Mexico Macro Daily(Beta Mode)

Inflation Undershoots, Peso Strengthens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| IPC Bolsa | 64,962.02 | +0.22% |

| USD/MXN | 17.39 | -0.38% |

| EUR/MXN | 20.05 | -0.40% |

| WTI Crude | 89.75 | -0.31% |

| Silver | 63.65 | -1.48% |

| Gold | 4,092.20 | -0.39% |

| Brent Crude | 92.72 | -0.41% |

| Bitcoin | 62,985.99 | +2.50% |

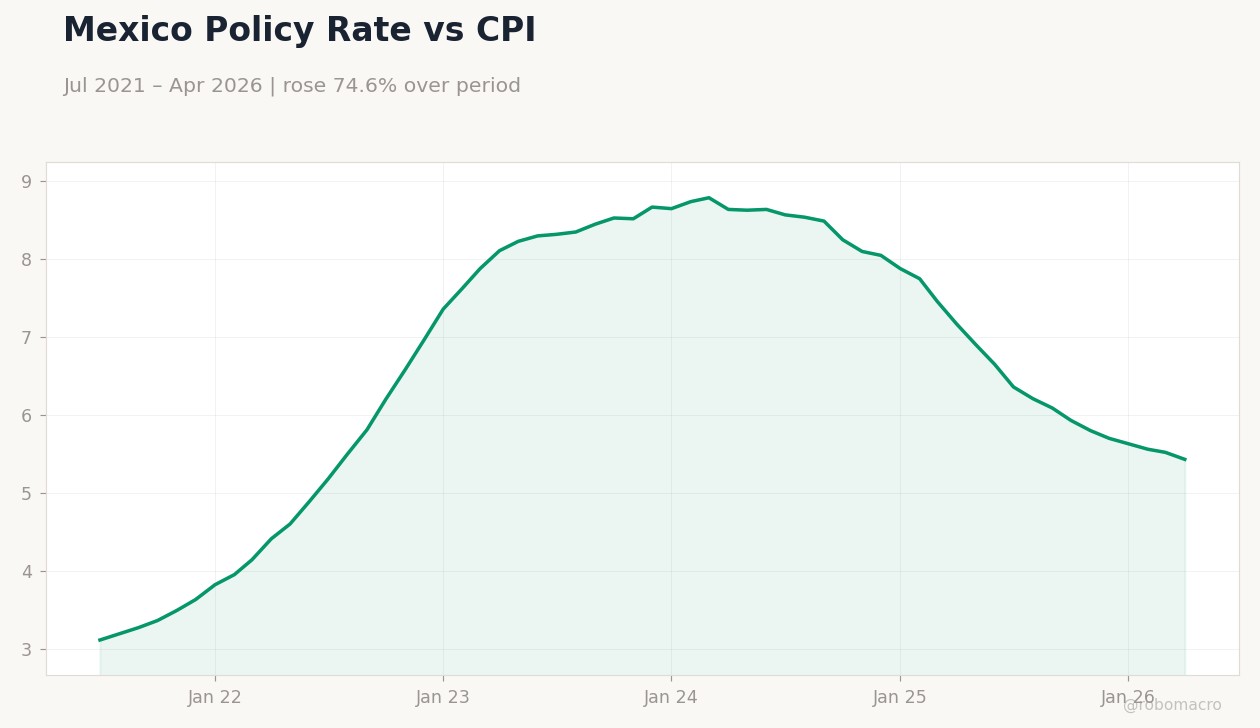

| Mexico Short-term Rate | 5.43% | -1.63% |

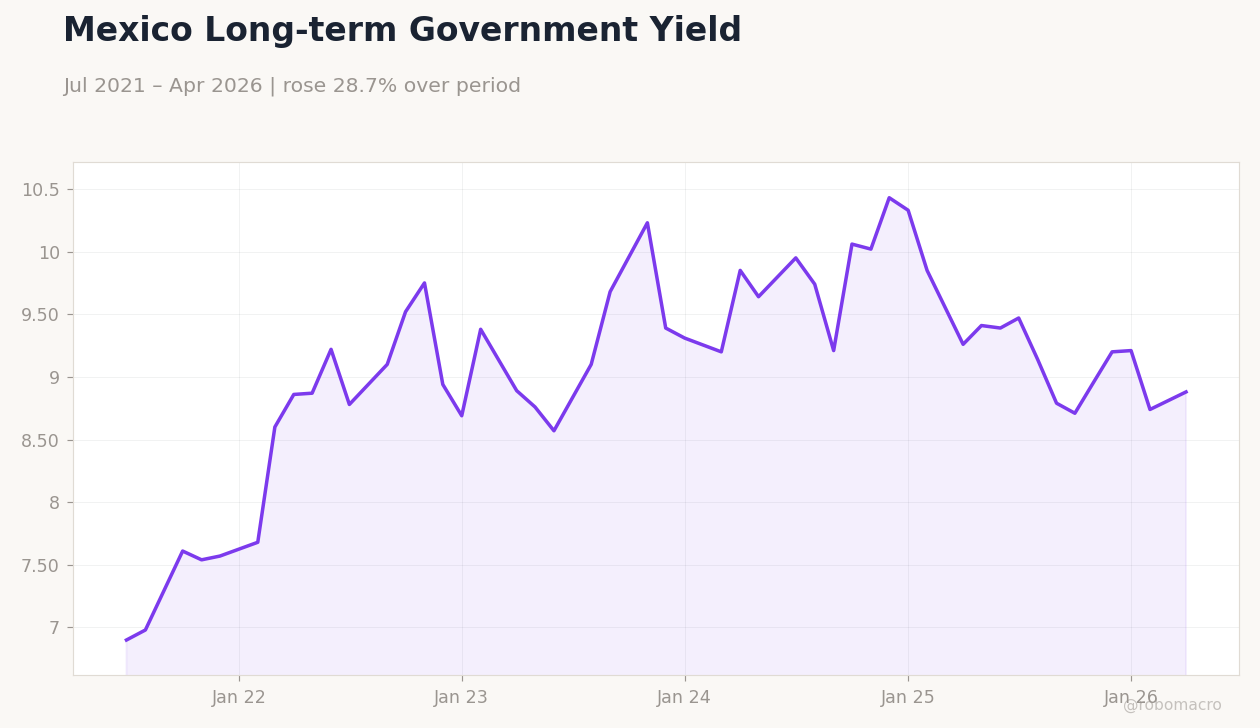

| Mexico Long-term Rate | 8.88% | +1.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.20 | -0.12 | -0.21 |

| Inflation Rate Year-over-Year | 4.45 | 4.03 | 3.94 |

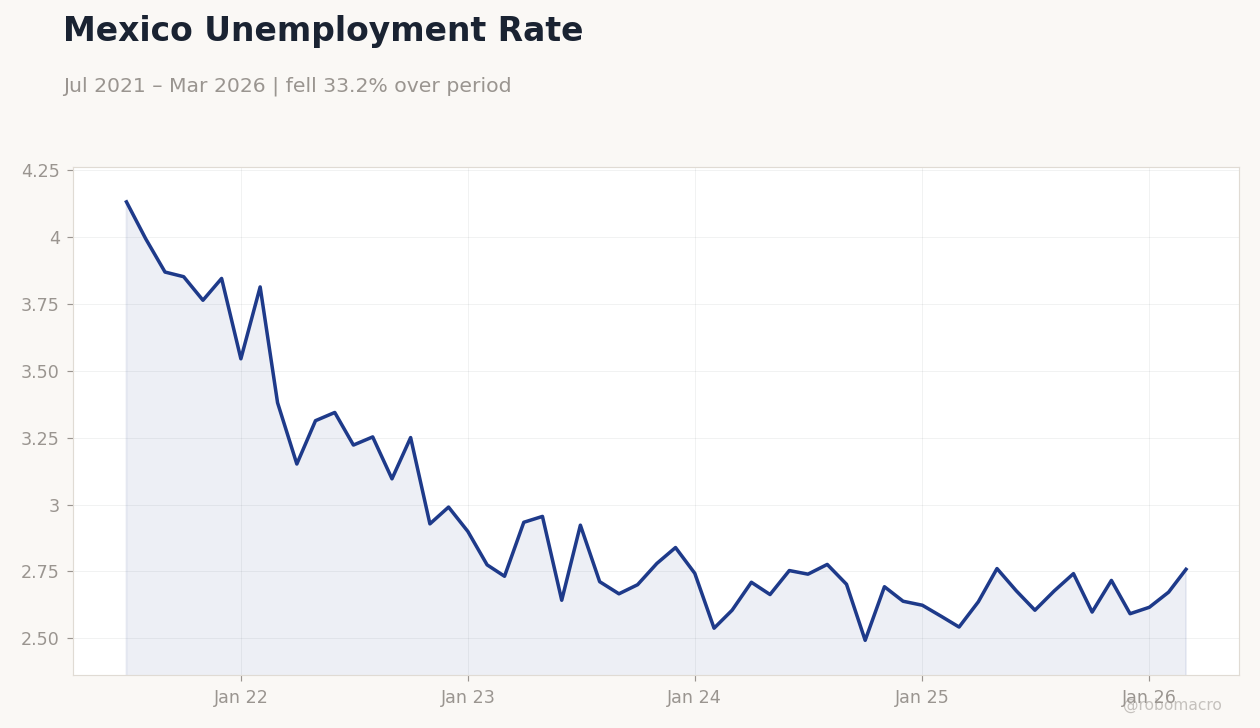

Mexico Unemployment Rate | Type: macro_line | Unemployment %: 2.758 (2026-03-01) | Range: 2.493–4.129 | Trend(5pt): 4.129,3.096,2.78,2.624,2.758

Mexico Unemployment Rate | Type: macro_line | Unemployment %: 2.758 (2026-03-01) | Range: 2.493–4.129 | Trend(5pt): 4.129,3.096,2.78,2.624,2.758

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Mexico May inflation undershoots at 3.94% y/y versus 4.03% consensus, with MoM at -0.21%.

- USD/MXN falls 0.38% to 17.39 as short-term rates ease to 5.43%.

- IPC Bolsa edges up 0.22% amid contained price pressures and stable Banxico outlook.

Yesterday's Recap

Mexico’s May inflation rate came in at 3.94% y/y, below the 4.03% consensus and prior 4.45% reading, while the month-over-month figure printed -0.21% against an expected -0.12%. The softer print reflected broad-based moderation in goods and services prices. The IPC Bolsa closed 0.22% higher at 64,962.02, supported by limited selling pressure on financials.

USD/MXN declined 0.38% to 17.39, with EUR/MXN also down 0.40% at 20.05. Mexico’s short-term rate fell 1.63% to 5.43%, while the long-term rate rose 1.60% to 8.88%. WTI crude slipped 0.31% to 89.75 amid softer energy demand signals.

Market participants viewed the inflation data as reinforcing expectations for steady policy.

The Day Ahead

No Mexico-specific data releases or central bank events are scheduled for today or tomorrow. Traders will monitor any follow-up commentary from Banxico officials on the inflation trajectory. Focus remains on external drivers including U.S.

trade policy signals and global commodity moves. Industrial production and other June indicators are not due until later in the month. Markets are expected to stay range-bound absent fresh catalysts.

Other Economic Notes

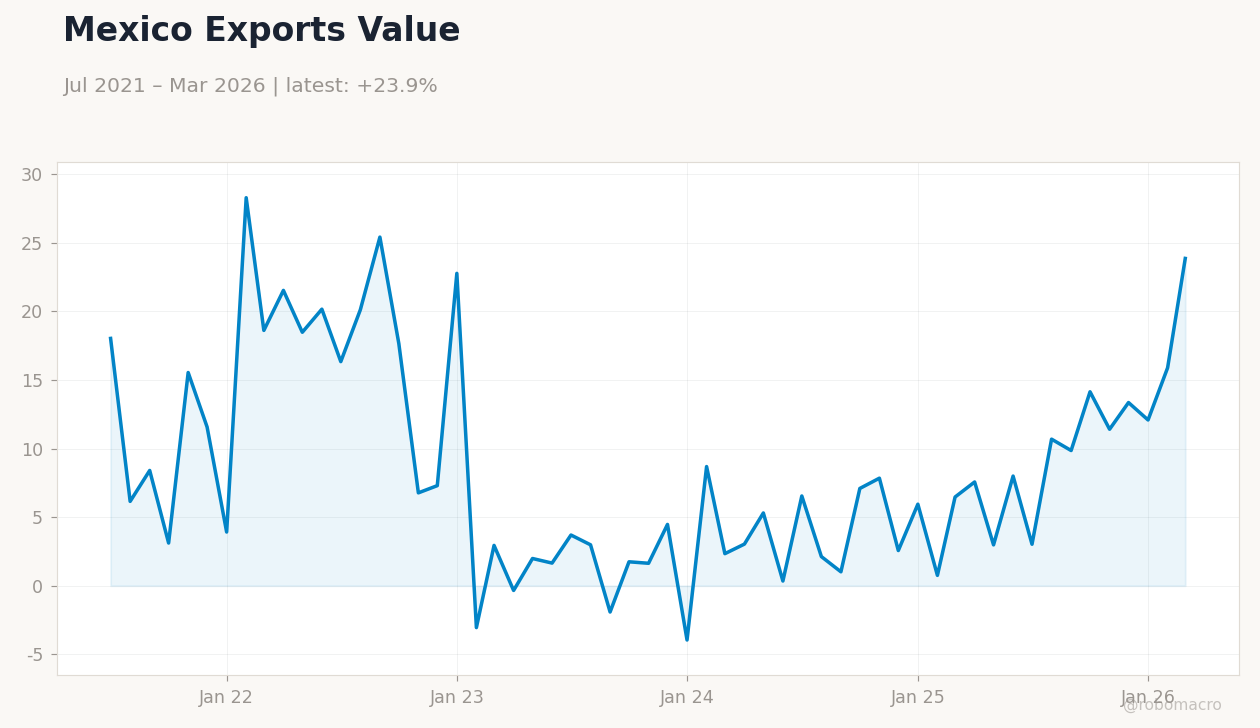

Nearshoring activity continues to underpin manufacturing exports despite the lack of fresh monthly figures. Remittances remain a key support for household consumption and the current account. Energy sector reforms show no legislative progress, leaving investment plans on hold.

USMCA-related uncertainty from renewed U.S. comments adds modest volatility to the peso without immediate disruption to trade flows.

Global Macro News

U.S. President Trump reiterated threats to withhold renewal of the USMCA trade deal with Mexico and Canada, citing unfavorable terms. The Bank of Canada held its policy rate at 2.25% as domestic growth slowed.

Turkey’s central bank also kept rates unchanged amid cooling activity. <i>↓ p.2</i>