber Freight and expanding B2B financing options.

Commodity trends, including oil and metals, might aid IPC Bolsa rebound if sustained. Escalating border issues from smuggling or pollution reports could weigh on cross-border stocks. Trading is likely subdued absent surprises from international macro events.

Other Economic Notes

Nearshoring continues to fuel Mexico's economic durability, with the B2B buy-now-pay-later sector forecasted to hit $1.97 billion by 2026, driven by platforms like Konfio, Tribal, and Mundi offering SME credit amid SPEI's instant payments. USMCA dynamics remain crucial, as Mexican exports to the U.S. <i>↓ p.2</i>