Mexico Macro Daily(Beta Mode)

Mexico Trade Surplus Beats Forecasts

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 70,021.35 | +1.19% |

| USD/MXN | 17.39 | +0.55% |

| EUR/MXN | 20.20 | +0.40% |

| WTI Crude | 91.43 | +3.10% |

| Silver | 73.07 | -2.06% |

| Gold | 4,412.90 | -0.78% |

| Brent Crude | 95.05 | +0.81% |

| Bitcoin | 73,381.88 | -1.30% |

| Mexico Short-term Rate | 5.43% | -1.63% |

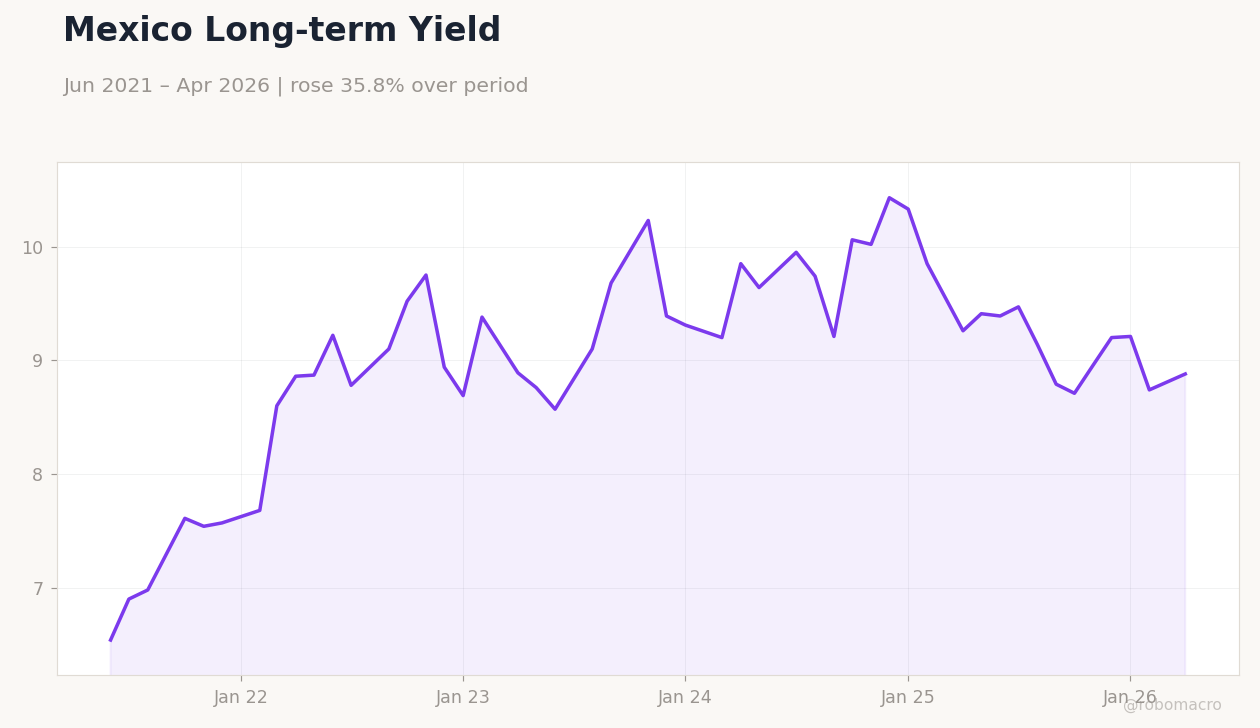

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 5,932m | 1,410m | 4,520m |

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate %: 5.43 (2026-04-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.43

Mexico Short-term Policy Rate | Type: macro_line | Short-term Rate %: 5.43 (2026-04-01) | Range: 3.05–8.79 | Trend(6pt): 3.05,5.5,8.53,8.05,5.56,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

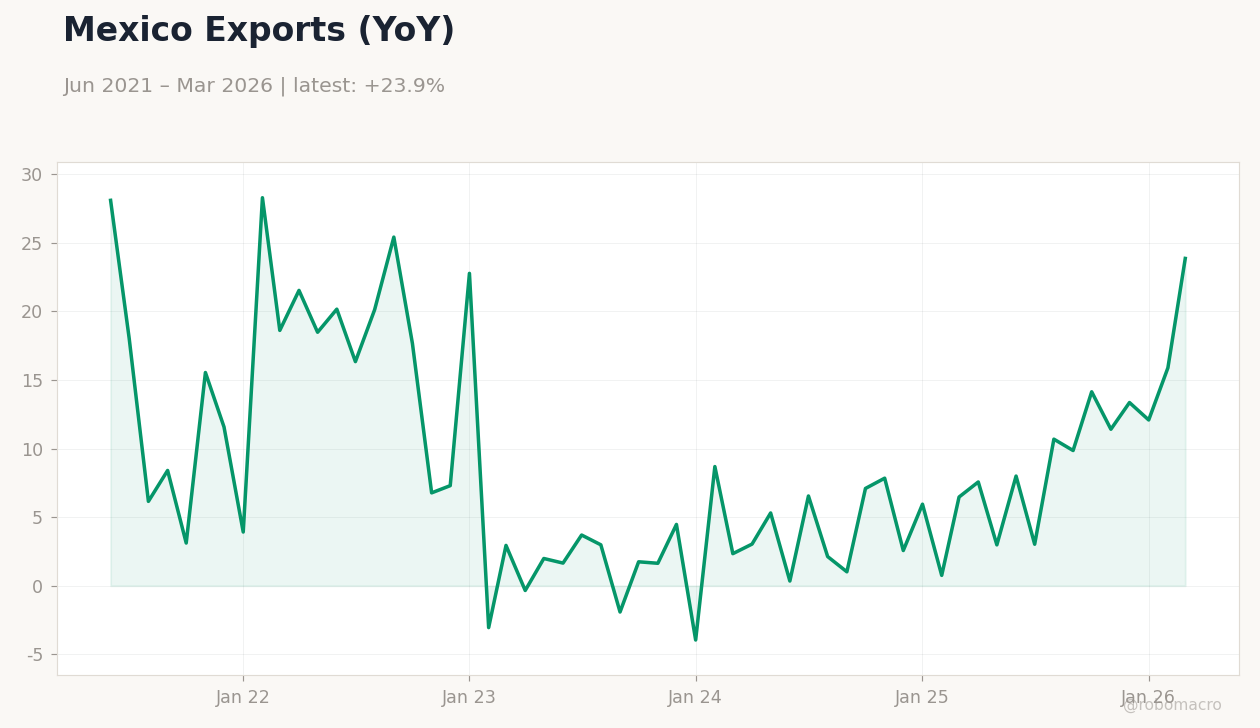

- Mexico posted a $4.52 bn trade surplus in April, far exceeding the $1.41 bn consensus and signaling resilient export momentum.

- IPC Bolsa climbed 1.19% to 70,021.35 while USD/MXN rose 0.55% to 17.39 amid mixed rate moves.

- Short-term Mexican rates fell to 5.43% as markets priced steady Banxico policy amid strong external demand.

Yesterday's Recap

Mexico’s April trade balance delivered a $4.52 bn surplus, well above the $1.41 bn consensus and reversing the prior month’s $5.93 bn print. The outturn reflected firm manufacturing exports to the United States under nearshoring flows. IPC Bolsa advanced 1.19% to close at 70,021.35, led by auto and electronics names.

USD/MXN rose 0.55% to 17.39 while EUR/MXN gained 0.40% to 20.20. WTI crude jumped 3.10% to $91.43, supporting the energy-linked peso complex. Mexico’s short-term rate eased 1.63% to 5.43% while the long-term rate rose 1.60% to 8.88%.

Market reaction stayed orderly with limited volatility in the peso.

The Day Ahead

No major Mexican data releases are scheduled for 28 May. Traders will monitor USMCA-related statements from Washington for any tariff signals. Oil price moves will continue to influence MXN sentiment given elevated WTI levels.

Regional equity flows may support IPC Bolsa if US equity futures hold gains. Banxico officials are not expected to speak, leaving markets focused on incoming US trade rhetoric.

Other Economic Notes

Record Mexican exports to the United States highlight an ongoing shift toward North American supply chains despite looming USMCA talks. Informality continues to sustain cash usage, limiting fintech penetration and tax revenue gains. GM’s planned localization of China-built models from 2027 could add further nearshoring investment in the auto sector.

US bilateral tariff discussions with Mexico, while excluding Canada, introduce fresh uncertainty for 2026 growth forecasts.

Global Macro News

Trump administration signals to retain tariffs on Mexican and Canadian goods are stirring USMCA renegotiation risks. Petrobras and Pemex are advancing Gulf of Mexico exploration talks that could lift Mexican energy output. Argentina’s peso liberalization and rising reserves offer a regional contrast to Mexico’s tighter external accounts.

<i>↓ p.2</i>