Mexico Macro Daily(Beta Mode)

Peso Rises as Mexico Trade Surplus Narrows

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,589.52 | +0.37% |

| USD/MXN | 17.26 | -0.19% |

| EUR/MXN | 20.09 | +0.00% |

| WTI Crude | 96.60 | +0.00% |

| Silver | 76.20 | +0.40% |

| Gold | 4,523.20 | +0.05% |

| Brent Crude | 100.21 | -3.22% |

| Bitcoin | 77,257.53 | +0.36% |

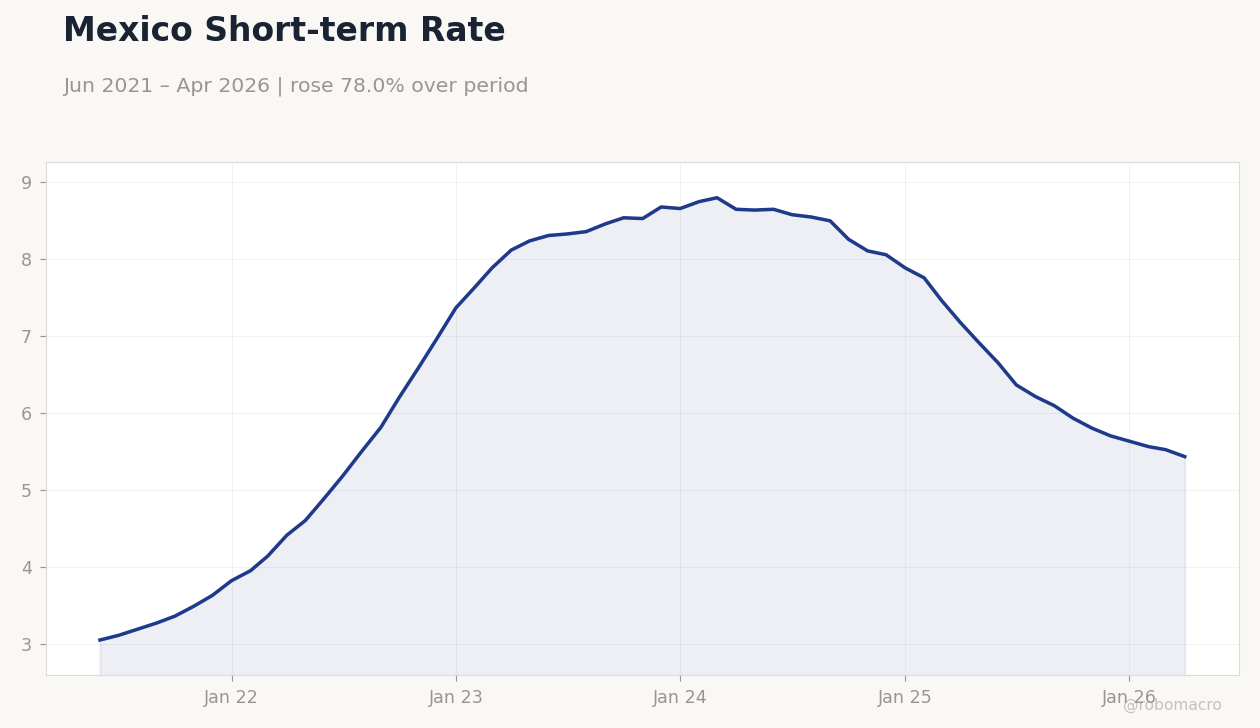

| Mexico Short-term Rate | 5.43% | -1.63% |

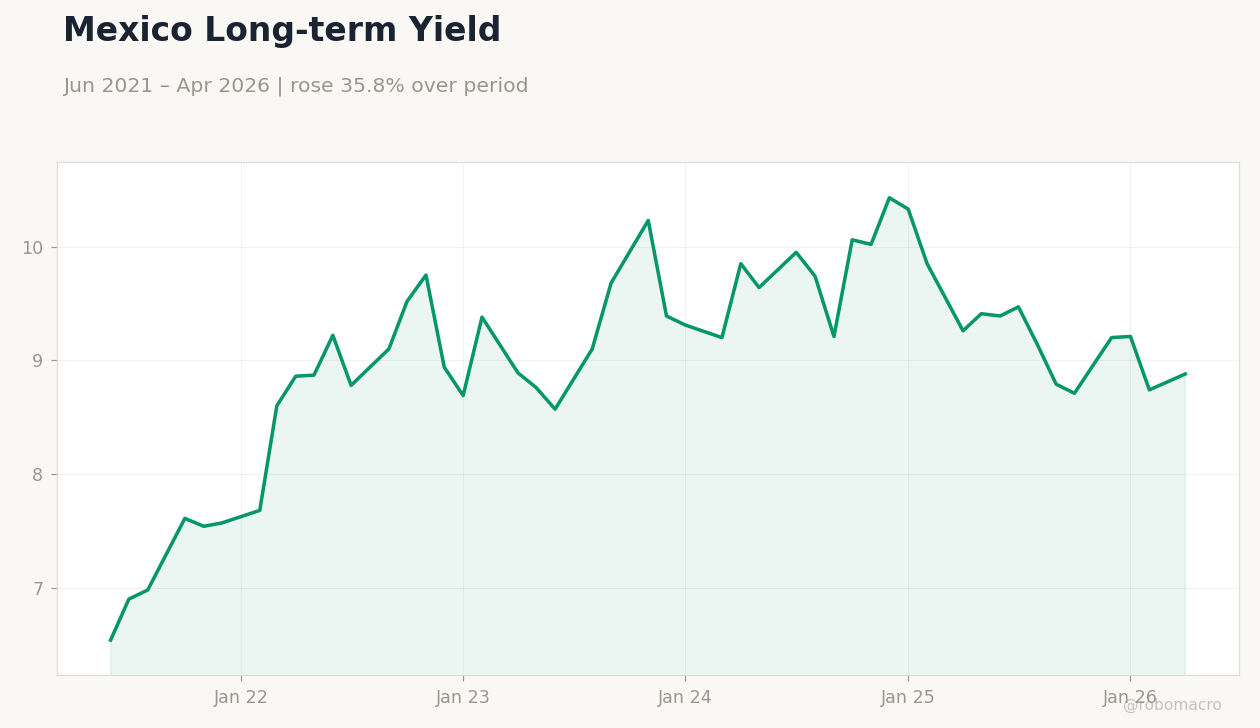

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

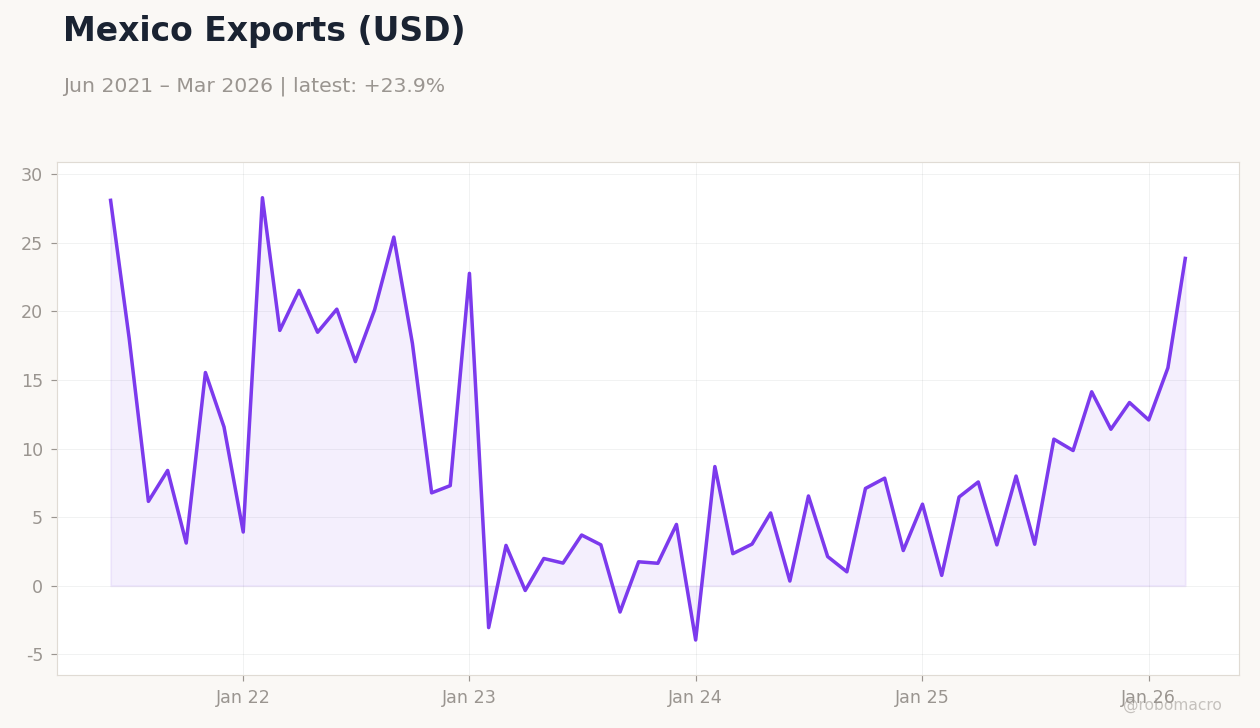

| Trade Balance | 5,932m | - | 4,520m |

Mexico Short-term Rate | Type: macro_line | Short-term Rate (%): 5.43 (2026-04-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.43

Mexico Short-term Rate | Type: macro_line | Short-term Rate (%): 5.43 (2026-04-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexico's April trade surplus narrowed to 4.52 billion USD from 5.93 billion USD prior, reflecting softer export momentum.

- IPC Bolsa rose 0.37 percent to 68,589.52 while USD/MXN fell 0.19 percent to 17.26 on peso buying.

- Short-term Mexican rates held at 5.43 percent while long-term yields climbed to 8.88 percent.

Yesterday's Recap

Mexico reported a narrower trade surplus of 4.52 billion USD for April, down from the prior 5.93 billion USD reading. The IPC Bolsa advanced 0.37 percent to close at 68,589.52 amid selective buying in nearshoring-exposed names. USD/MXN declined 0.19 percent to 17.26, extending the peso's recent firmness against the dollar.

EUR/MXN held steady at 20.09 while WTI crude remained unchanged at 96.60. Mexico's short-term rate stood at 5.43 percent and the long-term rate rose 1.60 percent to 8.88 percent. Brent crude dropped 3.22 percent to 100.21.

Bitcoin gained 0.36 percent to 77,257.53 with limited spillover to local assets. Silver rose 0.40 percent and gold edged up 0.05 percent.

The Day Ahead

No major Mexican data releases are scheduled for today or tomorrow according to the calendar. Markets will monitor USMCA-related trade flows and any Banxico member commentary. Participants may focus on peso positioning ahead of month-end flows.

Equity desks will track IPC sector rotation tied to manufacturing data from the United States. Volatility in long-term yields could influence duration positioning in local bonds.

Other Economic Notes

Nearshoring continues to support manufacturing investment despite the softer trade print. USMCA compliance remains central to export competitiveness with North American partners. Silver and gold prices posted modest gains, offering limited support to mining equities within the IPC.

High long-term yields signal caution on fiscal sustainability and inflation expectations. Broader regional growth concerns from Brazil may indirectly weigh on sentiment toward Mexican assets.

Global Macro News

China introduced new export controls on chemical precursors destined for the United States, Mexico and Canada, signaling tighter coordination on fentanyl-related trade. Iran's World Cup training base relocation to Mexico received FIFA approval and could generate modest tourism-related inflows. <i>↓ p.2</i>