Mexico Macro Daily(Beta Mode)

Peso Weakens Ahead of Inflation Print

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 65,944.64 | -0.30% |

| USD/MXN | 17.44 | +0.96% |

| EUR/MXN | 20.12 | +0.29% |

| WTI Crude | 91.65 | +1.23% |

| Silver | 68.58 | -0.53% |

| Gold | 4,354.20 | +0.39% |

| Brent Crude | 94.59 | +1.61% |

| Bitcoin | 63,821.00 | +0.92% |

| Mexico Short-term Rate | 5.43% | -1.63% |

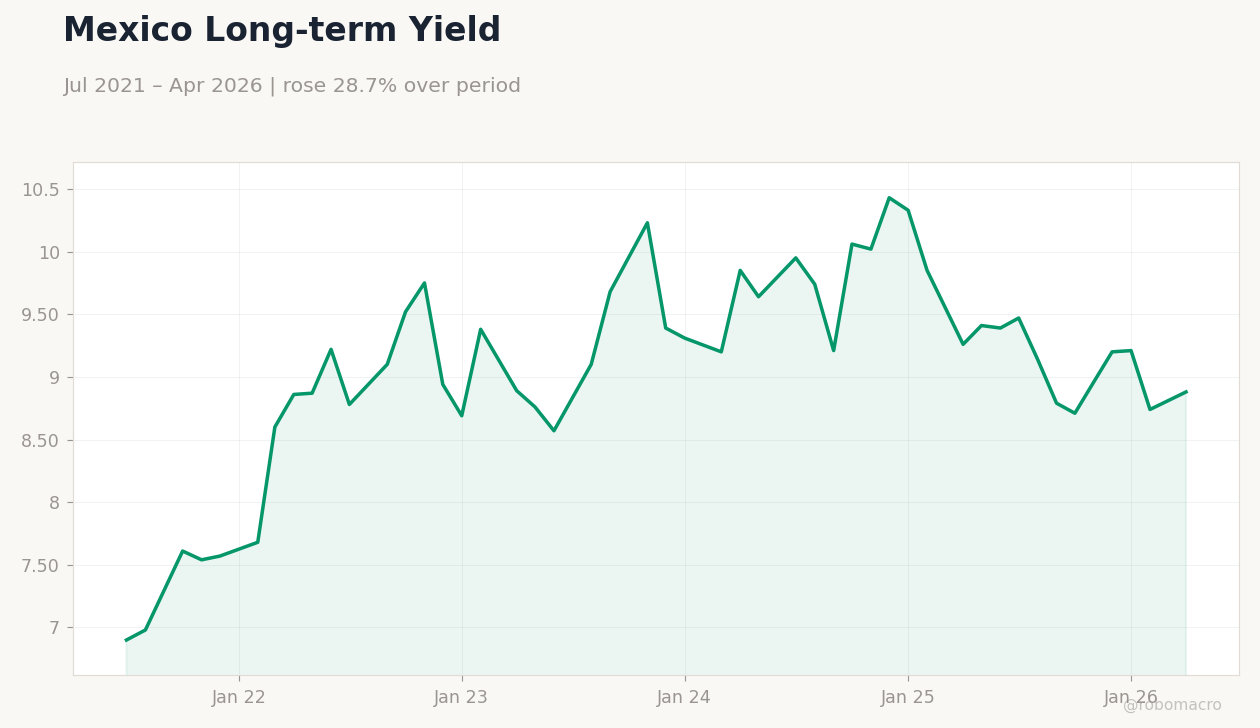

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Mexico Policy Rate vs CPI | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Mexico Policy Rate vs CPI | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-09) | |||

| Inflation Rate Month-over-Month | 0.20 | - | 04:00 |

| Inflation Rate Year-over-Year | 4.45 | - | 04:00 |

- USD/MXN rose 0.96% to 17.44 as markets priced limited near-term Banxico easing.

- IPC Bolsa fell 0.30% to 65,944.64 amid softer growth revisions and USMCA delays.

- Mexico short-term rate held at 5.43% while long-term yields climbed 1.60% to 8.88%.

Yesterday's Recap

Mexican markets closed mixed on June 7 with no domestic data releases. The peso depreciated sharply as USD/MXN climbed nearly 1% to 17.44, reflecting broader USD strength and delayed USMCA renewal talks. IPC Bolsa declined 0.30% to 65,944.64 as investors digested downward growth revisions for Mexico and the US.

Oil prices advanced, with WTI up 1.23% to 91.65 and Brent rising 1.61% to 94.59, supporting energy-linked revenues. Mexico’s short-term rate remained at 5.43% while the long-term rate increased to 8.88%. News of potential months-long haggling over auto rules and Chinese content added to trade uncertainty.

Remittances and nearshoring flows continued to underpin the current account despite the softer equity tone.

The Day Ahead

Mexico will release May inflation data at 04:00 ET on June 9. The MoM rate is expected to follow the prior 0.2% print while the YoY measure stands at 4.45%. These figures will shape expectations for Banxico’s next moves given the 5.43% policy rate.

No central bank speakers or minutes are scheduled. Markets will also monitor any updates on USMCA consultations and pension fund inflows reported by US asset managers. Industrial production and export data may follow later in the week.

Other Economic Notes

Growth forecasts for Mexico were revised lower due to rising protectionism and policy uncertainty. Nearshoring remains a bright spot with new auto-component investments announced in northern states. Remittances hit record levels, supporting consumption even as fiscal discipline limits sovereign spread widening.

US demands for stricter car-parts rules could extend trade negotiations beyond the July USMCA milestone. Pension fund allocations to private credit are drawing interest from major US managers seeking exposure to the $500 billion Afore system.

Global Macro News

USMCA partners are set to miss the July renewal deadline, increasing tariff risks for autos and manufacturing supply chains. <i>↓ p.2</i>