Mexico Macro Daily(Beta Mode)

Mexico CPI Undershoots, Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 65,698.10 | -0.67% |

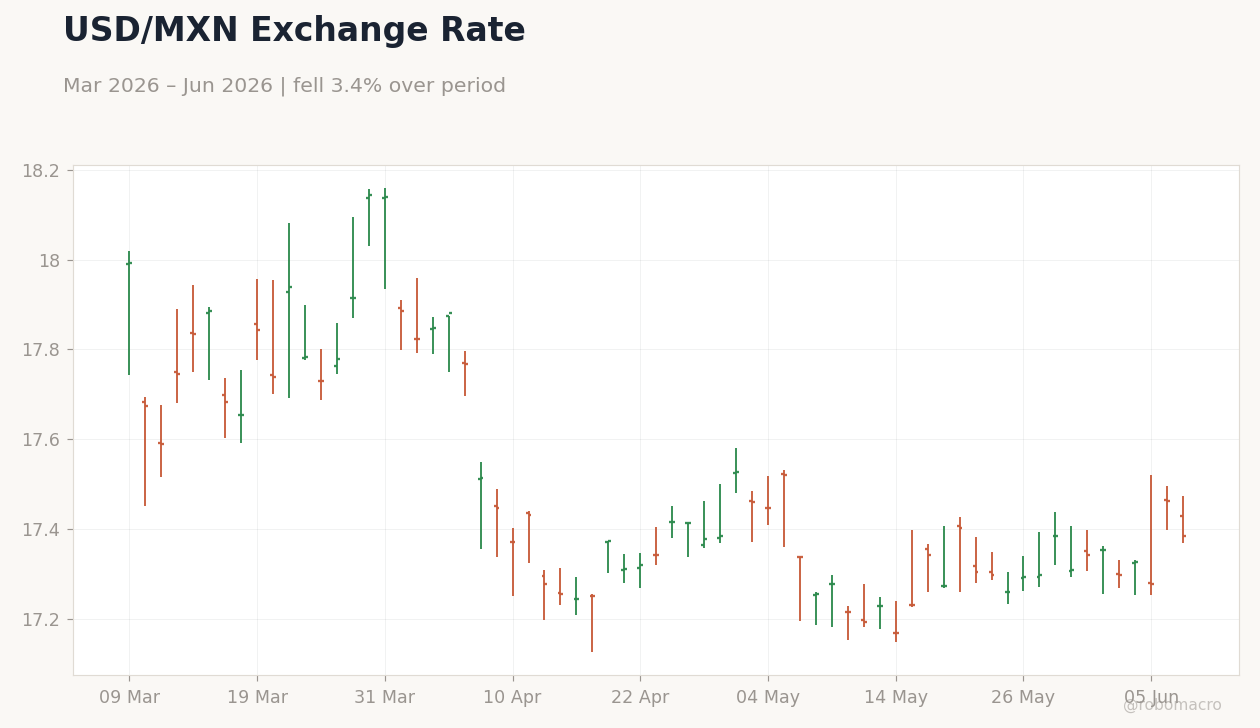

| USD/MXN | 17.38 | -0.48% |

| EUR/MXN | 20.12 | -0.01% |

| WTI Crude | 89.31 | -2.18% |

| Silver | 68.88 | +0.66% |

| Gold | 4,367.10 | +0.72% |

| Brent Crude | 92.68 | -1.67% |

| Bitcoin | 62,497.62 | -0.94% |

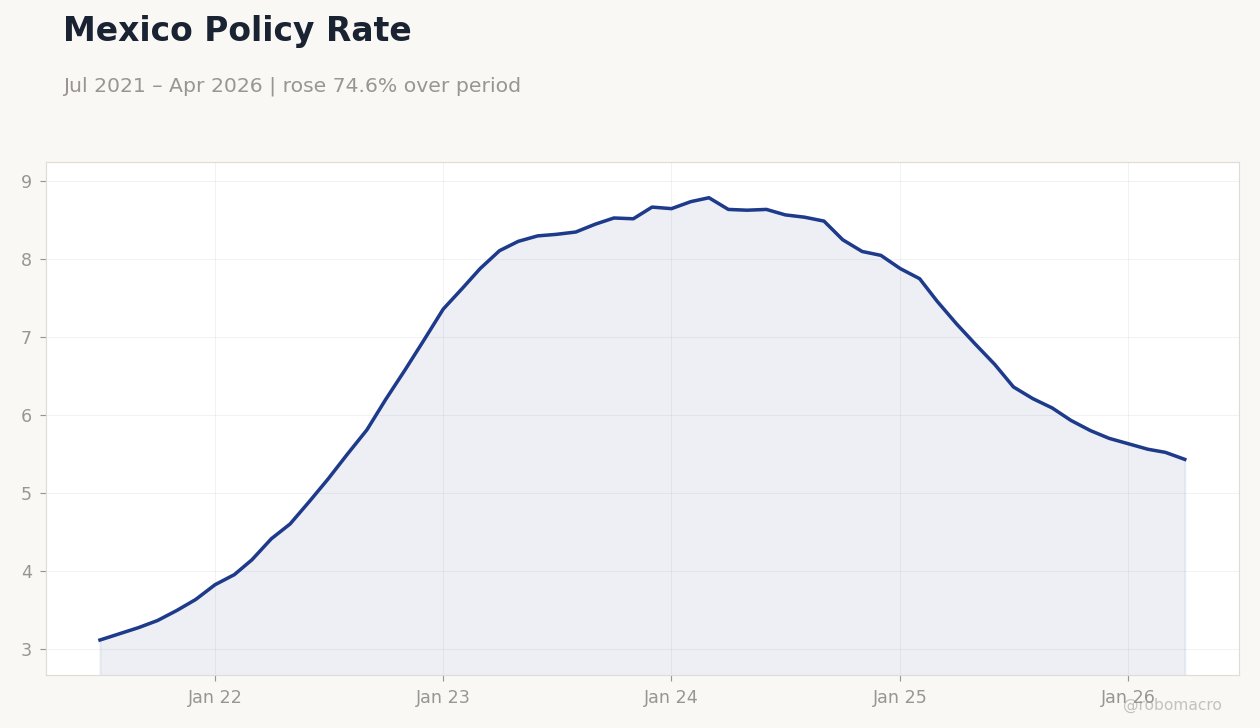

| Mexico Short-term Rate | 5.43% | -1.63% |

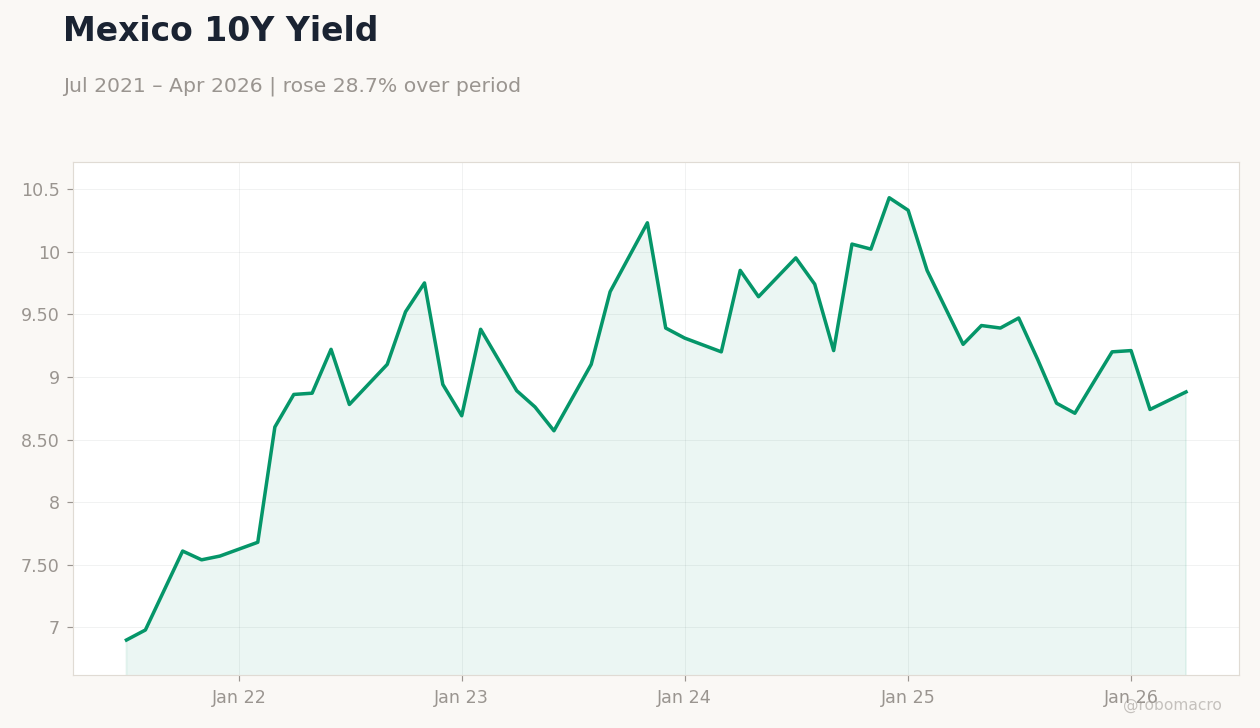

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.20 | -0.12 | -0.21 |

| Inflation Rate Year-over-Year | 4.45 | 4.03 | 3.94 |

Mexico Policy Rate | Type: macro_line | Short-term Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Mexico Policy Rate | Type: macro_line | Short-term Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- May inflation slowed more than expected to 3.94% y/y and -0.21% m/m, returning inside Banxico’s target range.

- IPC Bolsa fell 0.67% to 65,698.10 while USD/MXN declined 0.48% to 17.38 on softer price data.

- Mexico short-term rate held at 5.43% as markets adjusted cut expectations lower.

Yesterday's Recap

Mexico’s May inflation print surprised to the downside, with the year-over-year rate falling to 3.94% against a 4.03% consensus and the month-over-month rate printing -0.21% versus -0.12% expected. The softer outcome placed headline inflation back inside Banxico’s 2-4% target band. The peso reacted positively, driving USD/MXN to 17.38 and EUR/MXN to 20.12.

Equity markets moved lower, with the IPC Bolsa closing at 65,698.10, down 0.67%. Short-term Mexican rates held at 5.43% while the long-term rate rose to 8.88%. WTI crude fell 2.18% to 89.31, adding modest downside pressure to the energy-linked peso.

No Banxico speakers appeared.

The Day Ahead

No economic releases are scheduled for Mexico on June 9 or June 10. Attention will remain on secondary indicators such as industrial production and trade balance due later in the week. Market participants will monitor any follow-up commentary from Banxico board members for signals on the timing of future easing.

USMCA-related trade flows and nearshoring investment announcements may also influence sentiment. The absence of data leaves room for external drivers, particularly US yields and oil prices, to dominate peso trading.

Other Economic Notes

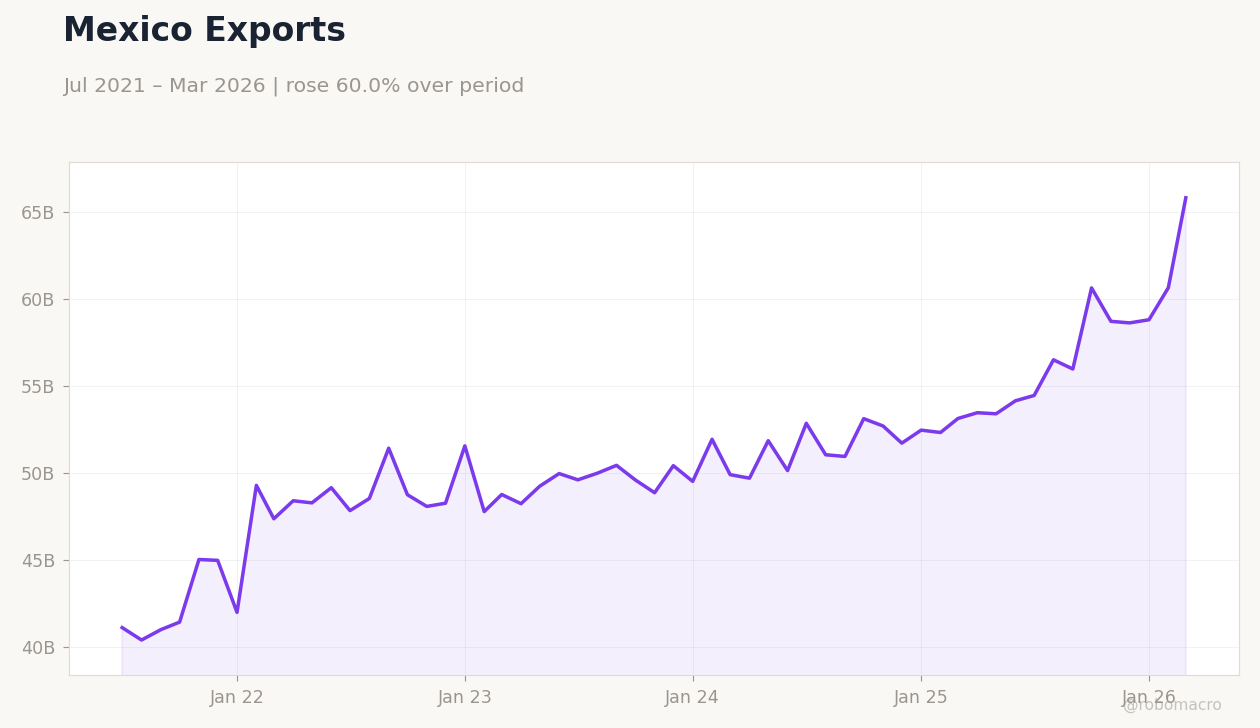

Downward revisions to Mexican and US growth forecasts highlight risks from rising protectionism and policy uncertainty. Blue Owl, Ares and Golub Capital are actively courting Mexico’s $500 billion pension fund sector for private-credit allocations. SOCAP cooperatives continue to demonstrate stronger grassroots trust than fintech platforms, underscoring persistent gaps in formal financial inclusion.

Nearshoring inflows remain a key growth support even as overall GDP projections have been trimmed.

Global Macro News

Ottawa’s “Fortress North America” trade proposal seeks to protect USMCA preferences amid renewed bilateral talks with Washington. US-China tariff tensions continue to weigh on global supply chains that feed Mexican manufacturing. <i>↓ p.2</i>