Mexico Macro Daily(Beta Mode)

Moody’s Cuts Mexico to Baa3 on Fiscal Strain

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,893.93 | +0.49% |

| USD/MXN | 17.36 | -0.24% |

| EUR/MXN | 20.13 | -0.32% |

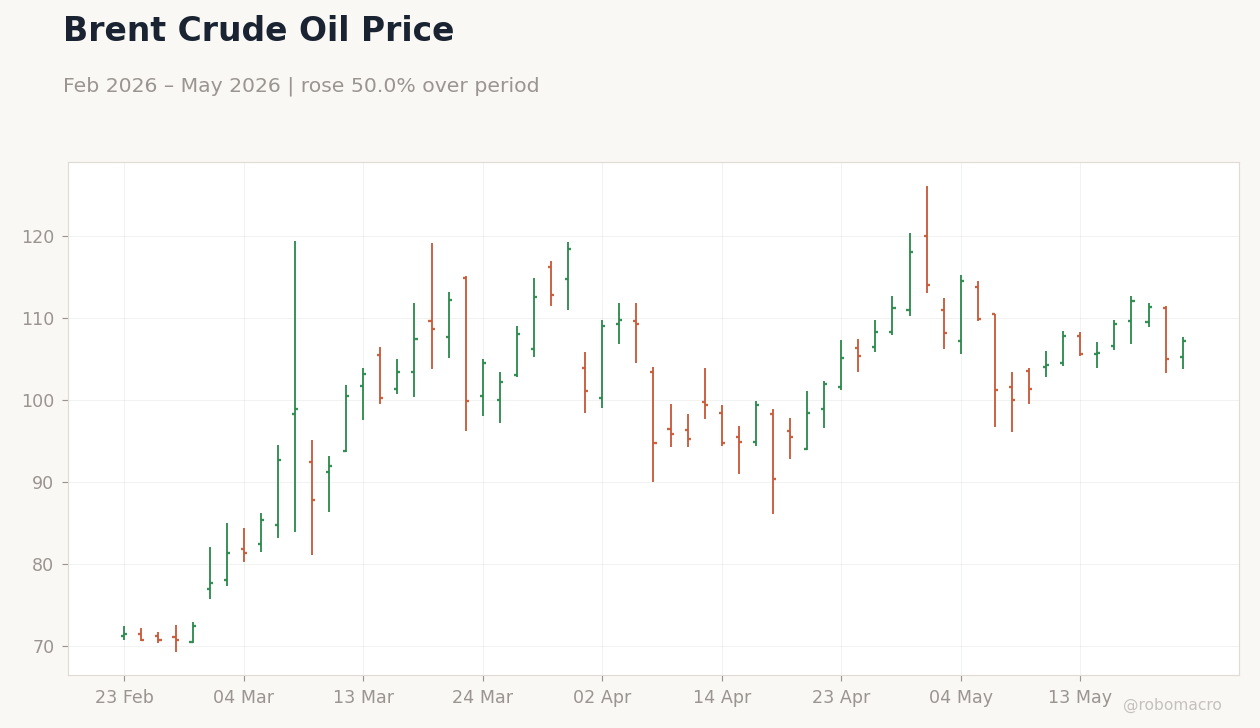

| WTI Crude | 100.79 | +2.57% |

| Silver | 75.22 | -0.83% |

| Gold | 4,511.10 | -0.45% |

| Brent Crude | 106.98 | +1.87% |

| Bitcoin | 77,175.55 | -0.36% |

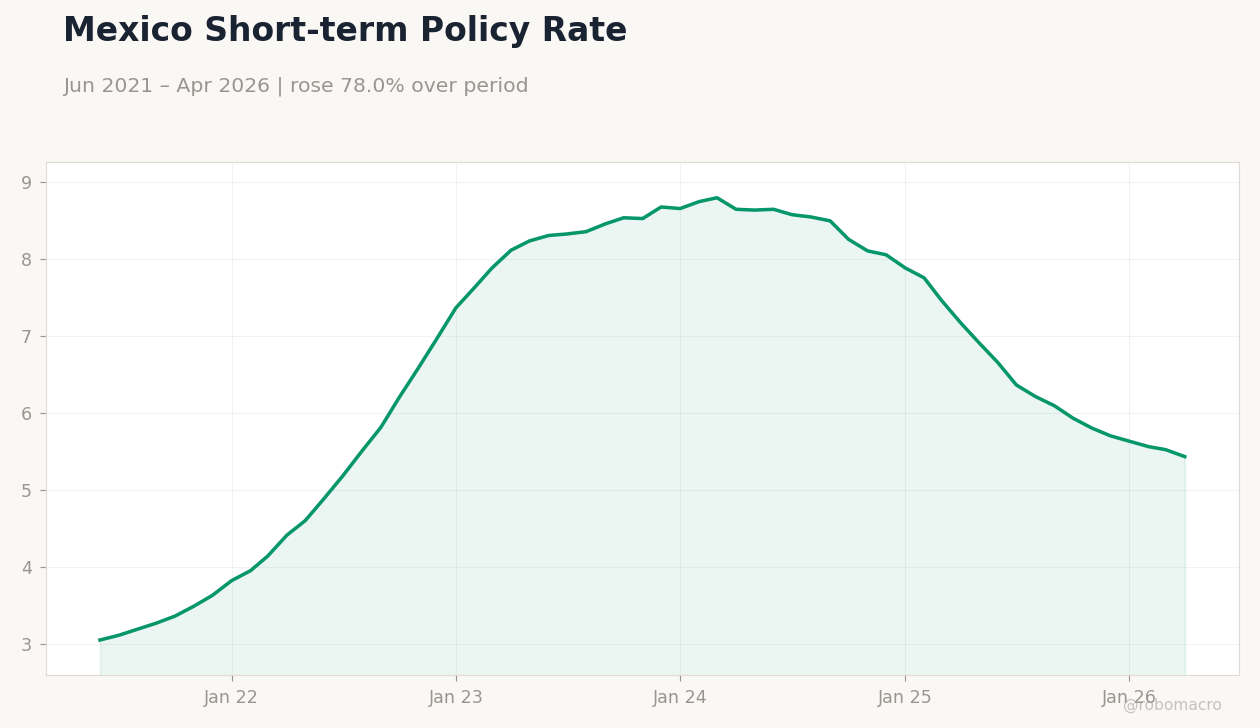

| Mexico Short-term Rate | 5.43% | -1.63% |

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Government Yield | Type: macro_line | Percent: 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Mexico Long-term Government Yield | Type: macro_line | Percent: 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Moody’s downgrades Mexico sovereign rating to Baa3 from Baa2 over persistent fiscal weakness and rigid Pemex support.

- IPC Bolsa advances 0.49% to 68,893.93 while USD/MXN falls 0.24% to 17.36 on peso resilience.

- Mexico short-term rate holds at 5.43% as long-term yields rise 1.60% to 8.88%.

Yesterday's Recap

Markets digested Moody’s downgrade of Mexico’s credit rating to Baa3, citing rigid spending, weak revenues and ongoing Pemex transfers that prevent debt stabilization. The IPC Bolsa still climbed 0.49% to close at 68,893.93, supported by risk-on flows into local equities. USD/MXN eased 0.24% to 17.36 while EUR/MXN dropped 0.32% to 20.13, reflecting peso outperformance.

WTI crude surged 2.57% to 100.79 and Brent rose 1.87% to 106.98, lifting energy-linked names. Mexico’s short-term rate remained at 5.43% after a 1.63% daily decline in the benchmark, while the long-term rate increased 1.60% to 8.88%. No major data releases occurred, leaving the downgrade and commodity moves as the dominant drivers.

The Day Ahead

The calendar stays light with no scheduled releases from INEGI or Banxico. Traders will monitor follow-through from the Moody’s action and any official response on fiscal consolidation. Oil-price strength should continue to support the external accounts and peso.

Attention will also turn to USMCA consultations ahead of the 2026 ministerial meeting, where autos rules-of-origin remain the key friction. Market participants will watch Mbono curve reactions for any repricing of Banxico easing timing.

Other Economic Notes

Nearshoring inflows remain intact despite the rating cut, with new assembly investments still targeting northern states. Remittances continue to provide a steady current-account buffer. Energy-reform delays have slowed private renewables capex, keeping reliance on Pemex support and widening fiscal rigidities.

US-Mexico trade relations stay constructive overall, though autos-origin disputes could surface again before year-end.

Global Macro News

Elevated oil prices offer Mexico a terms-of-trade tailwind that partially offsets rating concerns. Global central banks outside Mexico are tightening or holding to combat inflation spillovers from geopolitical energy shocks. Stronger commodity revenues should help narrow Mexico’s fiscal gap in the near term.

<i>↓ p.2</i>