Mexico Macro Daily(Beta Mode)

Moody's Downgrade Weighs on Mexican Assets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,384.41 | -0.74% |

| USD/MXN | 17.30 | -0.02% |

| EUR/MXN | 20.08 | -0.23% |

| WTI Crude | 96.48 | +0.13% |

| Silver | 76.16 | -0.33% |

| Gold | 4,521.50 | -0.40% |

| Brent Crude | 103.35 | +0.75% |

| Bitcoin | 77,380.48 | -0.20% |

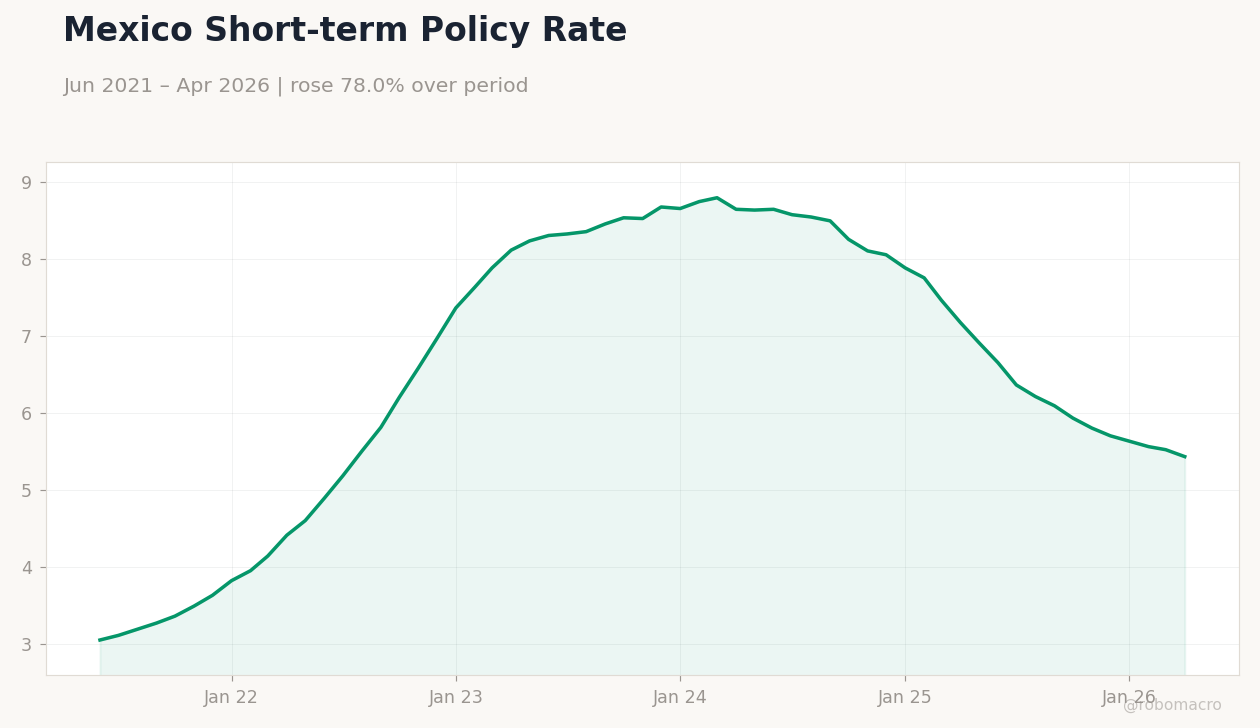

| Mexico Short-term Rate | 5.43% | -1.63% |

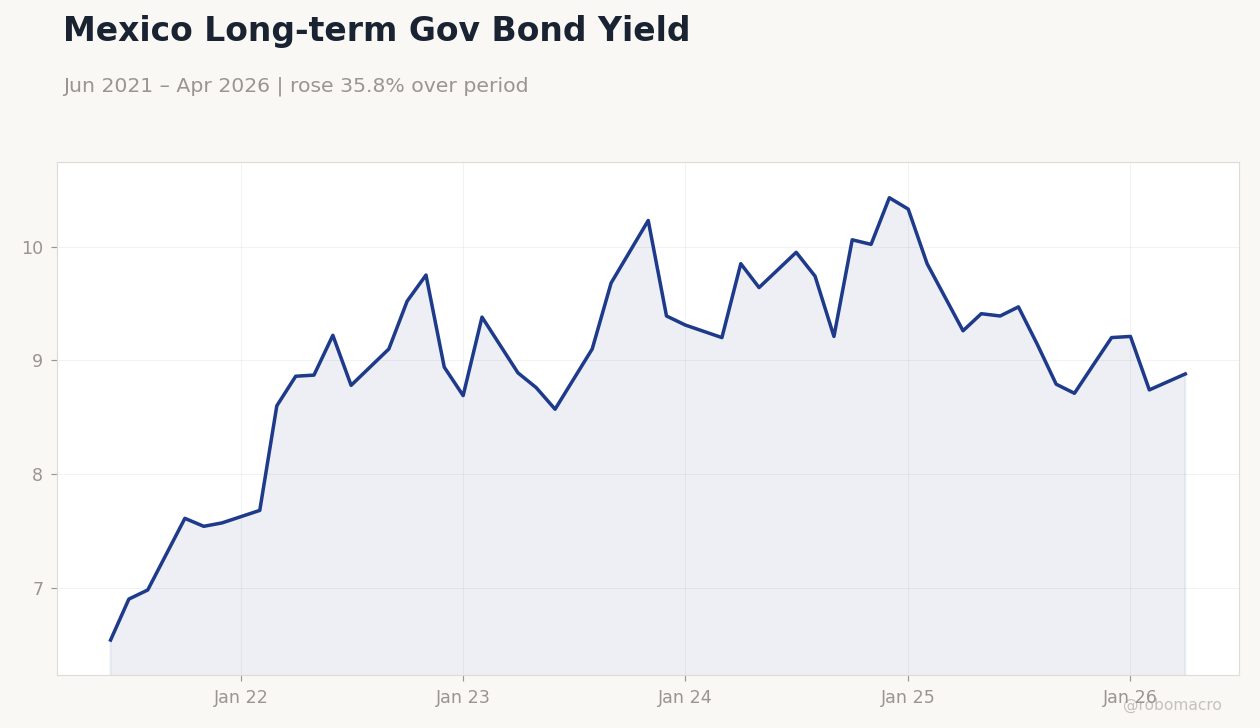

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Long-term Gov Bond Yield | Type: macro_line | %: 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Mexico Long-term Gov Bond Yield | Type: macro_line | %: 8.88 (2026-04-01) | Range: 6.54–10.43 | Trend(5pt): 6.54,9.1,9.39,9.85,8.88

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Moody's downgrades Mexico's credit rating on rigid spending, low revenues and Pemex support needs

- Mid-May inflation slowed in line with forecasts after Banxico's final easing move

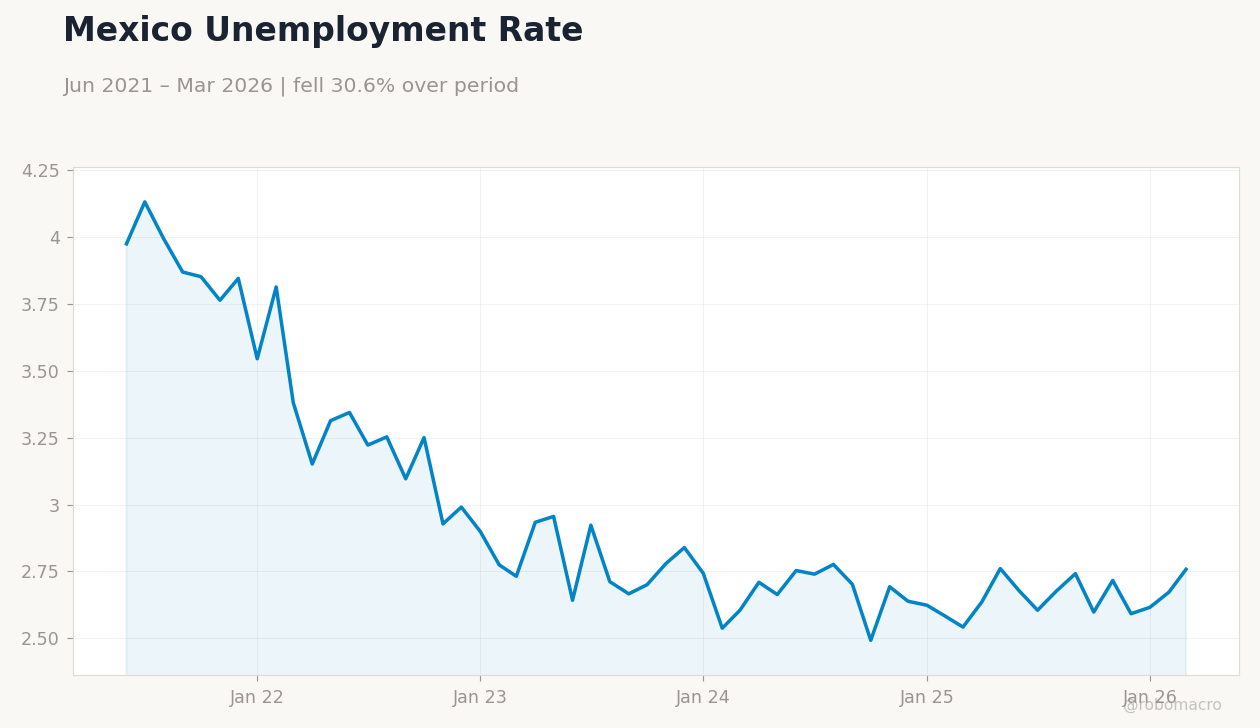

- Q1 GDP contraction proved milder than expected despite manufacturing and services weakness

Yesterday's Recap

Mexico's IPC Bolsa fell 0.74 percent to 68,384.41 as investors digested Moody's downgrade of the sovereign credit rating. USD/MXN held steady near 17.30 while the short-term rate eased to 5.43 percent. Mid-May inflation data confirmed a slowdown after Banxico delivered its last rate cut last month.

The economy shrank less than anticipated in the first quarter, with agriculture and manufacturing weighing on activity. Long-term yields rose 1.60 percent to 8.88 percent amid fiscal concerns. Brent crude gained 0.75 percent to 103.35, offering limited support to the peso.

Market participants focused on the rating agency's warning that debt containment remains elusive.

The Day Ahead

Attention turns to market digestion of the Moody's action and any follow-up fiscal commentary from officials. Traders will monitor USMCA-related developments and nearshoring announcements for peso direction. Oil price stability could limit downside in USD/MXN after yesterday's flat close.

Equity flows may remain cautious until clearer signals emerge on debt dynamics. Broader risk sentiment tied to global trade tensions will influence IPC Bolsa performance. No major domestic data prints are scheduled, keeping focus on external drivers and Banxico communications.

Other Economic Notes

Fiscal rigidity and continued Pemex support continue to pressure Mexico's debt trajectory according to Moody's assessment. Nearshoring inflows persist in key sectors such as automotive, yet overall growth momentum stays subdued. Remittances provide steady external support while energy-reform legislation remains stalled.

The combination of softer inflation and a shallower Q1 contraction offers limited relief to policymakers facing rating pressure. Markets price a narrow path for any further policy adjustment given these cross-currents.