Mexico Macro Daily(Beta Mode)

Mexico CPI Undershoots, Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 65,616.85 | +0.32% |

| USD/MXN | 17.38 | -0.51% |

| EUR/MXN | 20.07 | -0.28% |

| WTI Crude | 89.99 | +2.03% |

| Silver | 64.95 | -0.22% |

| Gold | 4,163.40 | -2.27% |

| Brent Crude | 92.83 | +1.51% |

| Bitcoin | 62,135.00 | +0.80% |

| Mexico Short-term Rate | 5.43% | -1.63% |

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.20 | -0.12 | -0.21 |

| Inflation Rate Year-over-Year | 4.45 | 4.03 | 3.94 |

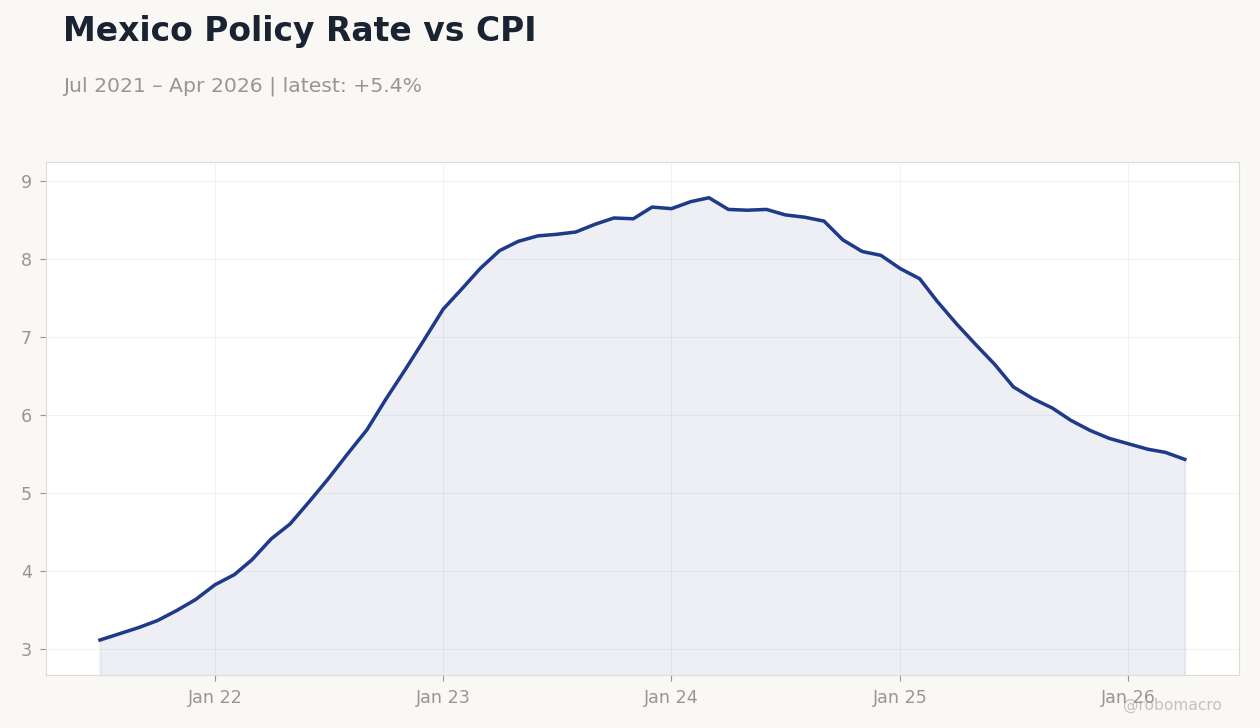

Mexico Policy Rate vs CPI | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Mexico Policy Rate vs CPI | Type: macro_line | Policy Rate %: 5.43 (2026-04-01) | Range: 3.11–8.79 | Trend(6pt): 3.11,5.81,8.52,7.88,5.52,5.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- May inflation cooled to 3.94% y/y, below consensus and inside Banxico’s target band

- USD/MXN fell 0.51% to 17.38 as softer data reinforced easing expectations

- IPC Bolsa rose 0.32% while short-term rates eased 1.63% to 5.43%

Yesterday's Recap

Mexico’s May inflation rate fell 0.21% month-over-month against a -0.12% consensus, while the annual rate printed 3.94% versus 4.03% expected. The downside surprise returned headline inflation to Banxico’s 2-4% target range. USD/MXN declined 0.51% to close at 17.38, with EUR/MXN also easing 0.28%.

The IPC Bolsa advanced 0.32% to 65,616.85, supported by peso strength and selective equity inflows. Mexico’s short-term rate dropped 1.63% to 5.43% while the long-term rate rose 1.60% to 8.88%. WTI crude gained 2.03% to 89.99, providing modest support to the energy-linked peso.

Markets interpreted the print as validation for further policy easing later this year.

The Day Ahead

The Mexican calendar is empty today and tomorrow, leaving markets to digest yesterday’s inflation release. Attention will shift to next week’s industrial production and retail sales prints for growth signals. Banxico’s June minutes, due next week, will provide the next direct read on policymakers’ reaction function.

Traders will monitor USMCA-related headlines for any impact on nearshoring flows. Peso volatility is expected to remain contained absent fresh data or external shocks.

Other Economic Notes

Remittances continue to underpin the current account and provide a buffer for the peso. Progress on energy-sector reforms that permit greater private participation in transmission is viewed as mildly supportive for nearshoring investment. USMCA labor consultations on auto wages remain active but have not produced new market-moving developments.

Financial-inclusion efforts via SOCAP cooperatives highlight structural gaps that fintechs have yet to close at scale.

Global Macro News

North American rig counts rose again, supporting regional energy prices that indirectly aid Mexico’s fiscal accounts. US-China trade tensions persist, keeping supply-chain diversification themes alive for Mexican manufacturers. The Bank of Canada held rates steady, reinforcing a cautious global easing cycle that Mexico is tracking.

<i>↓ p.2</i>