Mexico Macro Daily(Beta Mode)

IPC Drops, Peso Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 69,206.85 | -1.40% |

| USD/MXN | 17.35 | +1.07% |

| EUR/MXN | 20.17 | +0.30% |

| WTI Crude | 99.89 | -1.27% |

| Silver | 78.07 | -8.06% |

| Gold | 4,559.30 | -2.54% |

| Brent Crude | 108.24 | +2.38% |

| Bitcoin | 80,215.56 | -1.03% |

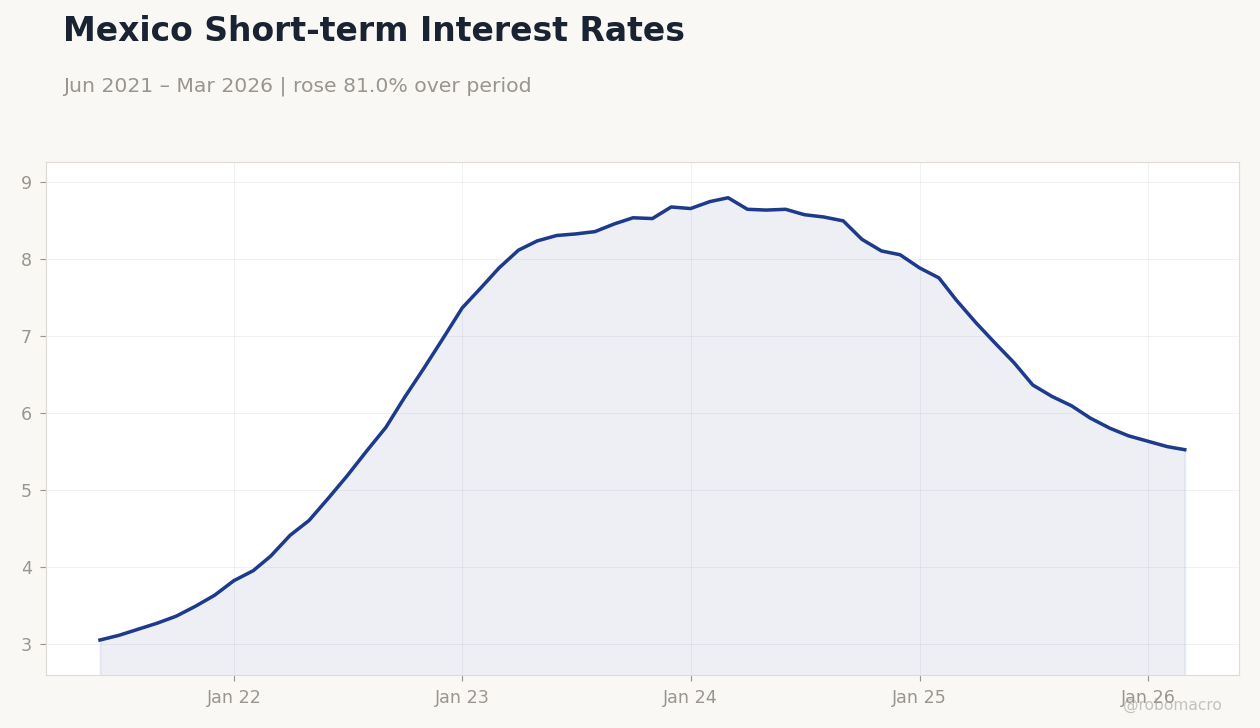

| Mexico Short-term Rate | 5.52% | -0.72% |

| Mexico Long-term Rate | 8.74% | -5.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Short-term Interest Rates | Type: macro_line | Short Rate %: 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.52

Mexico Short-term Interest Rates | Type: macro_line | Short Rate %: 5.52 (2026-03-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.52

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexican equities declined amid global risk-off sentiment, with IPC Bolsa down 1.40% to 69,206.85.

- Peso depreciated versus dollar, USD/MXN up 1.07% to 17.35, pressured by rising US yields.

- Bond yields eased, short-term rate at 5.52% (-0.72%) and long-term at 8.74% (-5.10%).

Yesterday's Recap

Mexican markets experienced a risk-off session with no major data releases, as the IPC Bolsa index fell 1.40% to close at 69,206.85, driven by declines in cyclical sectors amid global commodity volatility. The peso weakened against the dollar, with USD/MXN rising 1.07% to 17.35, reflecting safe-haven flows into the greenback and higher US Treasury yields. EUR/MXN edged up 0.30% to 20.17, showing modest euro resilience but overall peso pressure.

Bond markets saw yields compress, with the short-term rate dropping 0.72% to 5.52% and long-term rate falling 5.10% to 8.74%, as investors priced in potential Banxico easing amid subdued inflation signals. Commodity-linked assets mixed, with silver plunging 8.06% to 78.07 and gold down 2.54% to 4,559.30, weighing on mining-exposed equities. Bitcoin dipped 1.03% to 80,215.56, aligning with broader crypto caution.

Overall, the quiet data calendar amplified focus on external factors like oil price swings, with WTI down 1.27% to 99.89 and Brent up 2.38% to 108.24.

The Day Ahead

Today's calendar remains light with no scheduled Mexican economic releases or events, shifting attention to global developments that could influence peso and equity flows. Markets will monitor US economic indicators for clues on Fed policy, given Mexico's trade linkages under USMCA. Nearshoring trends may gain traction from any updates on cross-border logistics, as highlighted in recent trucking market reports.

Banxico speakers are absent, so forward guidance implications will hinge on prior communications. Investors should watch commodity movements, especially oil, for impacts on Mexico's export revenues. Overall, a subdued session could see volatility driven by external macro news.

Other Economic Notes

Nearshoring continues to bolster Mexican manufacturing, with FDI inflows supporting industrial hubs amid USMCA-driven supply chain shifts. Remittances remain a key consumption driver, potentially offsetting any domestic demand softness in a high-rate environment. <i>↓ p.2</i>