Mexico Macro Daily(Beta Mode)

Mexico IPC Slips as Fiscal Worries Mount

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 67,976.50 | -1.78% |

| USD/MXN | 17.30 | +0.39% |

| EUR/MXN | 20.14 | +0.23% |

| WTI Crude | 100.91 | -4.28% |

| Silver | 76.90 | -0.34% |

| Gold | 4,557.30 | +0.03% |

| Brent Crude | 109.28 | +0.02% |

| Bitcoin | 77,288.50 | -0.18% |

| Mexico Short-term Rate | 5.43% | -1.63% |

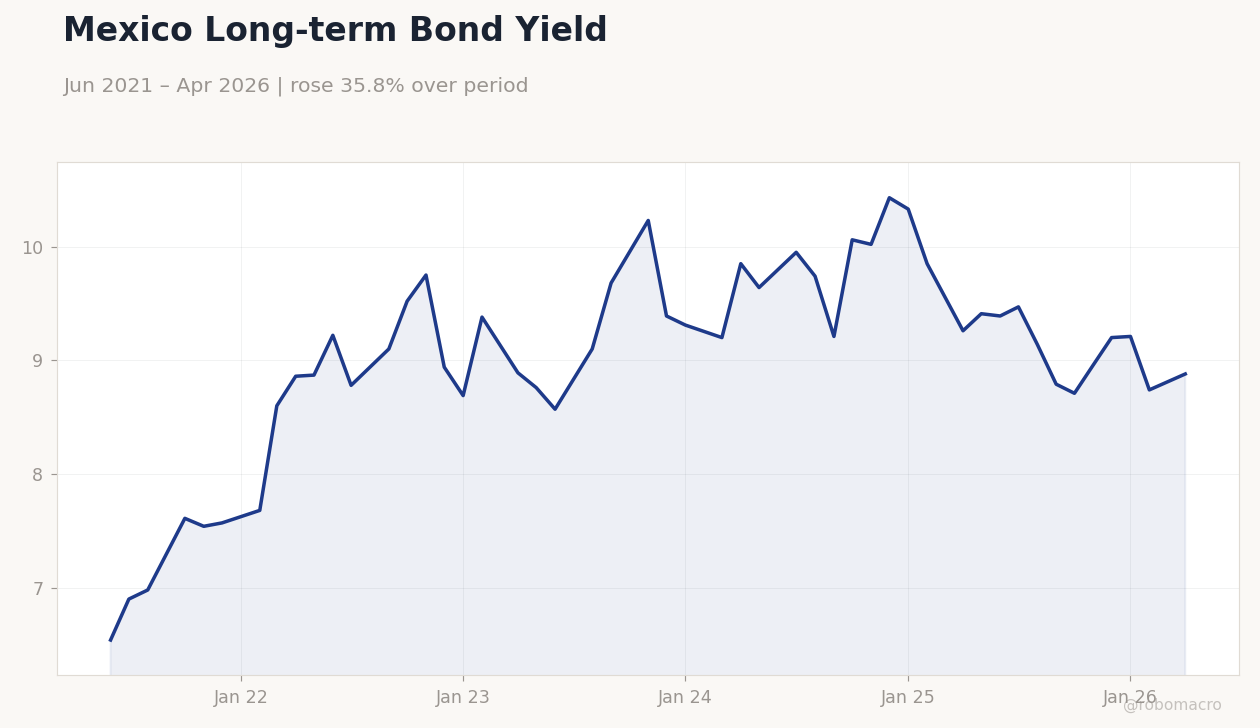

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Bond Yield | Type: macro_line | Yield (%): 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Mexico Long-term Bond Yield | Type: macro_line | Yield (%): 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- IPC Bolsa fell 1.78% to 67,976.50 on thin volume and global risk-off flows.

- USD/MXN rose 0.39% to 17.30 while Mexico short-term rate held at 5.43%.

- Long-term yields climbed to 8.88% as fiscal concerns resurfaced ahead of debt targets.

Yesterday's Recap

Mexican equities closed lower with the IPC Bolsa ending at 67,976.50 after a 1.78% decline driven by profit-taking in nearshoring names. The peso softened as USD/MXN advanced 0.39% to 17.30 amid modest USD strength and light local positioning. Short-term Mexican rates held at 5.43%, reflecting market views on Banxico’s easing path.

Long-term yields rose to 8.88% on renewed focus on fiscal sustainability. WTI Crude tumbled 4.28% to 100.91 while Brent held flat at 109.28. Gold edged up 0.03% to 4,557.30 and silver slipped 0.34%.

No economic data prints were released, leaving price action dominated by external commodity moves and domestic rate signals.

The Day Ahead

The Mexican calendar remains empty today with zero scheduled releases. Market participants will track USMCA-related headlines and any updates on fiscal consolidation plans. Oil price volatility could transmit quickly to the peso given Mexico’s energy exposure.

Global equity sentiment will influence IPC flows, especially in manufacturing and export sectors. Attention stays on incoming foreign portfolio data for signs of sustained bond inflows.

Other Economic Notes

Authorities must contain the fiscal deficit, interest payments and contingent liabilities to safeguard investment-grade status. Nearshoring momentum continues to underpin manufacturing output despite the absence of fresh industrial prints. Remittances remain a steady consumption support even as no new monthly figure appeared yesterday.

Energy reform progress is viewed as having limited near-term effect on Pemex capital spending. Broader EM carry-trade interest is lifting select regional currencies but has yet to materially benefit the peso.

Global Macro News

US equity markets extended gains despite persistent inflation concerns that could delay Fed cuts and keep external financial conditions tighter for Mexico. Brazil’s credit stimulus measures risk anchoring local rates higher, potentially diverting portfolio flows away from Mexican assets. <i>↓ p.2</i>