Mexico Macro Daily(Beta Mode)

Business Confidence Dips as Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 68,587.74 | -0.40% |

| USD/MXN | 17.31 | -0.44% |

| EUR/MXN | 20.17 | -0.11% |

| WTI Crude | 89.79 | +2.78% |

| Silver | 76.04 | +0.57% |

| Gold | 4,530.40 | -0.66% |

| Brent Crude | 93.15 | +1.20% |

| Bitcoin | 71,907.61 | -2.27% |

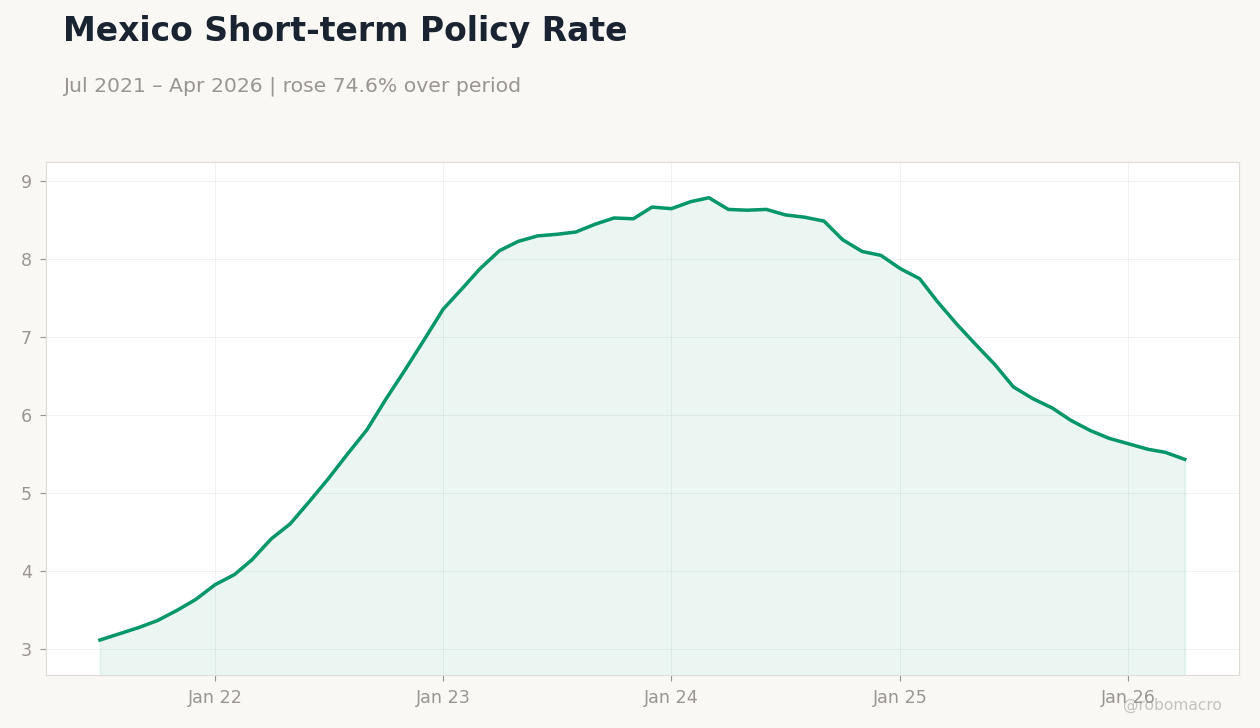

| Mexico Short-term Rate | 5.43% | -1.63% |

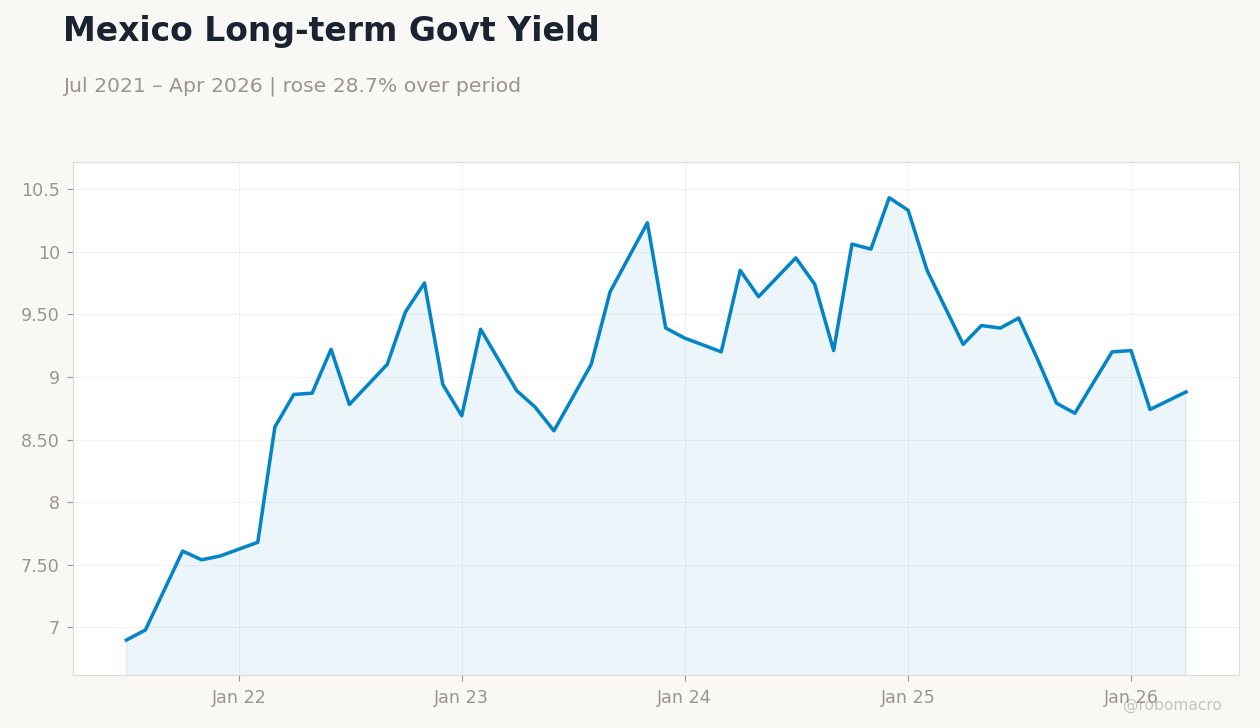

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business Confidence Index | 47.90 | - | 47.50 |

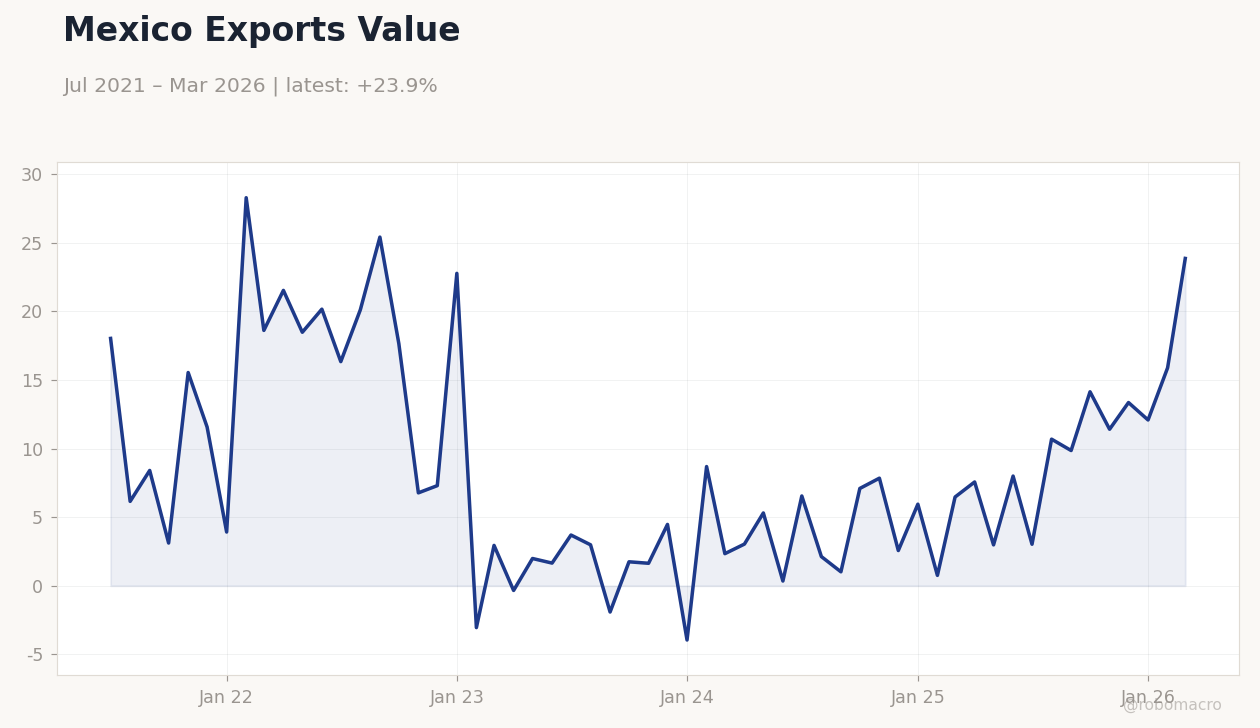

Mexico Exports Value | Type: macro_line | USD mn: 23.86 (2026-03-01) | Range: -3.957–28.28 | Trend(5pt): 18.03,25.41,1.637,5.944,23.86

Mexico Exports Value | Type: macro_line | USD mn: 23.86 (2026-03-01) | Range: -3.957–28.28 | Trend(5pt): 18.03,25.41,1.637,5.944,23.86

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-05) | |||

| Consumer Confidence Index | 44.40 | - | 04:00 |

- Mexico's Business Confidence Index declined to 47.5 in May from 47.9 prior, signaling softer sentiment.

- USD/MXN fell 0.44% to 17.31 while IPC Bolsa dropped 0.40% to 68,587.74 amid mixed commodity moves.

- Mexico short-term rate held at 5.43% with long-term yields rising 1.60% to 8.88%.

Yesterday's Recap

Mexico's Business Confidence Index printed at 47.5 for May, down from 47.9 in the prior month and reflecting weaker corporate optimism. The peso advanced as USD/MXN closed at 17.31 after a 0.44% decline, outperforming regional peers on steady remittances and contained inflation prints. IPC Bolsa ended 0.40% lower at 68,587.74, with losses concentrated in financials while nearshoring-linked industrials held steadier.

The short-term policy rate remained at 5.43% while the long-term yield climbed to 8.88%. WTI crude rose 2.78% to 89.79, providing some support to energy-exposed names. No Banxico speakers appeared and markets absorbed the data without volatility spikes.

EUR/MXN eased 0.11% to 20.17, extending the peso's broad-based gains.

The Day Ahead

Attention turns to the Consumer Confidence Index release scheduled for June 5 at 04:00 ET. Markets will assess whether the 44.4 prior reading deteriorates further amid fiscal tightening signals. No Mexican data prints are listed for June 1-2, leaving room for USMCA-related headlines to influence flows.

Traders will monitor any updates on the autumn Russia-Mexico business forum discussing non-dollar trade mechanisms. Positioning ahead of the print favors limited MXN volatility given the absence of Banxico commentary.

Other Economic Notes

Companies face heightened compliance costs as fiscal scrutiny intensifies, elevating operational risk for firms reliant on government permits. Record tourism inflows continue to bolster services activity and peso receipts despite softer business sentiment. Nearshoring remains the dominant structural driver, yet unresolved USMCA automotive rules-of-origin issues cap upside for manufacturing exports.

PEMEX fiscal protections under the 2025 energy framework have reduced near-term sovereign risk premia.