Mexico Macro Daily(Beta Mode)

Mexico Trade Surplus Tops Forecasts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 69,197.57 | +1.37% |

| USD/MXN | 17.31 | +0.11% |

| EUR/MXN | 20.14 | +0.11% |

| WTI Crude | 90.63 | -3.47% |

| Silver | 74.24 | -2.71% |

| Gold | 4,467.00 | -0.74% |

| Brent Crude | 94.20 | -5.40% |

| Bitcoin | 75,636.55 | -0.25% |

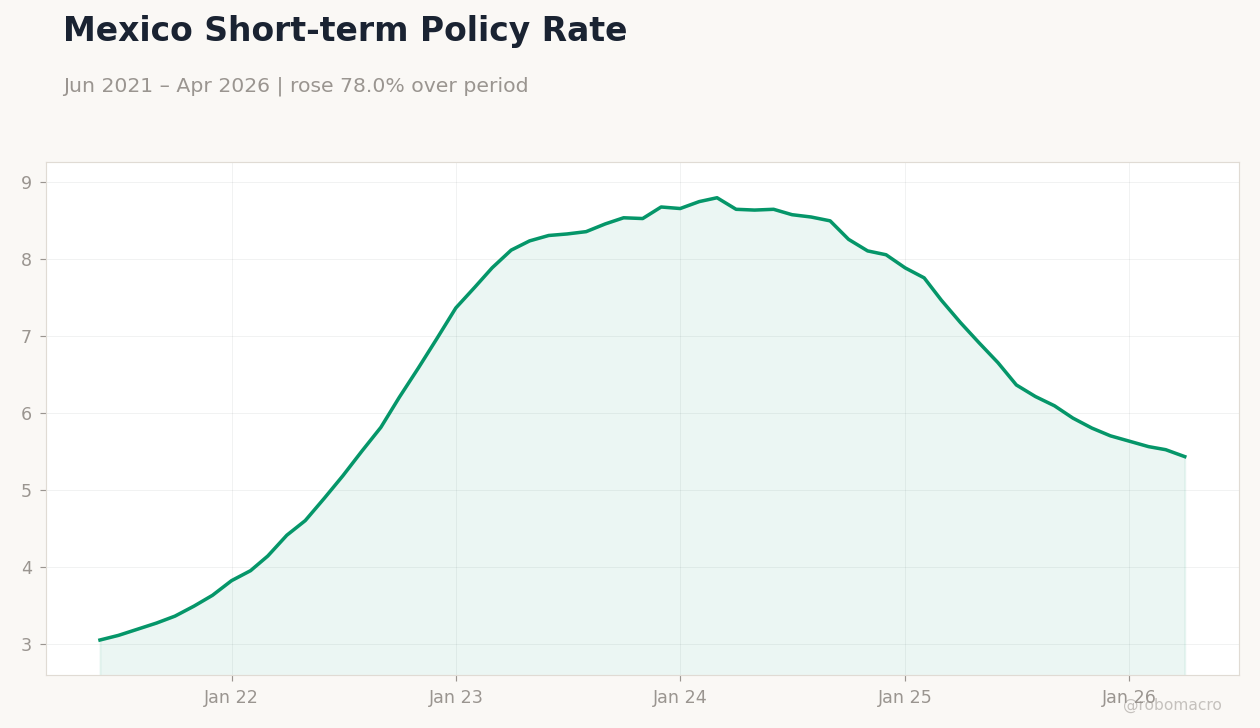

| Mexico Short-term Rate | 5.43% | -1.63% |

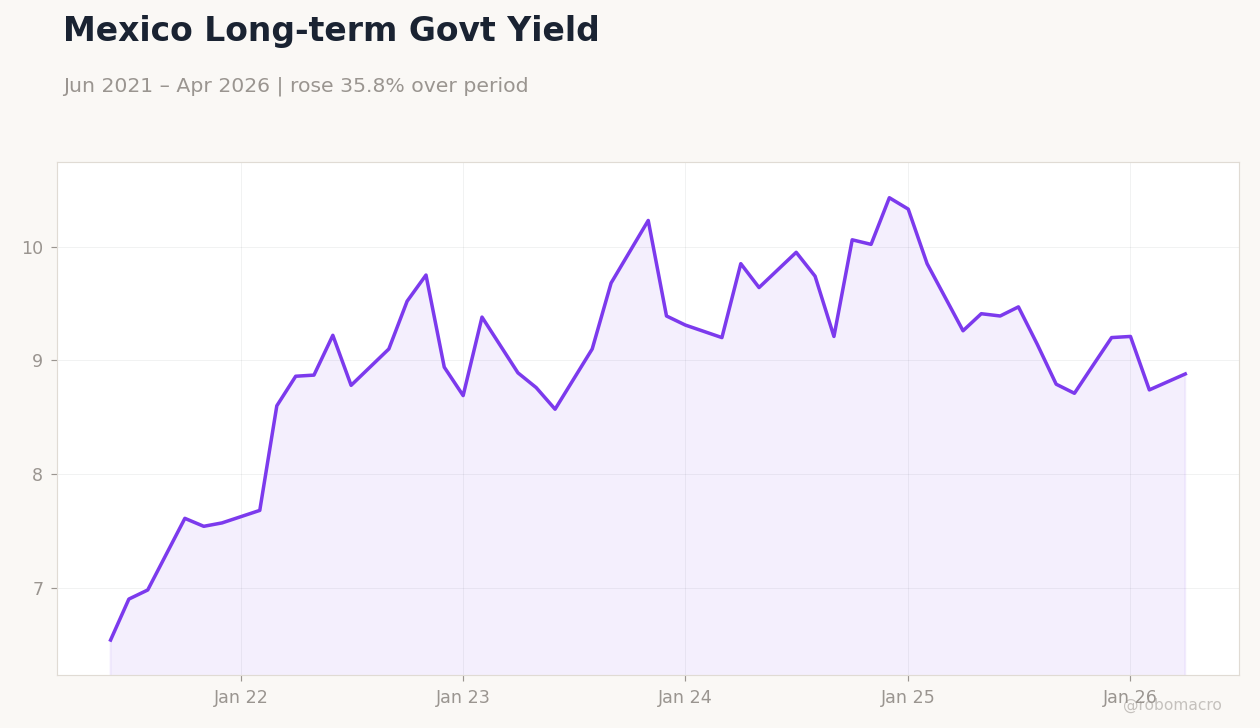

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 5,932m | 1,410m | 4,520m |

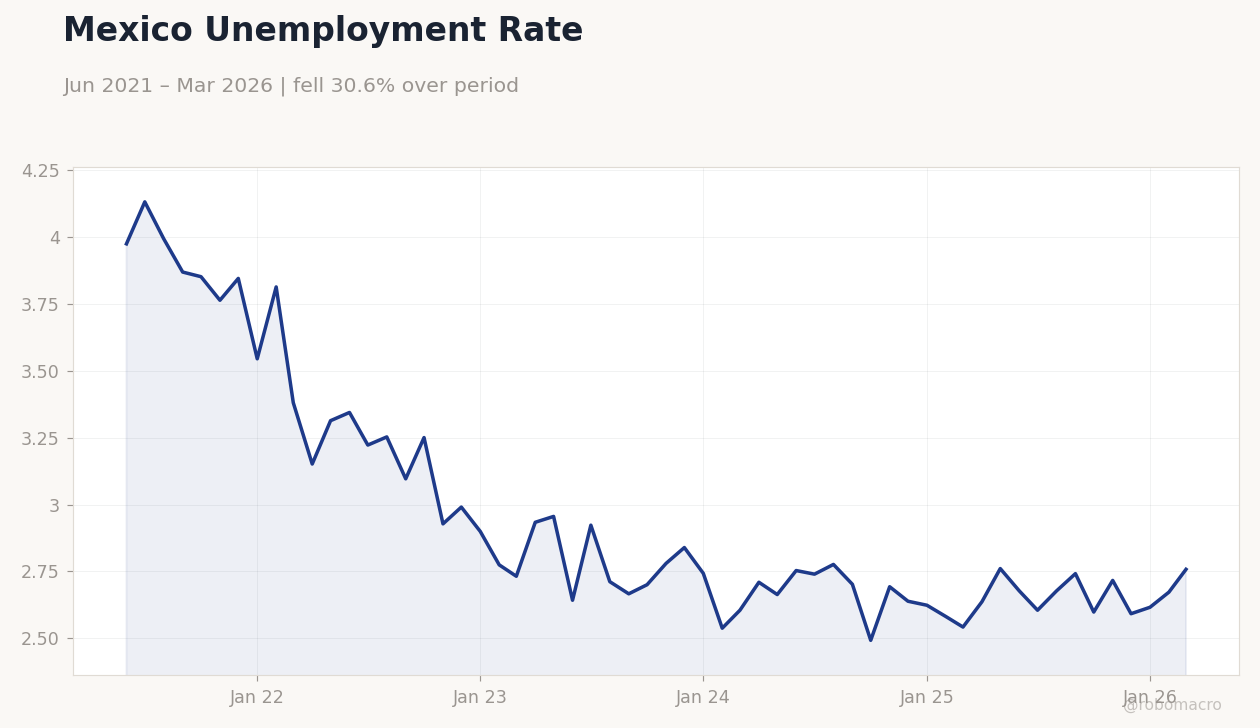

Mexico Unemployment Rate | Type: macro_line | %: 2.758 (2026-03-01) | Range: 2.493–4.129 | Trend(6pt): 3.973,3.252,2.701,2.639,2.673,2.758

Mexico Unemployment Rate | Type: macro_line | %: 2.758 (2026-03-01) | Range: 2.493–4.129 | Trend(6pt): 3.973,3.252,2.701,2.639,2.673,2.758

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

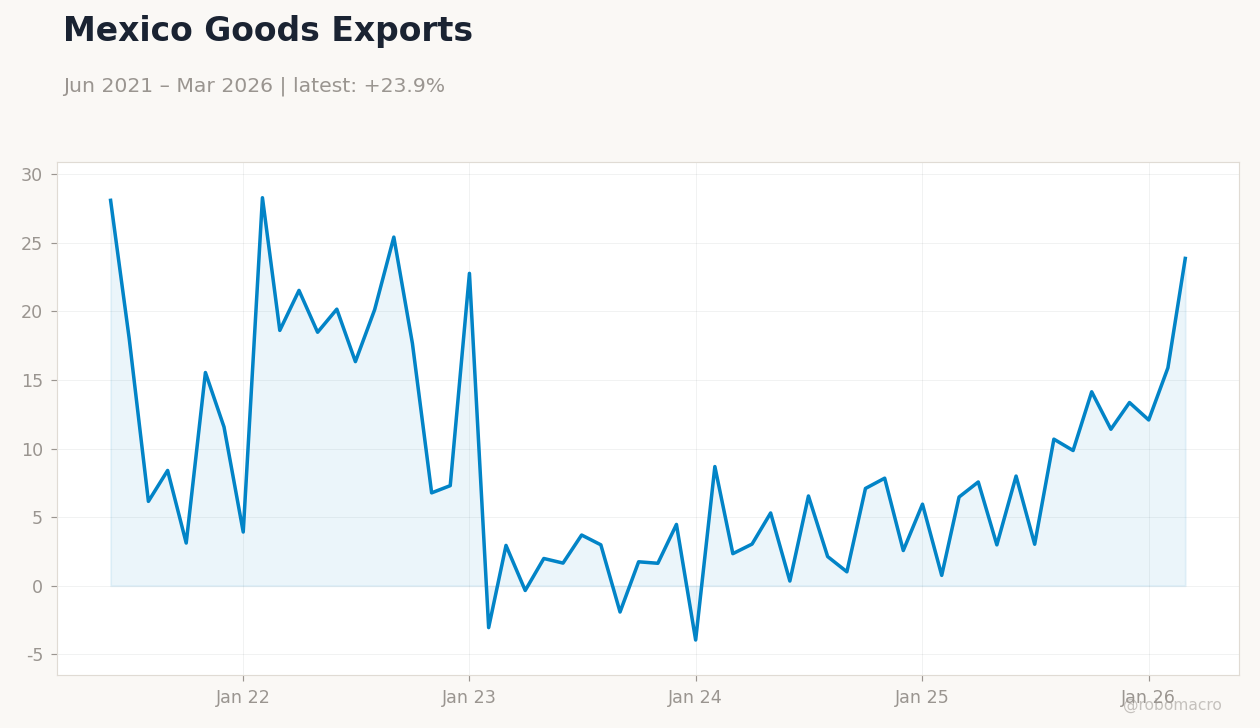

- Mexico April trade balance printed a $4.52 billion surplus, well above the $1.41 billion consensus.

- IPC Bolsa rose 1.37% to 69,197.57 while USD/MXN edged 0.11% higher to 17.31.

- Mexico short-term rate fell to 5.43% as long-term yields increased 1.60% to 8.88%.

Yesterday's Recap

Mexico posted a $4.52 billion trade surplus in April that beat the $1.41 billion consensus though fell short of the prior $5.93 billion reading. The outturn reflected resilient exports tied to nearshoring despite faster import growth. IPC Bolsa advanced 1.37% to close at 69,197.57, supported by industrial names.

USD/MXN finished at 17.31 after a 0.11% gain, while EUR/MXN rose the same amount to 20.14. WTI crude fell 3.47% to $90.63 per barrel and Brent dropped 5.40%, weighing on sentiment. Mexico’s short-term rate declined 1.63% to 5.43% whereas the long-term rate rose 1.60% to 8.88%.

No Banxico speakers appeared and markets absorbed the data without shifting policy expectations.

The Day Ahead

No Mexican data releases are scheduled for today or tomorrow. Attention will stay on USMCA tariff developments and any fresh comments from US officials on trade enforcement. Nearshoring-related investment flows remain the dominant theme for equities and the peso.

Market participants will monitor global risk appetite given sharp moves in oil and metals. Any diplomatic updates on regional hosting arrangements could influence short-term sentiment. Positioning ahead of next week’s potential US data prints may keep volumes light.

Other Economic Notes

President Sheinbaum’s stance on USMCA compliance continues to ease immediate tariff concerns for auto exporters. Remittances and rising industrial electricity demand underscore steady consumption and nearshoring momentum. Environmental remediation issues surrounding the 2014 Sonora spill keep pressure on copper producers.

Export composition risks shifting toward lower-value goods if US tariff policy persists. These factors collectively support a cautious but constructive view on Mexican growth.

Global Macro News

US officials signaled tariffs on USMCA partners will remain in place, keeping trade relations in focus for Mexico. ECB council member Schnabel advocated a June hike even if Middle East tensions ease, supporting higher global yields. <i>↓ p.2</i>